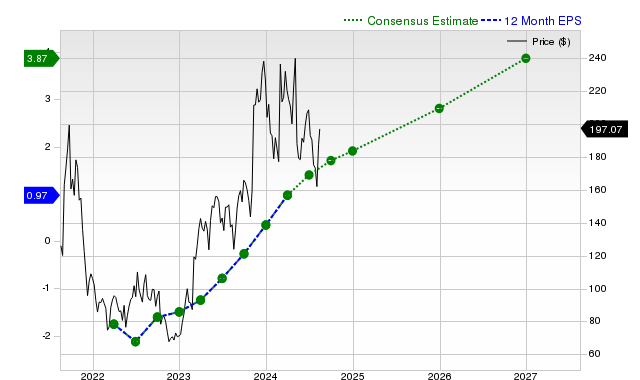

Duolingo (DUOL) shares have recently underperformed, declining 9.5% over the past month against broader market gains, despite strong positive earnings and revenue estimate revisions. Current fiscal year EPS estimates have been raised 7.7% over 30 days to $3.12 (+66% YoY), with revenue projected to reach $1.02 billion (+36.3% YoY). While the company consistently beats consensus estimates, its Zacks Rank #3 (Hold) suggests near-term market-in-line performance, and an 'F' grade for valuation indicates it trades at a significant premium to peers.

Duolingo (DUOL) presents a clear divergence between its fundamental growth trajectory and recent market performance, creating a classic growth-versus-valuation dilemma for investors. While the stock has declined 9.5% over the past month, significantly underperforming the S&P 500's +2% gain and its technology services industry's +11.6% rise, the company's underlying metrics remain robust. Analyst earnings estimates are consistently being revised upwards; the consensus for the current fiscal year has increased by 7.7% over the last 30 days to $3.12 per share, representing a 66% year-over-year growth projection. This is supported by strong revenue forecasts, with estimates pointing to a 36.3% increase to $1.02 billion this year and a further 25.8% rise to $1.28 billion next year. Duolingo's execution is also strong, having beaten revenue estimates for the past four quarters and delivering a significant +65.45% EPS surprise in its last report. However, these positive factors are tempered by significant valuation concerns, as evidenced by a Zacks Value Style Score of 'F', which indicates the stock is trading at a premium to its peers. The resulting Zacks Rank #3 (Hold) suggests these conflicting signals are likely to lead to near-term performance in line with the broader market.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mixed

Sentiment Score

0.05

Ticker Sentiment