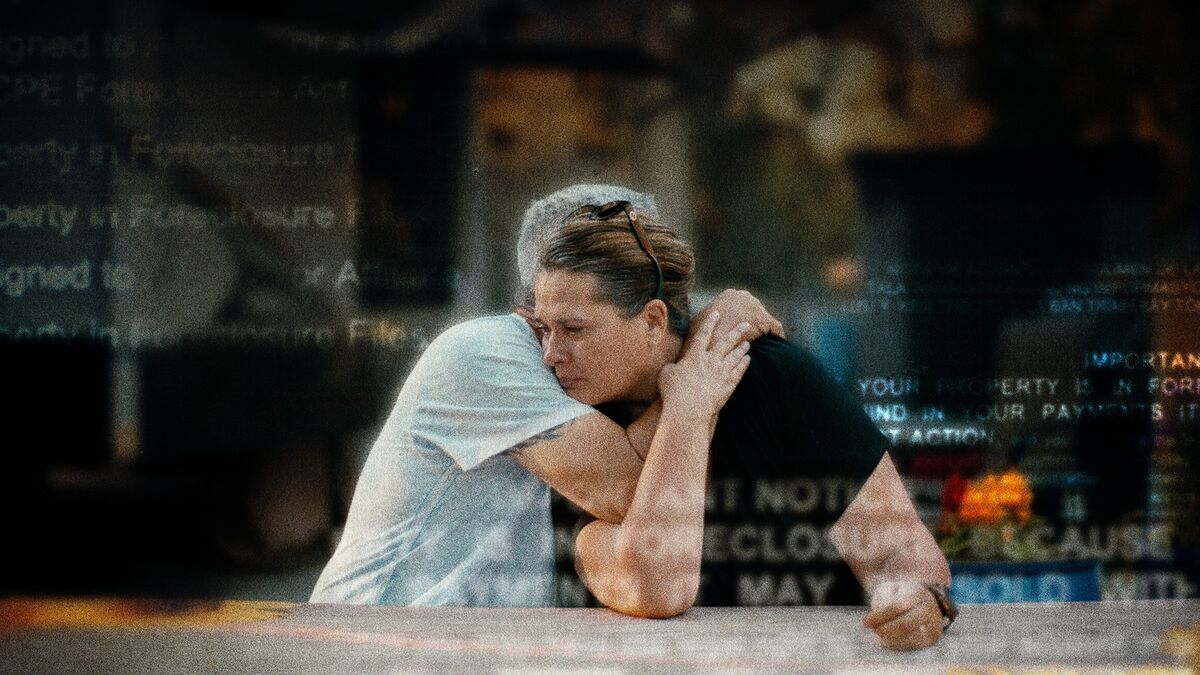

A growing secondary market in so-called “zombie” mortgages is enabling private equity and debt buyers to revive long-dormant second liens and pursue foreclosures, often for sums far above original balances. In one case Bloomberg Investigates documents show Scott and Kari Amable lost their three‑bedroom house in 2021 after a debt collector claimed roughly $200,000 on a second mortgage they originally borrowed $98,000 for and were previously told had been canceled. The trend creates profit opportunities for buyers while exposing homeowners, servicers and potentially regulators to legal and reputational risk as dormant mortgage claims are resurrected amid recovering home prices.

Market structure: Private debt buyers and credit managers (large PE firms and mortgage credit REITs) are the direct beneficiaries — they acquire “zombie” second liens at pennies-to-dollars on the dollar and extract value via foreclosure or collection, lifting returns by an estimated 20–40% IRR on acquired pools if local prices hold. Losers are distressed homeowners (consumer welfare, legal claims), mortgage servicers (reputational and operational strain), and localized housing markets where forced sales can depress prices by 3–8% in affected ZIP codes over 6–18 months. Risk assessment: Tail risks include a regulatory wave (federal/state moratoria, retroactive debt forgiveness or large fines) or mass successful litigation that could wipe out valuations of acquired loan portfolios; probability medium but impact high (write-downs >50% for specialty buyers). Short-term (0–3 months) headline volatility; medium-term (3–12 months) potential for increased foreclosure flows; long-term (12–36 months) structural changes if legislation limits secondary debt sales. Hidden dependencies: mortgage servicers’ data accuracy and statute-of-limitations laws vary by state — a single adverse appellate decision in a large state (e.g., CA, NY) is a catalyst. Trade implications: Expect widening non‑agency MBS spreads and higher credit provisions at regional banks, creating opportunities to short mortgage credit risk (NRZ, TWO) and regional bank ETFs (KRE) while buying protection on mortgage REITs (REM). Conversely, large diversified alternative managers (BX, ARES) with credit arms stand to earn fees and acquire assets but face political risk; a long/short relative-value approach reducing idiosyncratic legal exposure is warranted. Entry: act quickly on options protection within 1–3 months around investigative headlines; exit or trim on any regulatory clarity within 6–12 months. Contrarian angles: Consensus focuses on borrower harm and headline risk, underestimating the durability of private-credit economics — if lawsuits are limited and local housing remains tight, collectors can recoup >100% of purchase price within 12–24 months. Reaction may be overdone for diversified managers (BX, ARES) whose scale dilutes legal risk; underdone for small mortgage REITs and specialty debt buyers where single-state rulings can cause >30% NAV shocks. Historical parallel: post-2008 distressed mortgage trades delivered outsized returns but were concentrated and legally complex; similar specialization is required now.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

strongly negative

Sentiment Score

-0.65