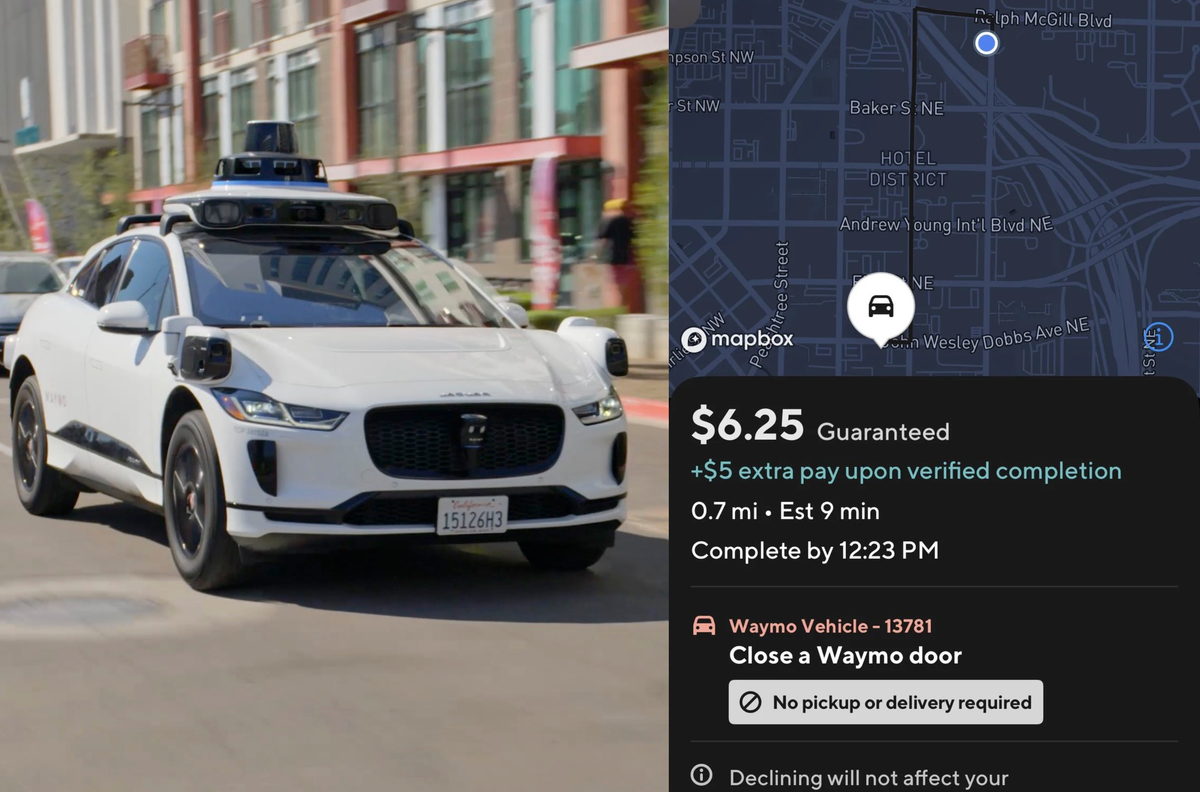

Waymo and DoorDash are running an Atlanta pilot that notifies nearby Dashers to close a Waymo vehicle's ajar door, with at least one reported job paying around $10 (a screenshot showed $6.25 guaranteed plus $5 on verified completion) for a roughly 0.7-mile trip. The partnership, begun earlier this year, is intended to get AVs back on the road quickly while providing Dashers incremental earnings; Waymo said future vehicles will have automated door closures and declined to provide detailed payment mechanics. The measure highlights a minor operational friction in AV deployment and an ongoing commercial tie-up between the two firms, but it is unlikely to have material financial impact on either company.

Market structure: This pilot is a small but structurally meaningful example of platform arbitrage — DoorDash (DASH) captures microtask revenue and Waymo reduces fleet downtime. Winners: DoorDash (incremental take-rate, retention), Waymo (lower operational delays), nearby gig workers; losers: legacy fleet operators and robo‑taxi revenue models that priced immediate driverless scale. Expect 1–3% incremental Dasher utilization and 50–200 bps potential gross-margin lift for DoorDash if scaled to multiple metros over 6–24 months. Risk assessment: Tail risks include a high‑profile safety/insurance incident or regulator reclassification of microtasks (5–10% probability over 12–24 months) that could drive a 15–40% equity re‑rating. Immediate (days) impact is negligible; short term (weeks–months) depends on pilot disclosures and Q‑report metrics; long term (2–5 years) the trend is ambiguous as Waymo’s statement that automated door closures are planned implies this revenue may be temporary. Hidden dependencies: who pays the fee, verification tech, and wage inflation that could erode margins by 30–70% of incremental revenue. Trade implications: Tactical long in DASH size 1–2% portfolio via 3‑month call spread (ATM to +15%) targeting +10–20% in 3–6 months; stop if downside exceeds 8%. Pair trade: long DASH vs short UBER (1:1, 0.5–1% net) for 3 months to exploit better local delivery monetization. Trim high‑multiple AV suppliers/exposure (e.g., NVDA, MBLY) by 10–20% pending softer robo‑taxi monetization over 12–24 months. Contrarian angles: The market underestimates microtaskability as a durable UX/retention lever — 2–5% higher Dasher time could convert to $100–200M incremental revenue for DoorDash (12‑24 month run‑rate) yet this is fragile to fraud/verification costs. Reaction is underdone today but could reverse quickly if Waymo deploys automated door closures within 12–36 months or if regulators cap pay‑per‑task models, creating binary 20–40% moves.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

neutral

Sentiment Score

0.10

Ticker Sentiment