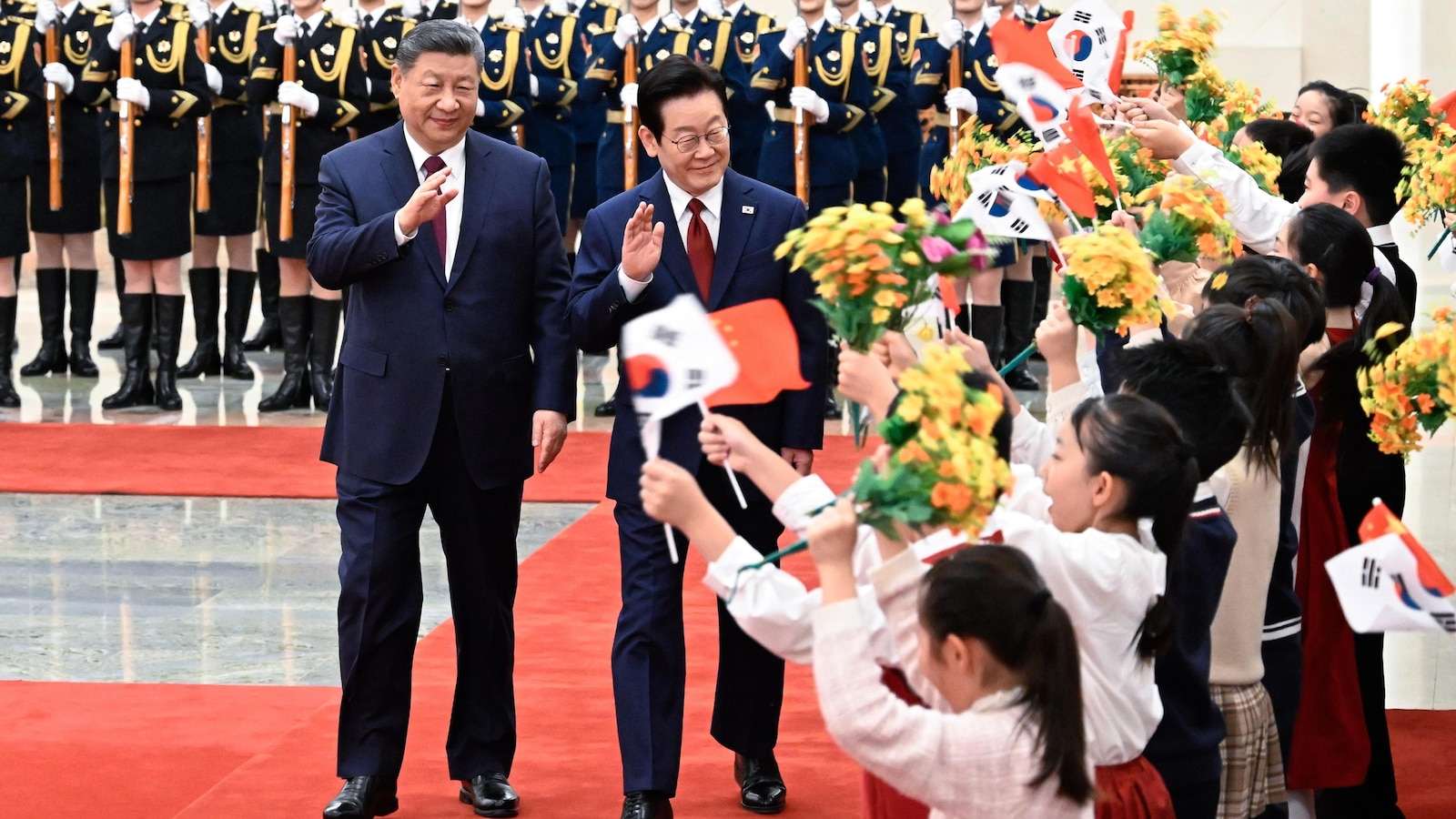

Chinese President Xi and South Korean President Lee Jae Myung agreed to deepen economic ties and bolster regional stability during Lee's first visit since taking office, overseeing the signing of 15 cooperation agreements across technology, trade, transportation and environmental protection and noting bilateral trade of about $273 billion in 2024. The talks and a business forum involving Samsung, Hyundai, LG and Alibaba aim to reduce bilateral friction and support commercial ties, but the visit was overshadowed by North Korean ballistic missile tests and rising China-Japan tensions, leaving a mix of trade-positive outcomes and sustained geopolitical risk for investors.

Market structure: A sustained China–South Korea thaw reduces near-term political tail-risk to cross-border supply chains and favors Korean exporters (autos, consumer electronics, semiconductors) and Chinese importers/services. Bilateral trade was ~$273bn in 2024; if implemented deals lift trade growth by 3–5% year-over-year in the next 12 months, expect incremental volume-driven revenue upside of 5–10% for large exporters versus peers. Pricing power will tilt to integrated Korean suppliers (Samsung, Hyundai suppliers) rather than fragmented assemblers in Southeast Asia. Risk assessment: Tail risks include a military escalation with Japan/US or tougher export controls from the US/EU that re-tighten tech flows — low-to-medium probability but high impact (earnings shocks >20%). Immediate market moves (days) will be driven by headlines; supply-chain reconfiguration and FDI shifts play out over quarters (2–12 months). Hidden dependencies: Chinese leverage over North Korea and China’s domestic policy (tariffs, subsidy shifts) could reverse benefits quickly if geopolitics harden. Trade implications: Tactical plays include selective long exposure to Korean semiconductor and auto names and opportunistic long calls on equipment suppliers (ASML) to capture capex normalization; hedge with out-of-the-money defense longs to protect against escalation. Expect FX moves: KRW likely to strengthen modestly (1–4%) on improved trade sentiment; JPY safe-haven moves can spike 2–6% on any escalation, pressuring Japan-exposed exporters. Contrarian angle: Consensus frames this as Korea pivoting fully to China; reality is nuanced — Seoul will retain US ties, so structural decoupling is unlikely. That suggests the market may be underpricing cyclical upside in Korean industrials and overpricing long-duration defense premium absent a clear escalation path; mispricings should resolve within 3–12 months as trade data and deal execution become visible.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mixed

Sentiment Score

0.00