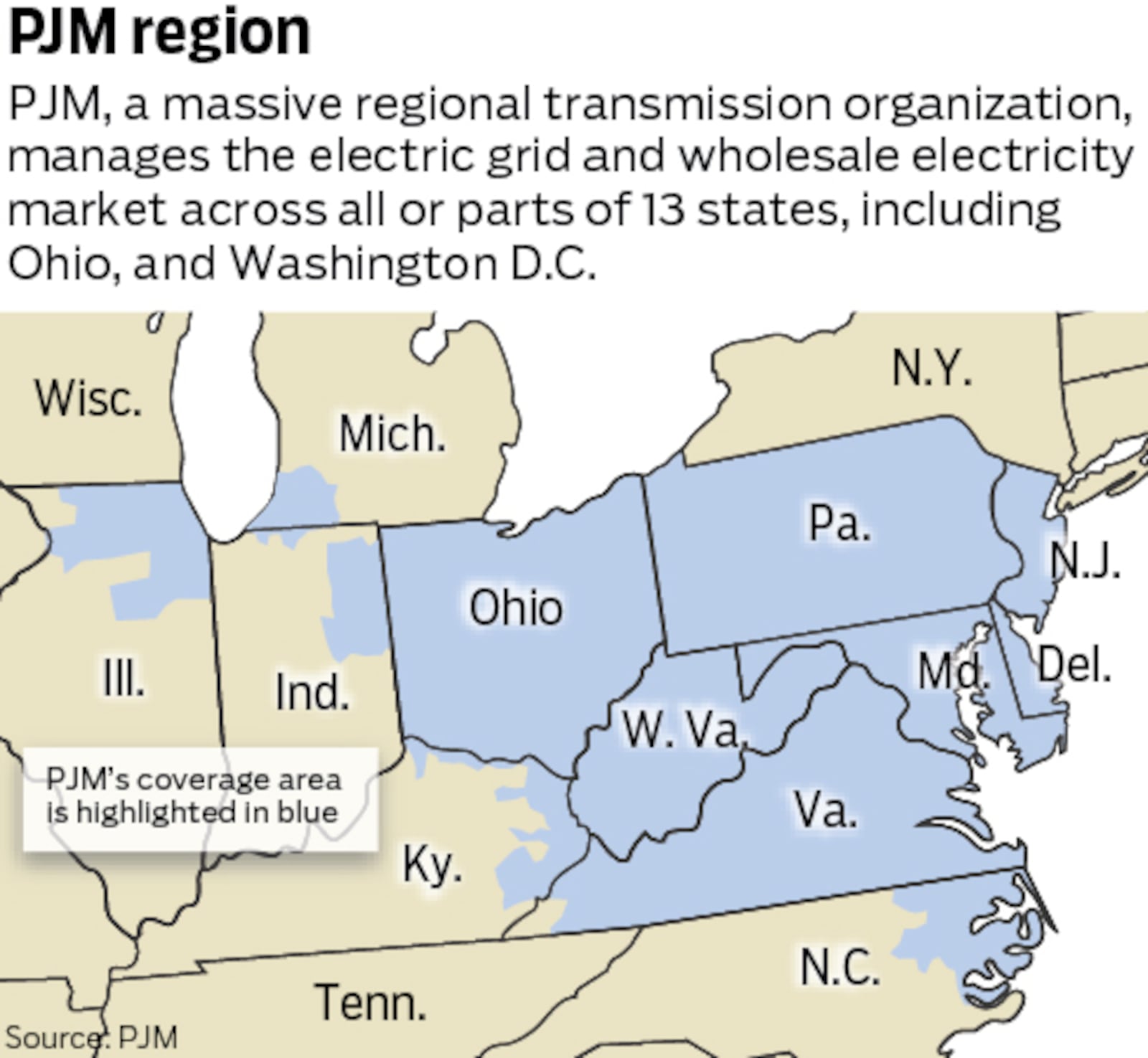

PJM capacity prices spiked sharply as data center demand increased projected capacity needs, with the benchmark capacity price rising 833% between the 2024-2025 and 2025-2026 delivery years and another 22% for 2026-2027 even after regulatory intervention. State governors and federal officials proposed extending retail price caps and requiring data centers to pay for new capacity, a move projected to save roughly 67 million PJM consumers about $27 billion over two years; the dynamic creates regulatory risk for generators, transmission & distribution providers and the economics of large data center projects. Utilities that do not own generation, such as AES Ohio, warn that new large loads require transmission investments and that cost-allocation and obligation-to-serve rules will drive local rate and infrastructure outcomes.

Market structure: PJM’s capacity shock (benchmark +833% YoY in one step, then a further +22% for 2026-27) reallocates economic rents toward assets that can provide firm capacity quickly — merchant generators, battery/peaker projects and transmission/T&D contractors. Losers are pure distribution utilities with no generation exposure and regional data-center landlords (EQIX, DLR) that absorb incremental operating costs or face special charges; consumers are insulated if caps are implemented (study cites ~$27B savings over two years). Capacity scarcity signals a persistent supply shortfall in PJM vs. big-load growth from hyperscalers, not a transitory weather event. Risk assessment: Near-term (days-weeks) risk is policy volatility: legislative/PUC fixes or emergency auctions that can reverse price discovery; medium-term (3–12 months) risk is protracted permitting and transmission lead times that raise capex and default risk for smaller IPPs. Tail risks include a state-level moratorium on new data centers or retroactive cost re-allocation (high-impact but ≤10% probability) and contagion into municipals/bank loans where local tax incentives backstop projects. Hidden dependencies: water constraints for cooling and interconnection queue delays that can delay supply response by 12–36 months. Trade implications: Implement a 2–3% portfolio long in merchant/firming generators (split VST 40% / NRG 30% / NEE 30%) with 12–18 month hold to capture capacity/energy upside; pair with a 1–1.5% short in data-center REITs (EQIX, DLR) funded by proceeds. Add a tactical buy of Quanta Services (PWR) at +1.5% as a play on grid build; hedge downside by buying 3-month EQIX 10% OTM puts (size 0.5% notional). Exit/trim if PJM’s effective retail-cap rollback reduces forward capacity curves by >30% vs. current levels. Contrarian angle: Consensus assumes caps permanently protect retail rates — underappreciated is cost-shifting: regulators will likely force bespoke tariffs/connection fees that monetize new capacity for generators and contractors. That favors developers able to sign long-term contracts (NRG/Vistra) and disfavors landlords who lack pass-throughs; historical PJM capacity events (post-2014 price shocks) show sharp reversals when new capacity online — watch interconnection completions as the true price trigger (12–36 month horizon).

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately negative

Sentiment Score

-0.45