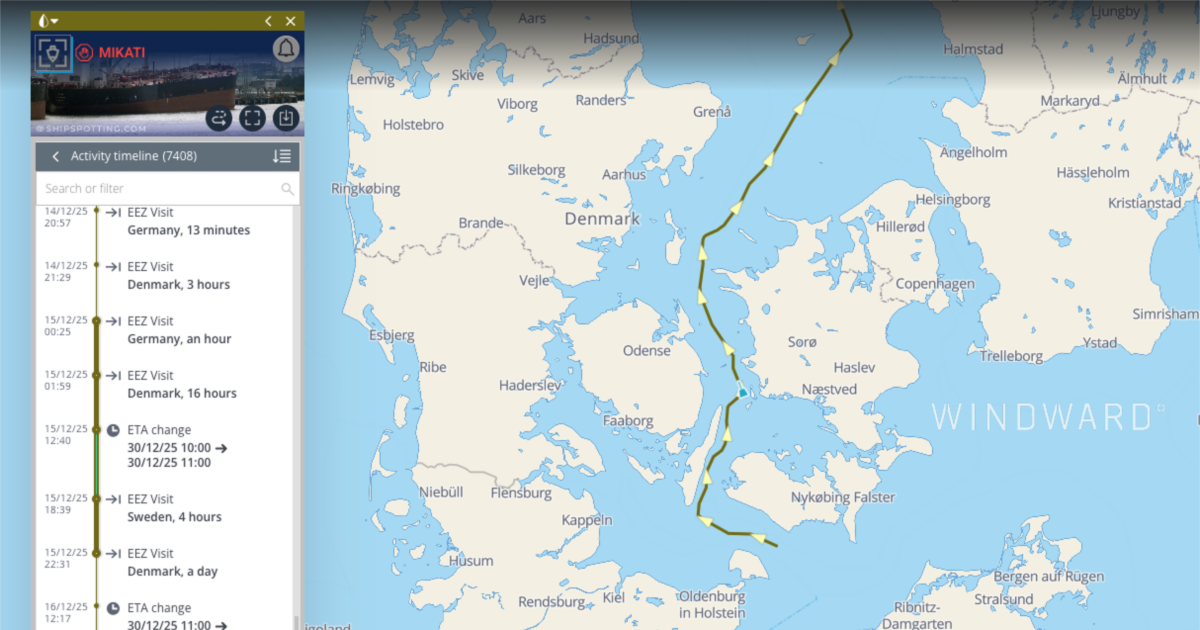

The 58,000-ton tanker Mikati — built in 2003 and added to the EU’s 18th Russia sanctions package on July 18 after AIS shutdowns, repeated name/flag changes and opaque ownership transfers — continued to move Russian crude via partial unloads in India, a ship-to-ship transfer with the blacklisted Noctis at Port Said, and delayed discharge in China, illustrating shadow-fleet evasion tactics. Intelligence firm Windward and analytics firm kpler show sanctioned vessels suffer large productivity hits but that Russian crude exports have largely persisted (kpler: ~30% productivity decline for EU sanctions vs ~70% for US OFAC), underscoring that EU measures are disruptive but comparatively leakier than U.S. sanctions.

Market structure: Sanctions fragment the tanker market into two pools — OFAC-compliant (de facto preferred by major buyers) and EU/UK-only blacklists (tolerated by India/China). Empirical signals: EU listings remove ~30% of a vessel's productivity on average while OFAC listings show ~70% declines; if OFAC coverage rises from ~40% to >60% within 90 days, expect a material squeeze in available compliant VLCC/Aframax capacity and a 20–50% rise in charter rates over 1–6 months. Higher freight spreads will transfer pricing power to high-quality, Western-flagged owners and brokers with clear compliance chains. Risk assessment: Tail risks include stepped-up OFAC secondary sanctions (high-impact, low-probability) that could instantaneously freeze routes to India/China and spike Brent 5–15% in 1–3 months, or retaliatory shipping insurance networks forming outside Western markets that restore capacity within 6–12 months. Hidden dependencies: insurance corridors (P&I clubs, Lloyd’s syndicates) and flag-state registries are chokepoints; monitoring weekly OFAC/EU lists and insurance underwriting notices is critical. Catalysts: major OFAC wave, a large STS-facilitated shipment de-anonymization, or China/India formal policy shifts can accelerate flows. Trade implications: Tactical winners are high-quality tanker owners and listed shipowners with Western insurance access (e.g., FRO, EURN) and sellers of freight derivatives; tactical losers are aging/anonymous-flagged owners, small opaque trading houses, and any firm relying on Russian crude access via shadow-fleet routes. Hedging oil-price upside via short-dated Brent call spreads is sensible to capture sanction-driven spikes, while selective long positions in compliance-focused insurers/brokers can monetize higher premiums. Contrarian angles: Consensus assumes sanctions permanently remove capacity; history (1990s sanctions circumvention, Iran) shows capacity often re-routes via non-Western insurance and STS markets within 6–12 months, compressing freight upside. The market may be overpaying for “sanction-proof” tonnage now; watch for cyclical mean-reversion in TC rates — if TC indices rise >40% in 90 days, it becomes attractive to fade with mean-reversion shorts in specialist small-cap owners that lack compliance credits.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately negative

Sentiment Score

-0.25