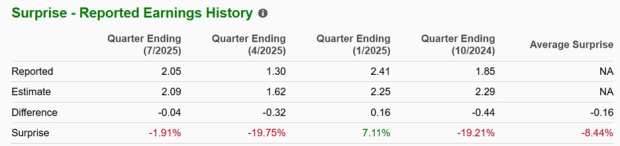

Ahead of their Q3 reports, Walmart — up ~14% YTD — is forecast to report sales of $177.14 billion (up >4% y/y) and EPS of $0.61 (up ~5%), while Target — down ~30% YTD — is expected to report $25.36 billion in sales (-1%) and EPS of $1.76 (-5%). Walmart’s recent outperformance reflects scale and e‑commerce leverage (more than $100 billion in digital sales), expansion into higher‑margin businesses (advertising, memberships, marketplace) and a string of modest earnings beats (3 of 4, avg surprise +2.8%), supporting a premium ~39x forward multiple; Target has lagged on sales and margins, missed consensus in 3 of 4 quarters (avg surprise -8.4%), trades at a material discount to the S&P/sector and its decade median, and offers a ~5.1% yield versus Walmart’s ~0.9%. Both stocks carry a Zacks Rank #3 (Hold); the looming Q3 prints will be decisive for whether Walmart’s secular initiatives sustain further upside or Target can validate a valuation recovery through operational improvements and dividend‑driven total return.

Consensus estimates position Walmart to report Q3 sales of $177.14 billion (up >4% y/y) and EPS of $0.61 (up ~5%), while Target is expected to show Q3 sales of $25.36 billion (down ~1% y/y) and EPS of $1.76 (down ~5%); market performance this year reflects that divergence with WMT up ~14% and TGT down ~30%. Walmart has a recent track record of modest beats (3 of 4 quarters, avg surprise +2.79%) despite a Q2 miss, and the company now generates over $100 billion in digital sales while expanding higher-margin lines such as advertising and marketplace services. Target has missed EPS consensus in 3 of the last 4 quarters with an average surprise of -8.44%, exhibiting weaker sales growth and margin pressure that have driven a valuation roughly 20% below its decade median and a steeper share-price decline. Both names trade at price-to-forward-sales below 2x and are Zacks Rank #3 (Hold); Walmart’s 39x forward P/E reflects a premium for growth and operational diversity, while Target’s ~5.07% yield versus Walmart’s ~0.92% frames the tradeoff between income and secular growth, making the upcoming Q3 prints the key near-term catalyst to validate either narrative.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

mixed

Sentiment Score

0.00

Ticker Sentiment