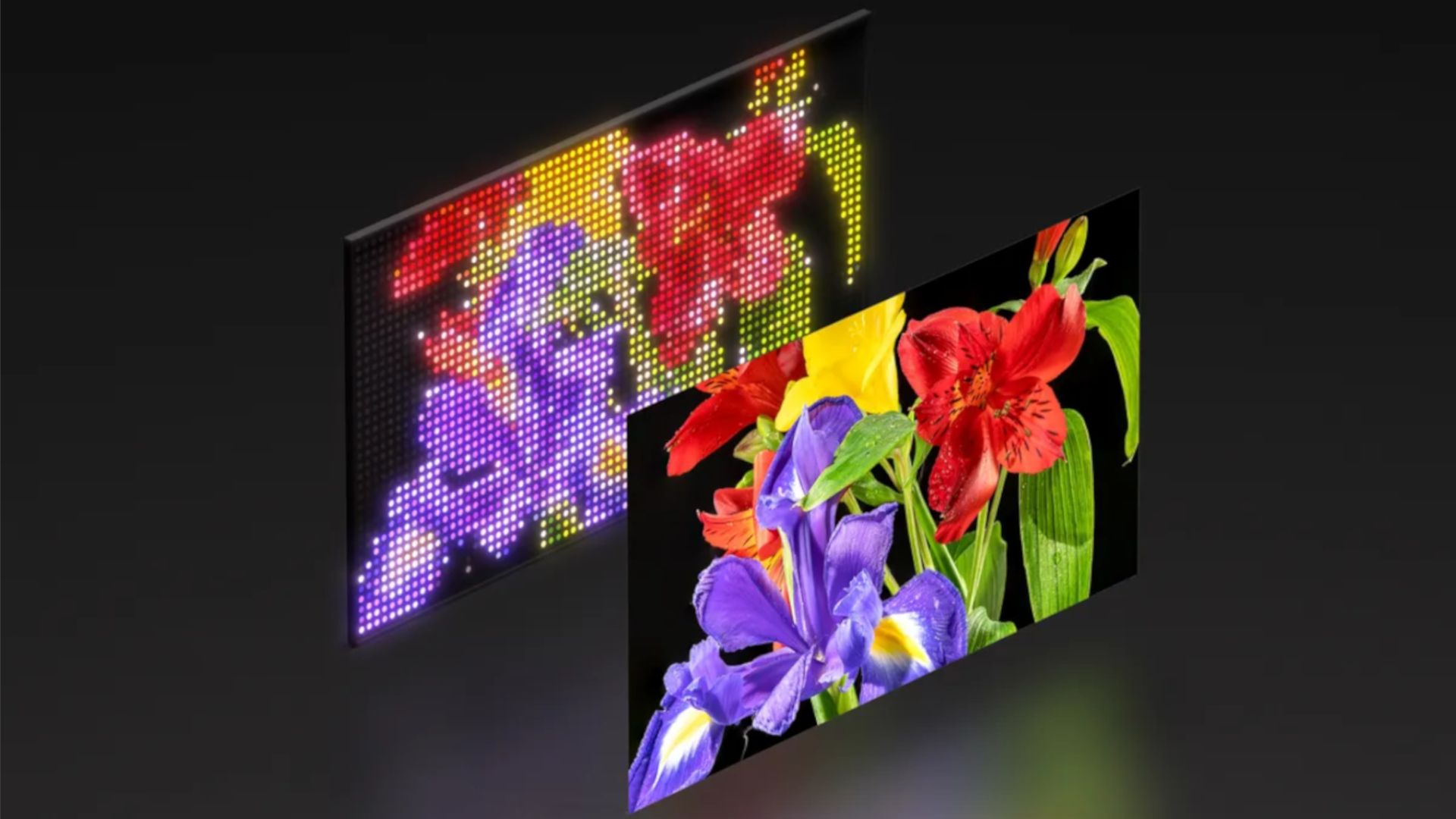

RGB LED TVs are debuting in 2026 with Hisense and Samsung rolling out models (e.g., Hisense UR9/UR8, Samsung R95H) in popular 55"–65" sizes while neither brand has announced high-end Mini-LED flagships (Hisense U8, Samsung QN90). If RGB adoption succeeds, Mini-LED could be pushed toward budget/mid-range tiers or, alternatively, current mid-tier Mini-LED models (Hisense U7SG, Samsung QN80H) may inherit flagship roles — outcomes will reshape product segmentation, pricing and competitive positioning over the next 12–24 months.

RGB LED adoption is a classic disruptive-upmarket move: manufacturers substitute a higher-performance but initially costlier backlight technology into flagship skews and let last-generation Mini-LED cascade down the lineup. That shift creates a multi-year capex and BOM reallocation: demand for RGB LED die (especially discrete red/blue chips), micro-assembly tooling and new LED driver ICs will spike in the next 6–18 months while traditional backlight component orders for legacy Mini-LED rise on volume but decline in ASP.

Second-order winners are specialized LED chipmakers and analog/driver silicon vendors that can supply high-voltage, high-density channel drivers and testing IP at scale; panel assemblers that integrate LED arrays cleanly will gain negotiating leverage to capture 100–300bps margin premium. Conversely, vendors reliant on economies of scale in standard Mini-LED manufacturing and commoditized TFT/LCD lines face margin compression if they cannot retrofit lines or secure differentiated RGB supply, creating potential share shifts among ODMs over 12–24 months.

Key catalysts that will determine the pace: early yield rates for RGB assemblies (a 5–10% yield difference vs Mini-LED will materially change cost parity), consumer willingness to pay a 10–30% ASP premium for brighter/purer color, and any rapid improvements in OLED/QD-OLED cost curves that could re-steal the “best non-OLED” crown within 18 months. Monitor quarterly capex guides from major panel/LED suppliers and patents or supply agreements that lock up RGB die volume — those are leading indicators for which brands can scale.

Contrarian risk: RGB may initially be a flagship niche rather than a full replacement; high manufacturing complexity means many brands will keep upgraded Mini-LED flagships to protect margins, delaying mass RGB penetration beyond 2027. If that happens, the market could be overpaying today for suppliers assumed to be sole beneficiaries, creating a 6–18 month re-rating risk.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly positive

Sentiment Score

0.20

Ticker Sentiment