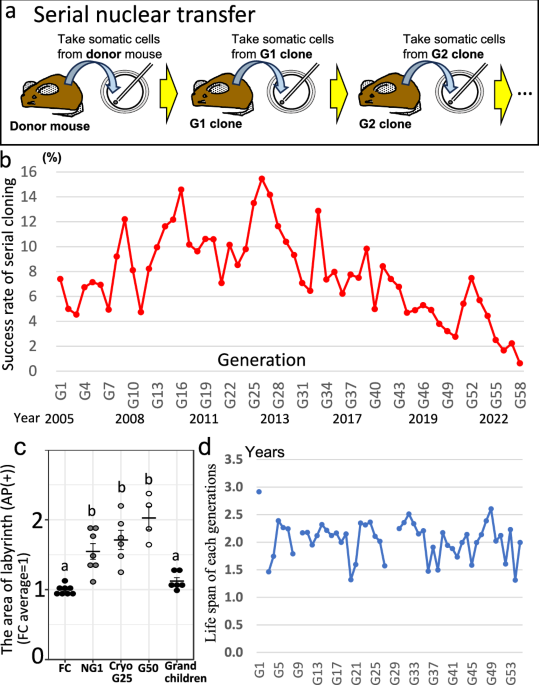

Serial somatic-cell nuclear transfer in mice was continued for ~20 years and 58 generations, but cloning success peaked at 15.5% (gen 26) then fell to an average 0.6% by gen 57 and failed at gen 58. Whole-genome sequencing shows accumulation of ~69 SNVs and ~1.4 indels per generation (≈3,700 SNVs and 80 indels total G1–G57) plus ~1.5 SVs per generation and multiple large structural variants (e.g., X loss, LOH, translocations) after G23–G25, which the authors link to collapse of cloning viability. Implication for investors: this paper reduces the technical feasibility outlook for long-term clonal propagation as a scalable commercial solution (e.g., animal cloning for agriculture or species rescue), suggesting limited near-term commercial upside and higher technical/biological risk for companies relying on repeated clonal propagation.

Near-term commercial winners are likely to be suppliers of high-throughput wet‑lab consumables and diagnostic kits rather than niche cloning service providers. Structural-variant detection and high-confidence WGS across many samples create recurring demand for reagents, library prep, and clinical-grade sample handling, favoring diversified lab-supply franchises with broad margins and predictable consumables revenue. In parallel, an under‑the‑radar bifurcation should accelerate: short-read volume will rise (higher sample throughput, cost-per-sample wins) while demand for long-read/orthogonal SV callers grows for definitive calls — that puts pressure on incumbents that lack a clear long-read strategy.

Key tail risks and catalysts cluster around technology and regulation. A technical breakthrough that allows routine in situ repair or elimination of large SV burdens (gene editing, more effective cytoplasmic rescue) would shorten the commercialization timeline for any cloning-derived applications and reduce downstream sequencing demand; conversely, restrictive regulation or high‑profile ethical rulings would curtail adoption and cap market expansion. Expect tradable catalysts on 3 time horizons: 0–6 months (sequencing consumables revenue prints and kit supply announcements), 6–24 months (adoption signals for long-read validation in clinical workflows), and 2–5 years (regulatory clarity or demonstration of reliable genomic‑repair workflows).

Consensus overlooks two second‑order effects: (1) increased need for end‑to‑end quality systems (sample tracking, contamination controls, validated pipelines) which favors vertically integrated vendors, and (2) accelerated demand for diagnostic-grade SV calls in animal breeding and conservation that can create non‑human recurring revenue streams. The market is not binary — winners will be those that combine consumables scale, bioinformatics IP, and a clear path to long‑read interoperability.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

neutral

Sentiment Score

0.00

Ticker Sentiment