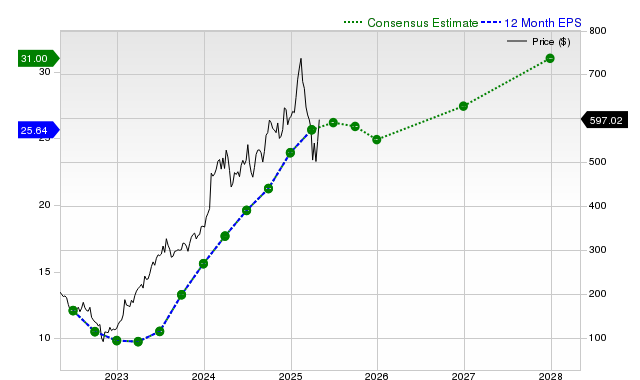

Meta Platforms (META) shares have declined 14.4% over the past month, underperforming the S&P 500 and its industry, despite consistently beating earnings and revenue estimates in the last four quarters. Analysts project robust revenue growth of over 20% for the current fiscal year and 17.2% for the next, with next fiscal year EPS expected to jump 27.3% to $30.23. However, due to recent estimate revisions, Meta currently holds a Zacks Rank #3 (Hold), suggesting it may perform in line with the broader market in the near term, while its valuation is assessed as trading at par with peers.

Meta Platforms (META) shares have experienced a significant decline of 14.4% over the past month, sharply underperforming the S&P 500's 1.4% gain and the Internet - Software industry's 11.8% loss. This recent downturn occurs despite Meta being a heavily searched stock, indicating high investor interest amidst its volatility. The company has consistently demonstrated strong operational performance, beating both EPS and revenue consensus estimates in each of the last four quarters, with the most recent quarter showing a 9.68% EPS surprise and a 3.63% revenue surprise. Analysts project robust future growth, with current fiscal year revenue estimated to increase by 20.6% and next fiscal year EPS expected to jump 27.3% to $30.23. Despite these strong fundamentals and positive outlook, Meta Platforms currently holds a Zacks Rank #3 (Hold), influenced by recent earnings estimate revisions, suggesting it may perform in line with the broader market in the near term. Furthermore, its Zacks Value Style Score of 'C' indicates that the stock is trading at par with its industry peers on valuation metrics.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately positive

Sentiment Score

0.40

Ticker Sentiment