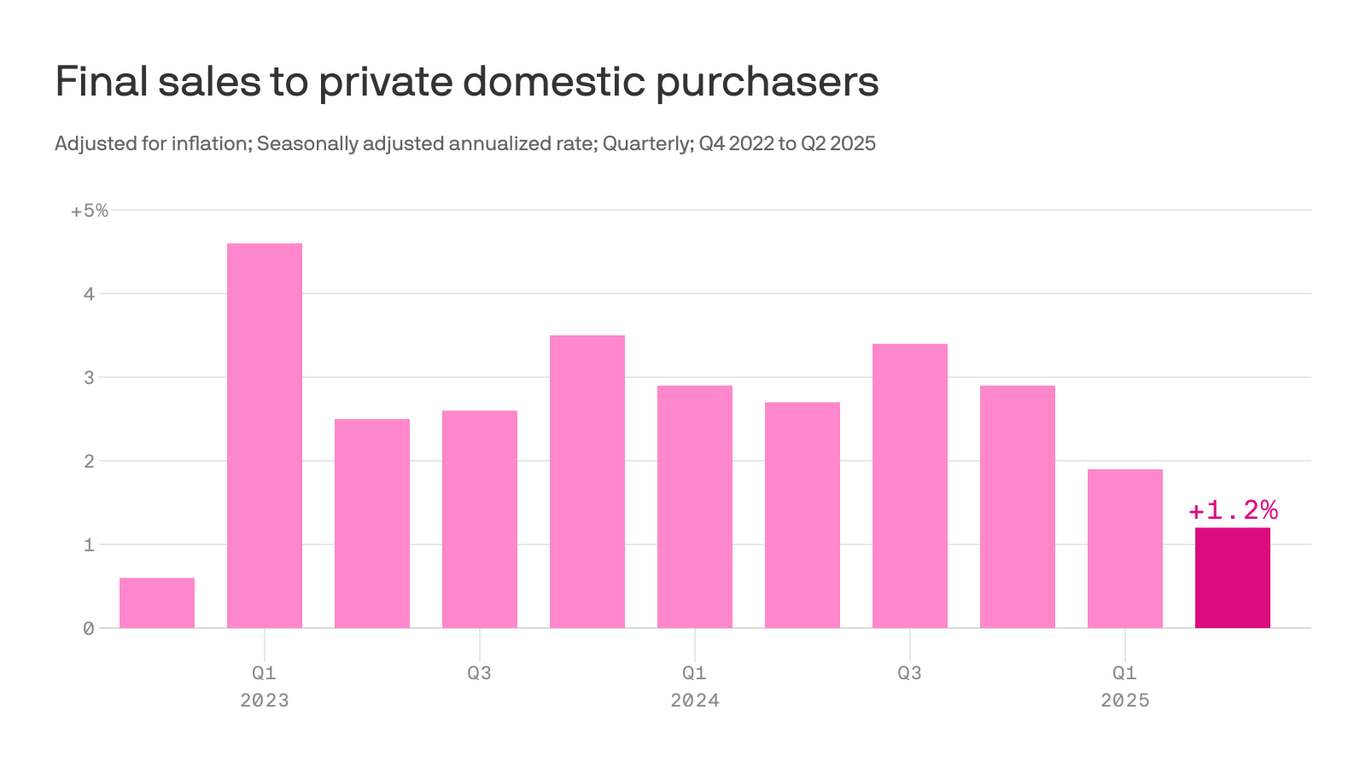

The U.S. economy's Q2 GDP grew at a robust 3% annual rate, but this headline figure masked significant underlying weakness, with real final sales to private domestic purchasers rising only 1.2%, the slowest pace since late 2022. This softness was driven by contractions in rate-sensitive sectors like residential and commercial construction. Coupled with Q2 PCE inflation at 2.1%, near the Fed's target, the data suggests that current elevated interest rates are dampening growth, strengthening the case for Federal Reserve rate cuts despite the strong top-line GDP.

Despite a robust 3% annualized headline GDP growth in the second quarter, underlying economic data reveals significant softness, strengthening the case for a dovish Federal Reserve policy shift. The headline figure was largely skewed by a normalization in import levels following a tariff-driven surge in Q1. A more accurate measure of private-sector health, real final sales to private domestic purchasers, grew at only a 1.2% rate, its weakest pace since late 2022 and a marked deceleration from the 3% rate in 2024. This weakness is concentrated in interest rate-sensitive sectors, evidenced by sharp contractions in residential investment, which fell 4.6%, and business structures, which fell 10.3%. The inflation picture further supports a less restrictive stance, with the Fed's preferred Personal Consumption Expenditures (PCE) Price Index rising just 2.1%, near the 2% target, although core PCE remains slightly elevated at 2.5%. The primary argument against imminent rate cuts stems from uncertainty over the future inflationary effects of tariffs, which appears to be the main factor delaying a policy change.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately negative

Sentiment Score

-0.40