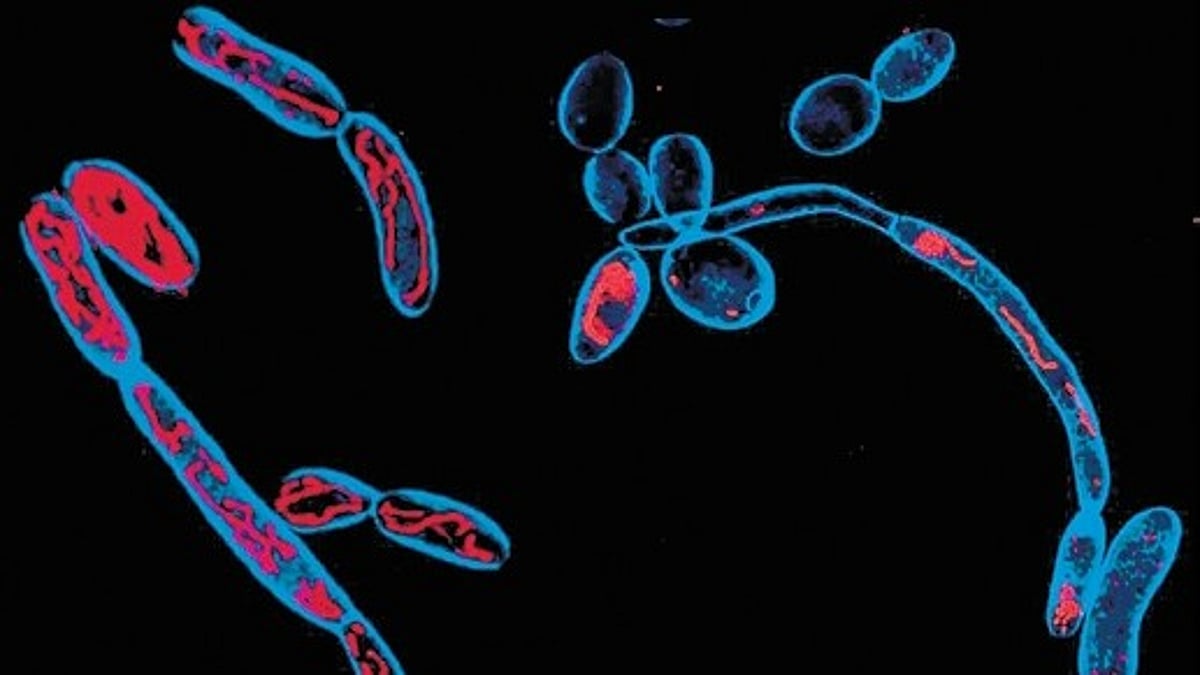

Researchers at CSIR-Centre for Cellular and Molecular Biology identified a metabolic control point linking rapid glycolysis to production of sulphur-containing amino acids that triggers fungi to switch from a benign yeast form to an invasive filamentous form. Experimentally slowing sugar breakdown kept fungi in the noninvasive yeast state, while adding sulphur amino acids restored invasiveness; a Candida albicans strain lacking a key glycolytic enzyme was metabolically weakened, more readily cleared by macrophages and caused milder disease in mice. The findings position fungal metabolism as a novel therapeutic target that could address rising antifungal resistance, but the evidence is preclinical and carries limited near-term commercial impact.

Market structure: The discovery creates clear winners — small/mid‑cap biotech and diagnostic players focused on antifungal mechanisms (metabolism-targeting drugs, combination therapies, companion diagnostics) and CROs that run IND‑enabling studies — because a new mechanism can command premium pricing and licensing fees. Incumbent broad‑spectrum antifungal sellers face longer‑term share erosion if metabolic approaches enable faster clearance or resensitize resistant strains; market shift to novel oral/systemic agents could reprice long‑run margins by ±10–30% in affected niches over 2–5 years. Risk assessment: Tail risks include translational failure (preclinical ↦ human efficacy), on‑target host toxicity (sulphur‑metabolism overlap), and IP/regulatory delays; any human safety signal could wipe 100% of microcap value. Time horizons: near term (days–weeks) no material market move; short term (3–12 months) bilateral licensing/academic replication is possible; long term (12–48 months) is when INDs/Phase I readouts and M&A value realization occur. Hidden dependencies: efficacy relies on in vivo metabolic gradients, drug delivery, and combination with existing antifungals. Trade implications: Direct plays: small, concentrated exposure to pure‑play antifungal developers (e.g., SCYNEXIS SCYX) and small‑cap biotech ETFs (XBI) via equity and calendar call spreads; use 6–12 month option tenors to capture licensing/M&A. Pair trades: long specialized antifungal microcap vs short generic antifungal suppliers with little R&D (to capture relative revaluation). Entry: scale in over 2–6 weeks; exit/trim on licensing, IND filing, or 12‑month no‑progress rule. Contrarian angles: The consensus underestimates ancillary opportunities — diagnostics and adjunct therapies (resensitizers) could be commercialized faster than de novo drugs, compressing time‑to‑revenue to 9–18 months. Reaction is likely underdone in the microcap space but overdone in assuming immediate market displacement; safety and systemic metabolism overlap are real risks that could keep valuations subdued until human data. Historic parallel: antibiotic adjuvant plays where small clinical signals triggered outsized M&A despite technical risk.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly positive

Sentiment Score

0.25