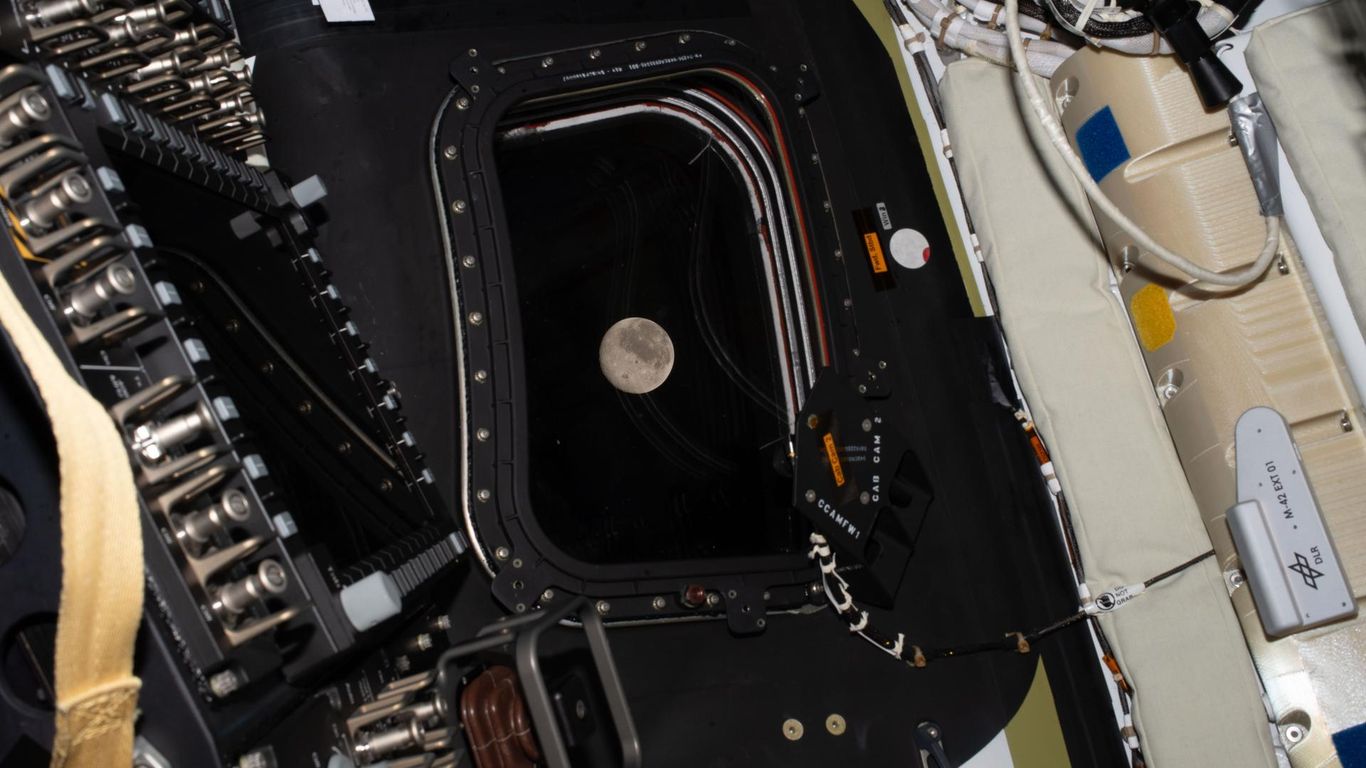

Artemis II set a new human spaceflight distance record, surpassing Apollo 13's 248,655-mile mark and reaching a peak of about 252,760 miles from Earth. The crew begins a seven-hour lunar orbit and observation period, will enter an expected ~40-minute radio blackout on the Moon's far side at 6:44 p.m. ET, and will observe a solar eclipse and attempt a new 'Earthrise' photograph.

A successful high-profile lunar mission materially de-risks the political case for multi-year NASA and DoD adjacent spending: expect program-level budget tailwinds measured in low‑single‑digit billions per year to flow to prime contractors and specialized suppliers over the next 2–5 years. That creates durable backlog that is awarded via multi-year contracts (R&D, production, ground systems) rather than one-off capex, advantaging firms with established Space Act or IDIQ relationships and vertically integrated systems capability. Second-order supply chain winners are not the glitzy consumer-facing names but specialized component and service providers — radiation‑hardened ICs, precision guidance/IMUs, cryogenic turbomachinery, and deep‑space comms/ground-station operators. These components have long lead times and high switching costs, so successful program continuation should translate into margin expansion and more predictable revenue timing for a narrow subset of semiconductor and aerospace suppliers over 12–36 months. Near-term risks are concentrated and binary: a technical setback or a high-profile anomaly would quickly re-price program optionality and slow contract awards (days→weeks of headline volatility, months→years for budget reauthorization). Macro and political risks — a fiscal squeeze or shifting priorities after an election — can reverse the multi-year upside; monitor FY budget markups and key contract award windows as hard catalysts. The market’s consensus focus on media moments and space-tourism narratives misses where durable value accrues. That implies a preferencing of defense primes and mission‑critical component suppliers over consumer/PR plays. Tactical exposure should therefore favor companies with sticky government backlog and engineering leverage rather than names trading on publicity-driven retail interest.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly positive

Sentiment Score

0.25