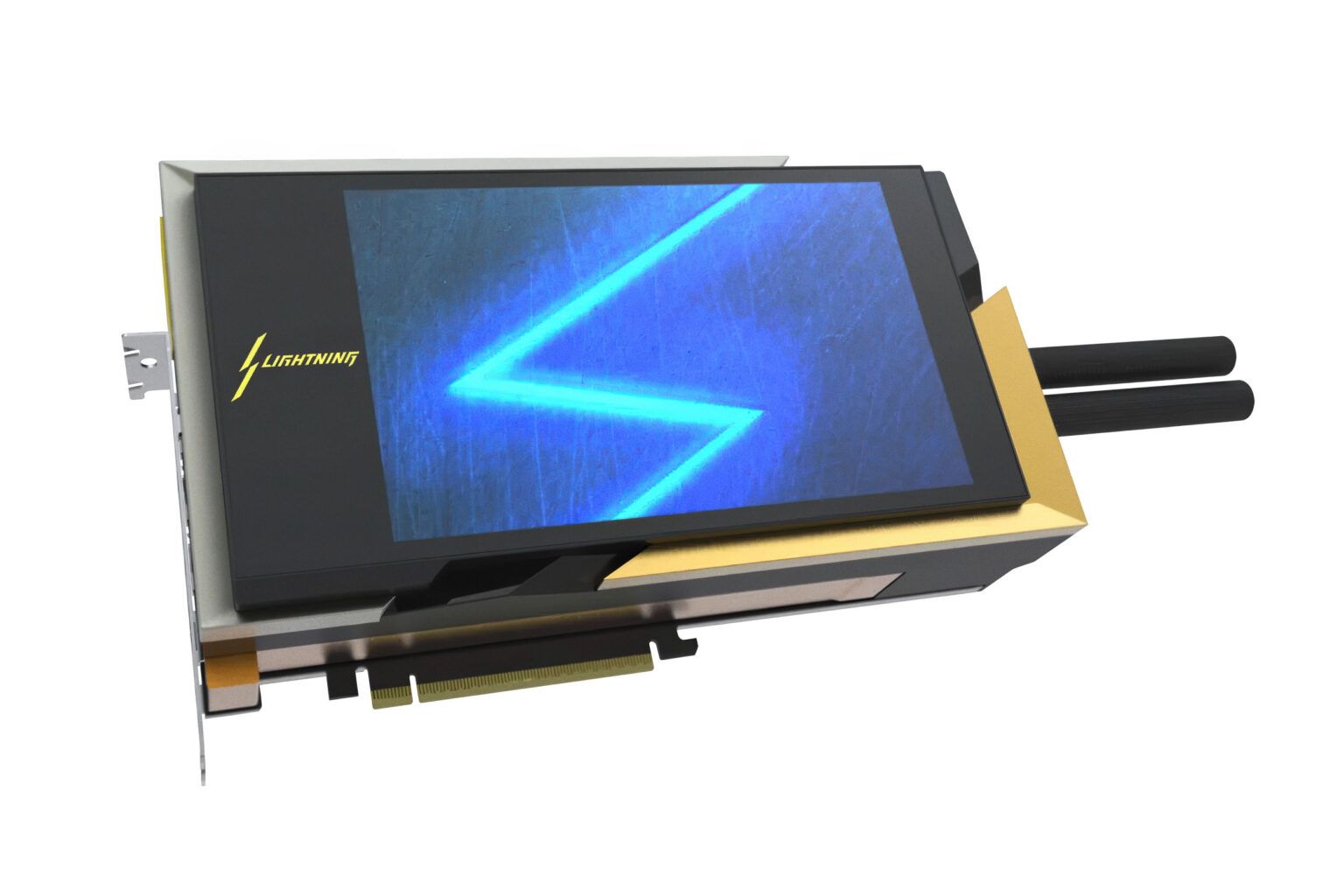

MSI is reviving its high-end Lightning GPU line with an RTX 5090 Lightning revealed via a CES Innovation Awards listing, featuring next‑generation liquid cooling (360mm radiator), a surface-mounted LCD, a companion mobile app, a reinforced PCB with a 40-phase VRM capable of up to 1,600W power delivery (and rumored 2,500W XOC BIOS), and likely 32 GB of GDDR7. The card is positioned for extreme overclockers and is expected to command a premium price (>$4,000) amid DRAM supply pressures, implying limited but high-margin demand that could benefit VRAM and high‑wattage PSU suppliers while having only niche, limited impact on broader public markets.

Market structure: MSI’s 1600W RTX 5090 Lightning is a halo product that boosts OEM ASPs but will account for negligible unit volumes (<~1–3% of board-partner GPU shipments). Winners: NVIDIA (NVDA) platform value capture, high-end DRAM suppliers (Micron MU, Samsung, SK Hynix) and premium PC component makers (MSI 2377.TW, ASUS 2357.TW). Losers: mid/low‑end GPU value segment could see price pressure if R&D and DRAM funnel to premium SKUs; mainstream gamers unlikely to buy at $4k+, so channel demand remains bifurcated. Risk assessment: Key tails — a sudden easing of GDDR7 tightness (30–50% downside to DRAM price squeeze) would compress supplier upside; aggressive energy-regulation or export controls within 3–6 months could dent halo shipments and NVDA channel allocation. Hidden dependency: flagship viability hinges on GDDR7 supply and a stable 16‑pin power ecosystem — shortages or connector failures create product recalls and warranty hits. Catalysts: CES reviews (next 7–30 days), benchmark leaks, and any formal NVDA/Micron supply comments will reprice risk rapidly. Trade implications: Tactical longs: NVDA for platform leverage and MU to play memory tightness; prefer defined‑risk options into near‑term CES volatility. Pair trades: long MU vs short small-cap cooling/PSU manufacturers that may fail to capture premium ASPs. Timeframe: position for 3–12 months for memory-driven moves; expect 5–15% re‑rating potential for MU and 3–8% for NVDA on positive supply comments. Contrarian angles: The market may overestimate volume and underweight cannibalization — historical parallels: RTX 3090 Ti (high ASP, low volume, little long‑term share shift). Mispricing: DRAM suppliers likely already priced some shortage; if DRAM lead times shorten within 90 days, memory longs will be exposed. Unintended consequence: premium arms race raises warranty/returns risk and could compress board‑partner margins if service costs spike.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly positive

Sentiment Score

0.25