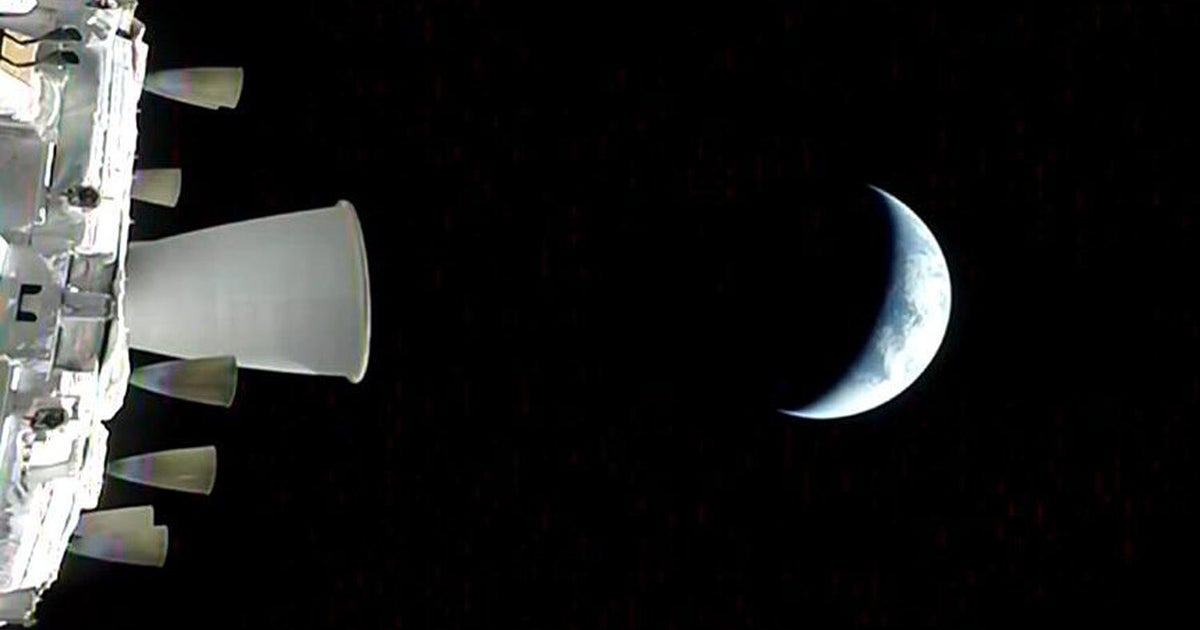

Artemis II completed a successful trans-lunar injection burn (nearly six minutes), boosting speed to 24,500 mph and adding 867 mph at ~115 miles altitude to put Orion on a free-return trajectory. The mission will carry the crew to about 252,455 miles behind the moon as a systems and procedures test for future landings; Orion is built by Lockheed Martin. NASA plans an additional Orion flight (Artemis III) next year to rehearse dockings with SpaceX and Blue Origin landers and says it will spend $20 billion over seven years to increase launch cadence to ~one moon landing every six months. Operationally positive for aerospace contractors, but likely only modest sector-level market effects.

Lockheed Martin is the clear industrial lever here: accelerating lunar cadence creates predictable, multi-year demand for large spacecraft buses, mission systems, and integration work where Lockheed already has secular advantages. The most important second-order effect is capacity bottlenecks in high-precision subcontracting (CNC machining, avionics harnesses, thermal systems) — these suppliers can reprice and expand margins quickly if NASA actually doubles launch cadence, creating outsized profit contribution for primes that secure long-term supplier commitments. Competitors and new entrants face asymmetric execution risk. SpaceX/Blue Origin cost curves and vertical integration can compress margins for traditional prime contractors on commoditized launch services, but primes retain advantage in mission assurance, government relationships, and classified payload work — a bifurcation that should favor diversified contractors with strong integration franchises over pure-play launchers if budgets remain stable. Key risks live in the budget and ops domain: congressional appropriations, a high-profile failure, or rapid price disruption from reusable heavy-lift providers could flip the trade within 12–36 months. Near-term catalysts to watch are formal contracting rounds for lunar lander hardware, FY appropriation releases each March–April, and Artemis III rehearsals next year — any negative read across those three will compress expected upside quickly. The consensus seems to price a steady, uncontested ramp; what is underappreciated is sequencing risk (supplier capacity, award timing) that creates asymmetric windows to monetise growth — if you can provide hardware/testing capacity this cycle, the revenue multiple re-rating will be front-loaded. Conversely, if Congress trims discretionary space budgets, the leverage swings the other way fast because incremental mission funding is lumpy and politically exposed.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly positive

Sentiment Score

0.40

Ticker Sentiment