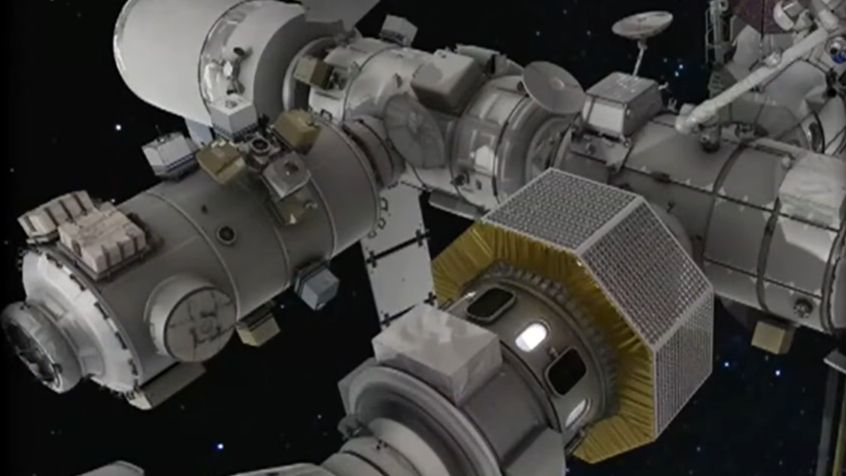

NASA is pausing the planned lunar Gateway orbital station to accelerate focus on a surface lunar base, planning a three‑phase buildout through the end of the decade at an estimated cost of roughly $20 billion. Schedule highlights: Artemis 2 is targeted for April 1 (crewed lunar flyby), Artemis 3 targeted for 2027 for integrated Orion/lander operations in Earth orbit, and Artemis 4 targeted for 2028 as the first landing attempt (without a Gateway rendezvous). Existing Gateway hardware and international partner contributions will be repurposed for surface systems, a shift that could reallocate program work for prime contractors and international partners.

Reprioritizing investment from an orbital hub to surface infrastructure reallocates engineering demand toward precision descent systems, high‑throughput cargo landers and modular habitat integration. That shift favors contractors with end‑to‑end landing experience, high‑margin avionics and power/thermal suppliers, and compresses TAM for firms that built components specific to long‑duration orbital logistics. Expect subcontract and supplier awards to migrate to teams that can scale high‑frequency cargo deliveries within 12–36 months; firms with flexible manufacturing and commercial launch partnerships will capture outsized share.

Budget realignment raises two second‑order supply‑chain effects: (1) inventory of near‑completion orbital hardware becomes a bargaining chip for primes and governments, potentially accelerating M&A or offset contracts; (2) rapid surface cadence increases demand for radiation‑hardened electronics and deployable power systems, tightening niche semiconductor and battery supply lines and creating 6–18 month bottlenecks. These pinch points will drive margin expansion for specialized suppliers but also elevate execution risk if launch cadence slips.

Key tail risks are political funding shifts (electoral cycles) and a test‑flight failure that could force multi‑year program delays — both can flip positive sentiment to negative within weeks. Conversely, a flawless demonstration mission in the next 6–18 months would re‑rate contractors exposed to lander and cargo manifests. The smart play is to lean into high‑quality primes and vertical‑specialists with visible backlog while hedging program execution risk through options or pairs that short pure‑play orbital suppliers whose market relevance is diminished by the strategic pivot.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

neutral

Sentiment Score

0.05