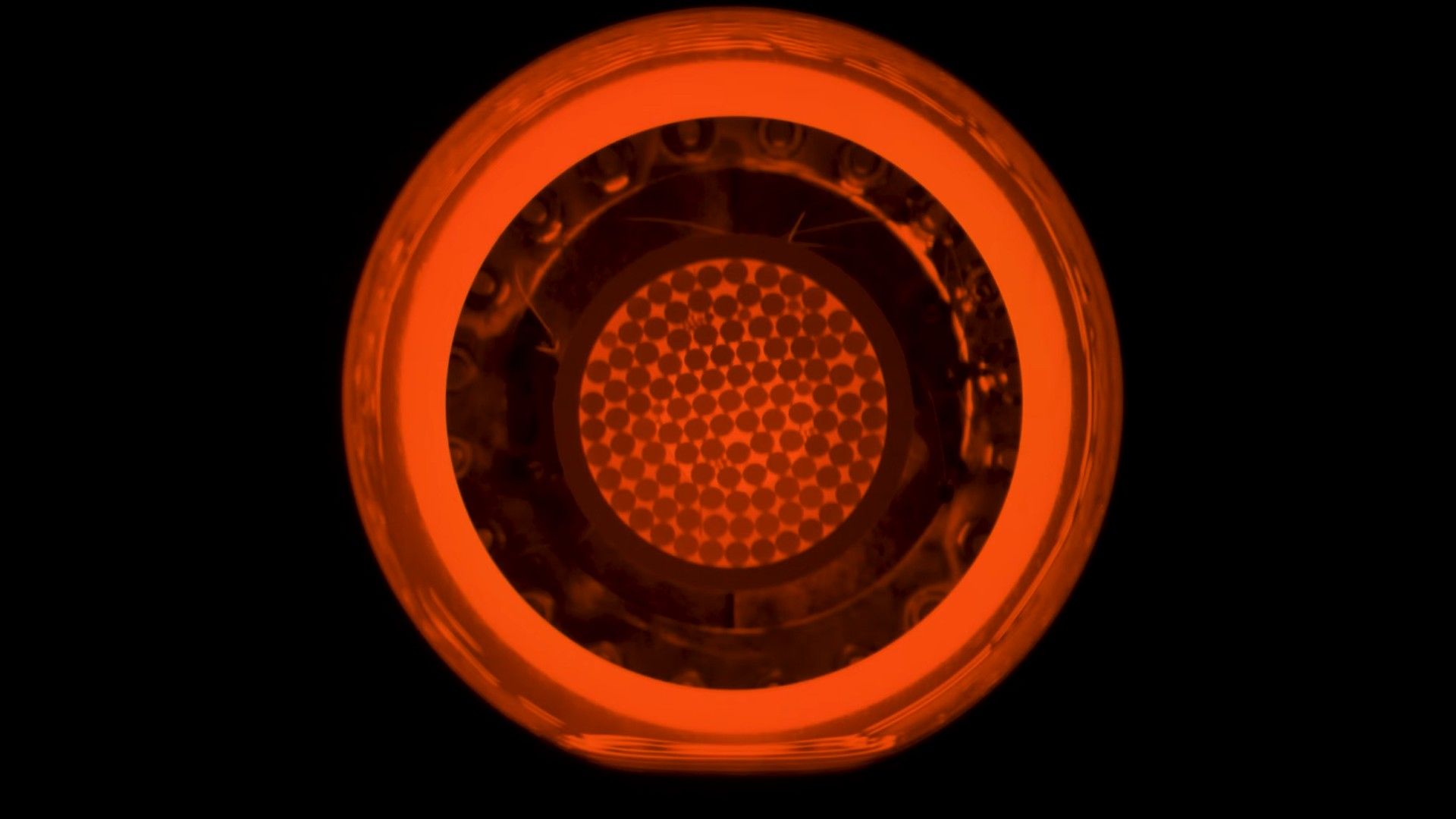

NASA's new lithium-fed magnetoplasmadynamic thruster reached 120 kilowatts in its first lab test, matching 25 times the power of the agency's current state-of-the-art ion engine. The prototype is part of longer-term efforts to scale ion propulsion toward 500 kilowatts to 1 megawatt, with future concepts tied to nuclear-powered space systems for Mars missions. The article is primarily a technology milestone with limited near-term market impact, but it underscores continued U.S. investment in advanced space propulsion.

This is less a near-term stock catalyst than a signal that the supply chain for deep-space propulsion is moving from science project to programmatic procurement. The real inflection is not the lab firing itself; it is that high-power electric propulsion now has a credible scaling path, which should incrementally expand budgets for power electronics, thermal management, vacuum test infrastructure, and space-rated materials long before human Mars missions become relevant. That means the earliest monetization is likely in defense, cislunar logistics, and high-value science missions, not Mars headlines. The key second-order effect is that nuclear space power becomes the gating item, not the thruster. If that ecosystem advances, the beneficiaries are companies with reactor-adjacent expertise, space-qualified power conversion, and long-duration thermal systems; if it stalls, the thruster work remains a technology demonstrator with limited addressable revenue. For the broader market, this is mildly supportive of the space infrastructure theme but not enough to change public-equity fundamentals on its own because adoption cycles are measured in years and depend on government capex, certification, and launch cadence. The contrarian read is that investors may overreact by bidding up every “space” name, when the bottleneck is actually systems integration and mission assurance rather than propulsion horsepower. The more actionable thesis is a basket focused on enabling hardware with visible non-space revenue, since those names can monetize the same capabilities in defense, industrial power, and grid electronics while retaining upside optionality if space programs scale. The main tail risk is political budget slippage or a reactor-related delay, either of which would push meaningful revenue out by 3-5 years and compress enthusiasm quickly.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

moderately positive

Sentiment Score

0.45

Ticker Sentiment