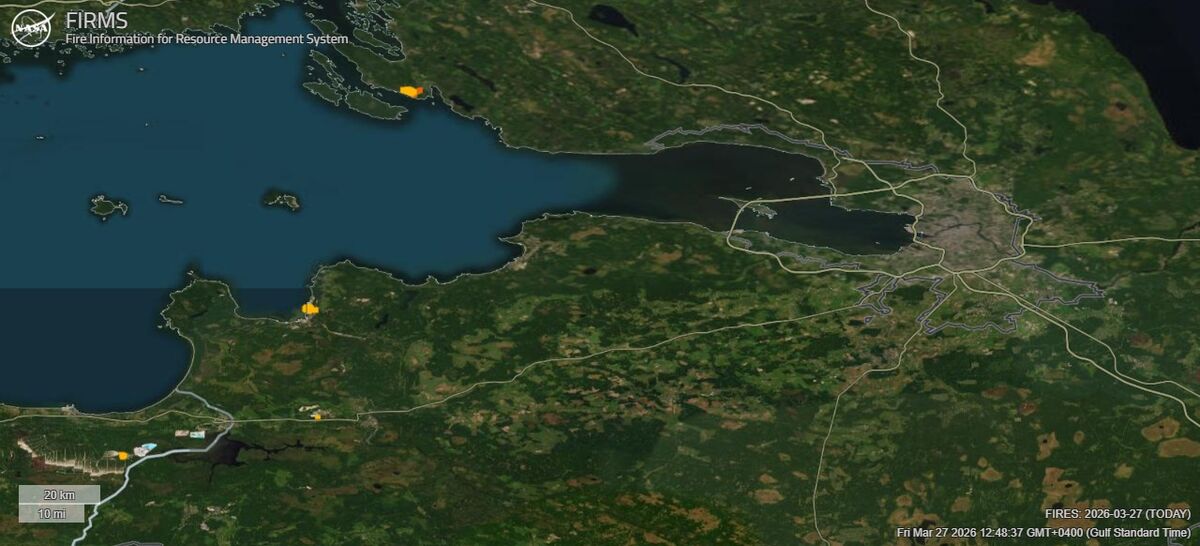

Two major Russian Baltic oil export terminals, Primorsk and Ust-Luga, are reported on fire after overnight drone attacks; NASA FIRMS satellite imagery shows blazes that began 3–12 hours before detection. The strikes risk disrupting crude and refined product flows through the Baltic, potentially tightening supply and putting upward pressure on regional oil prices and freight rates depending on outage duration. Monitor official port closures, repair timelines and tanker rerouting for impact on energy markets and logistics.

Disruptions to northwest export corridors materially raise the volatility of seaborne crude and refined product flows into Northern Europe, compressing optionality for refiners and logistics planners. Expect freight and war-risk insurance premia to reprice within days (spiking 2x-4x) and for physical sellers to favor larger, longer-haul cargoes — a mechanics that typically props up tanker spot rates and western Atlantic crude differentials for 2–12 weeks. Over 3–9 months, market responses bifurcate: buyers either draw local inventories and pay up for prompt barrels (supporting regional cracks) or shift to alternate supply routes (pipelines, Black Sea, North African cargoes), which dampens the price impulse but raises structural transshipment and insurance costs.

Two non-obvious second-order winners are: (1) owners of flexible mid-size tankers and time-charter providers who capture premium for short-notice re-routing, and (2) refiners and traders who can arbitrage increased Brent–Urals/dated differentials by owning storage or booking longer forward freight; both profit from widened basis volatility even if absolute volumes normalize. Conversely, fixed-cost coastal logistics (terminals, local barge fleets) and any counterparties with short physical coverage in the Baltic are exposed to outsized margin squeeze and forced substitution risk.

Tail risks sit in escalation and policy reaction — a marked closure of adjacent choke points or unilateral export bans would shift the shock from weeks to years of structural reallocation, whereas rapid security remediation or large strategic releases of crude could reverse price moves in 1–3 weeks. The consensus is pricing this as a short-lived logistical premium; however, the realistic path is a multi-month regime of higher structural costs for Baltic/NE Atlantic shipments driven by insurance and detour inefficiencies unless diplomatic/operational fixes are swift.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

strongly negative

Sentiment Score

-0.65