Construction firm Tutor Perini (TPC) has seen its shares rise 14.3% over the past month, significantly outperforming the S&P 500, following strong last reported quarter results that included a 386.21% EPS surprise and 11.55% revenue beat. This performance is underpinned by substantial upward revisions to future earnings estimates, with current fiscal year EPS now projected to increase 186.9% year-over-year, earning TPC a Zacks Rank #1 (Strong Buy) rating. Furthermore, the company's valuation is assessed as trading at a discount to its peers, potentially attracting further investor attention.

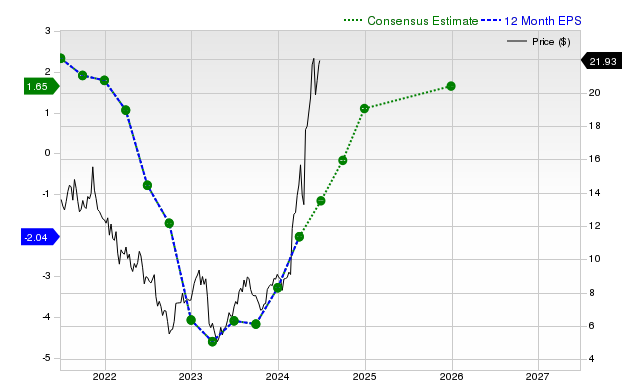

Tutor Perini Corporation (TPC) has demonstrated significant positive momentum, with its shares returning +14.3% over the past month, substantially outperforming both the S&P 500 composite's +2% gain and its heavy construction industry peers' +10.8% gain. This price action is underpinned by robust operational performance, highlighted by the last reported quarter's revenue of $1.37 billion (+21.8% YoY) and an EPS of $1.41, which constituted a massive +386.21% surprise over consensus estimates. The core driver of the bullish outlook is the sharp upward revision in earnings estimates by sell-side analysts. The consensus EPS estimate for the current fiscal year has been revised up by +116.6% over the last 30 days to $2.72, implying a +186.9% year-over-year growth. This trend is projected to continue, with next year's EPS forecast at $3.97, a +46% increase. This powerful revision trend, combined with strong revenue growth forecasts of +20.6% for the current year and +16.9% for the next, has earned the stock a Zacks Rank #1 (Strong Buy). Furthermore, despite the recent rally, the stock is graded 'B' for value, indicating it trades at a discount to its peers, suggesting potential for further appreciation.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

strongly positive

Sentiment Score

0.80

Ticker Sentiment