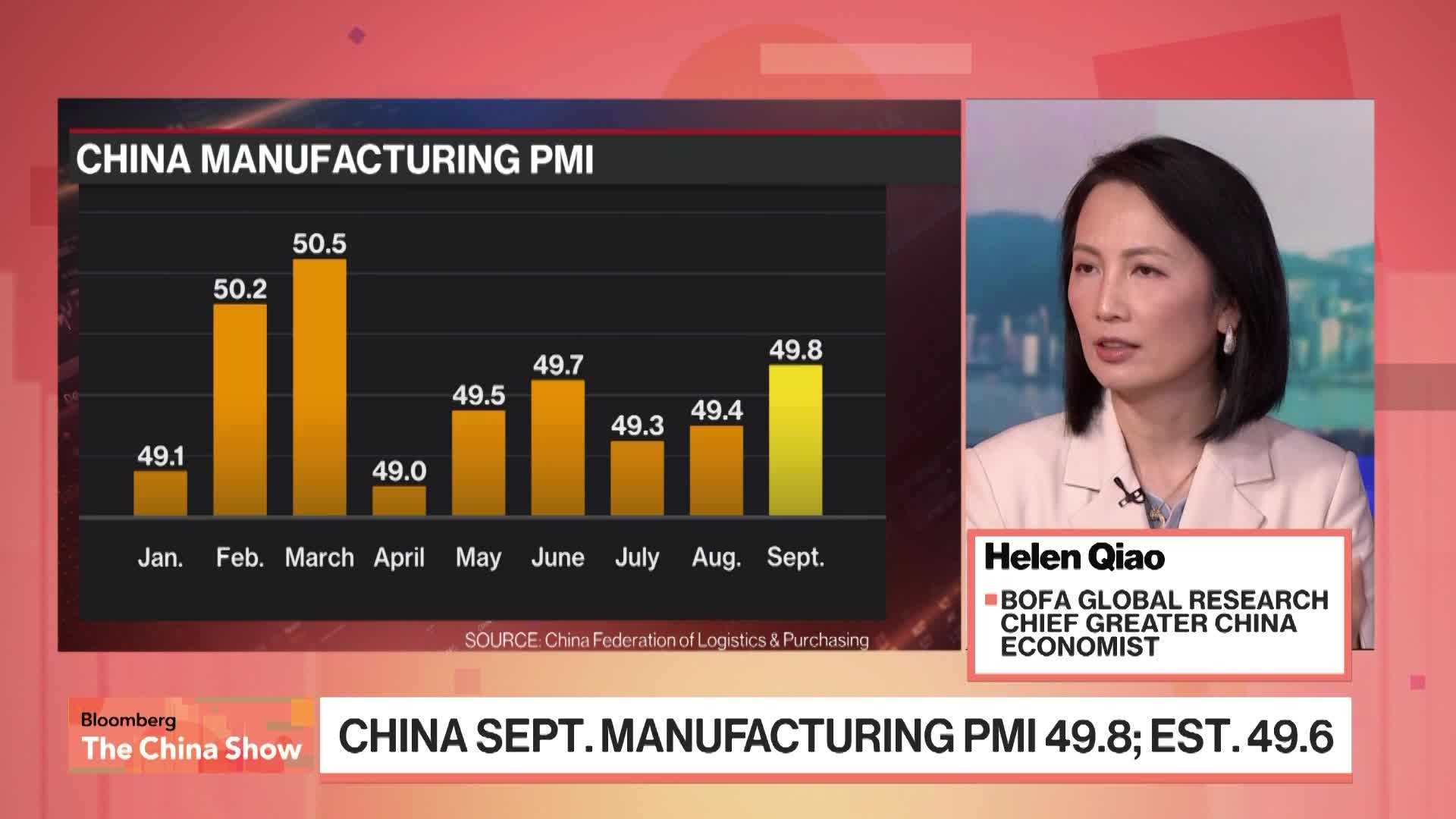

Despite China's official manufacturing PMI extending its contraction to a sixth consecutive month at 49.8, policymakers are reportedly not rushing to implement significant stimulus measures. According to Helen Qiao, Chief Greater China Economist at BofA Global Research, this cautious approach is due to the current resilience observed in industrial production and the labor market, suggesting a measured response to ongoing economic pressures.

China's manufacturing sector continues to signal contraction, with the official purchasing managers' index (PMI) at 49.8, extending its decline for a sixth consecutive month. Despite this persistent weakness, insights from BofA Global Research suggest that Chinese policymakers are not poised to implement large-scale stimulus measures imminently. This policy restraint is attributed to the perceived resilience in other core economic pillars, namely industrial production and the labor market, which are reportedly holding up well. The government's approach appears to be one of measured observation, balancing the clear downturn in manufacturing against stability elsewhere in the economy, implying that the threshold for aggressive intervention has not yet been met.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mixed

Sentiment Score

-0.10

Ticker Sentiment