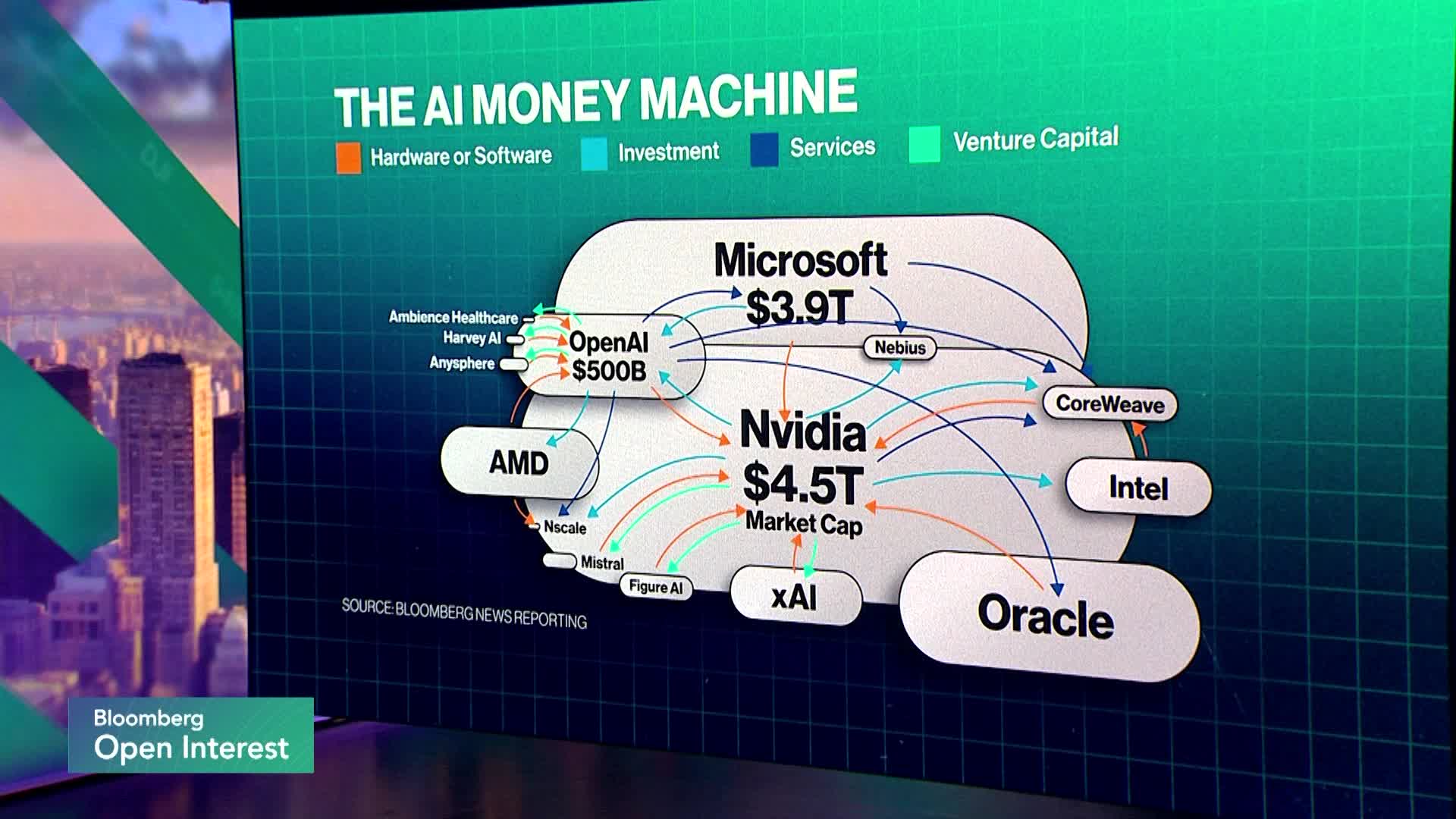

Nvidia has taken a small equity stake (reported around 2–3%) in Synopsys, a leading chip-design software provider, after buying shares at $414.79 and with the stock trading near $440 as it jumped roughly 5%. The move continues Nvidia's playbook of strategic minority investments (previously in Intel and Nokia) aimed at engineering partnerships and potential sales channel benefits for its GPUs; the discussion notes Synopsys’s software runs broadly across chip designers and can be optimized on Nvidia hardware. Market context: Nvidia remains supply-constrained but dominant (~90% share) in GPUs powering AI workloads, preserving high margins and limiting near-term pricing pressure despite competitive activity from Google's TPU efforts.

Market structure: NVIDIA (NVDA) and upstream foundries (TSM) and EDA vendors (Synopsys/SNPS) are primary beneficiaries as GPU-driven design-to-fab workflows lock customers into stacked ecosystems; NVDA still controls ~90% of the datacenter GPU market so pricing power and gross margins remain intact near current levels. Direct losers: cloud incumbents (GOOGL) if they fail to monetize TPUs at scale and any CPU incumbents losing share to accelerated compute; semiconductor cyclical suppliers (memory, HBM) should see demand pick up, supporting limited commodity upside for HBM and copper for fabs over 12 months. Risk assessment: Tail risks include an antitrust/regulatory probe into NVDA’s ecosystem or forced divestitures (probability medium, impact high) and a successful rapid outsized TPU landing by GOOGL or AWS (low-probability, high-impact). Near-term (days–weeks) expect headline-driven 2–8% swings; medium-term (3–12 months) risk centers on TSMC capacity guidance and NVDA earnings vs. sell-through; long-term (1–3 years) is a technology migration battle (GPU vs TPU) that will alter margins and share. Trade implications: Tactical: establish a 2–3% portfolio long in NVDA over 6–12 months, hedged with a 3-month 5–10% OTM put or a collar to cap drawdowns; buy TSM 1–2% overweight for foundry leverage with add-on on >8% pullback. Relative: run a pair trade long NVDA / short GOOGL sized to be delta-neutral (target 0.25–0.5% portfolio risk) for 3–6 months, unwind if NVDA guidance misses by >5% or if GOOGL announces 3+ large TPU third-party deals. Contrarian angles: The market underestimates governance/regulatory friction from NVDA’s equity-stake playbook—the SoftBank liquidity example shows forced selling can amplify volatility; conversely the market underprices persistent supply constraint: NVDA can sell every GPU TSMC delivers so upside persists absent node-scale competition. Historical parallel: dominant infrastructure suppliers (e.g., Intel in 2000s) fell after capacity/architecture missteps; watch 4–8 quarter share trends, not single quarters, before rotating aggressively into/away from NVDA.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately positive

Sentiment Score

0.40

Ticker Sentiment