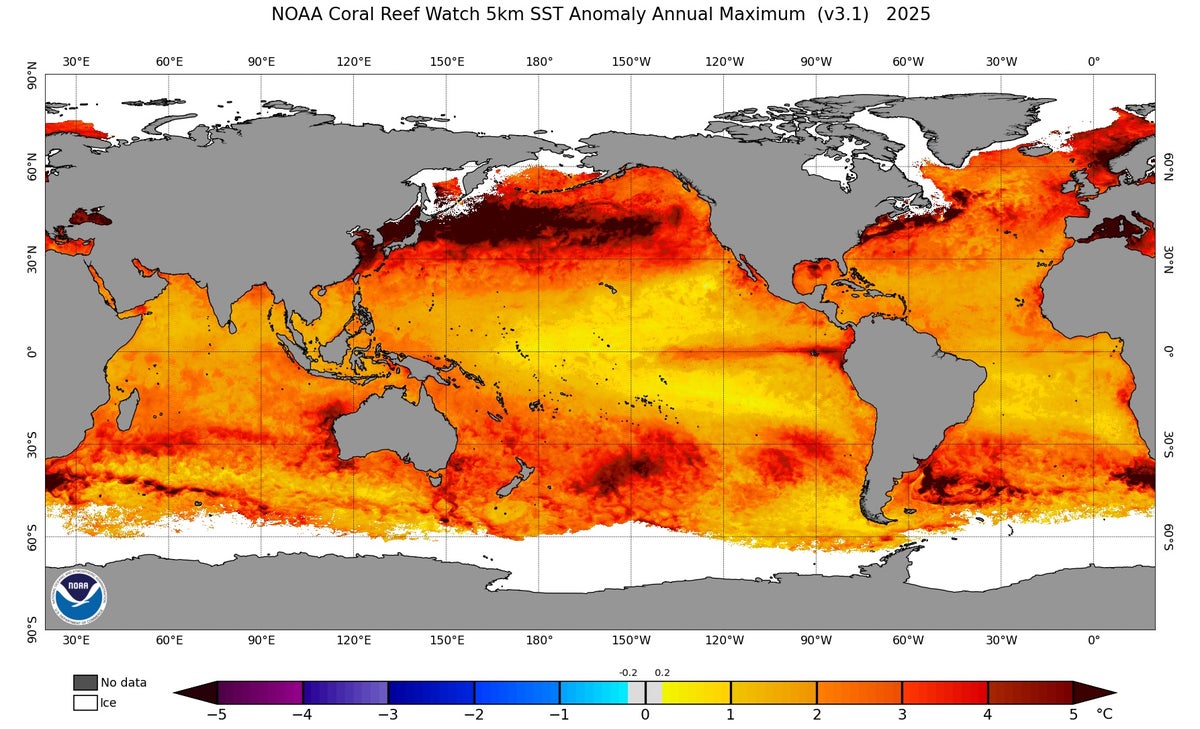

New international research published in Advances in Atmospheric Sciences shows the world’s oceans stored a record amount of heat in 2025, with the upper 2,000 meters absorbing 23 zettajoules more energy than in 2024—about 37 times 2023 global energy consumption—and average sea surface temperatures ~0.5°C above the 1981–2010 average. Researchers warn that since oceans absorb roughly 90% of excess greenhouse heat, the trend will drive sea-level rise, ecosystem disruption and more extreme weather, raising long-term risk for insurers, coastal real estate, agriculture and energy markets and increasing pressure for climate mitigation and adaptation investments.

Market structure: Hotter oceans steepen demand for climate-resilience capex (grid hardening, desalination, coastal defenses) benefiting renewable developers, water-tech and engineering firms (12–36 month revenue runway). Insurers and coastal real-estate-related sectors face margin compression as reinsurance pricing and loss frequency rise; expect selective pricing power gains for specialist contractors and battery/distributed energy suppliers. Risk assessment: Tail risks include a single catastrophic season (> $100bn insured losses) or rapid regulatory shocks (US/EU carbon or coastal zoning reforms) that could re-rate insurers and muni credits within 3–12 months. Hidden dependencies include municipal tax bases and mortgage exposure on coastal strip: rising SLR/heat materially raises credit stress for coastal muni bonds over 2–7 years. Catalysts: next 6–12 months of NOAA hurricane metrics, major climate legislation, and the 2026 earnings season for insurers. Trade implications: Tactical long exposure to solar, storage and water-infra names with 12–24 month horizons, while hedging insurer/reinsurance tail risk via puts or CAT allocations, is asymmetric. Cross-asset: expect upward pressure on catastrophe bond yields, selective widening of coastal muni spreads vs. core munis, and increased summer gas/energy volatility (trade seasonally for summer 2026). Contrarian angles: Consensus underprices durable demand for water/desalination — a 10–25% higher capex cycle is plausible over 3 years; conversely broad shorting of utilities is likely overdone because regulated utilities will pass through resilience costs. Historical parallel: post-Katrina reinsurance repricing (multi-year) suggests early active positions in specialty contractors and CAT exposure are higher-conviction plays.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately negative

Sentiment Score

-0.50