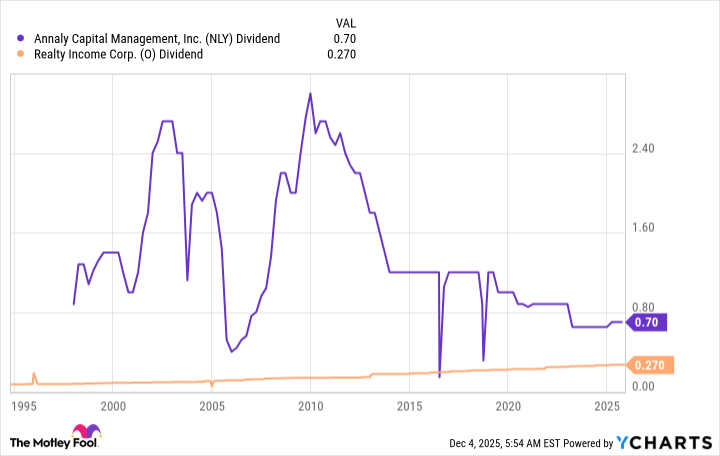

Annaly Capital (an mREIT) offers a very high ~12%+ dividend yield but its payouts have been highly variable due to the mark-to-market nature and self-amortizing characteristics of mortgage-backed securities, which are sensitive to interest rates, prepayments and housing dynamics. By contrast, Realty Income (a property-owning net-lease REIT) yields roughly 5.6%, operates a 15,000+ property portfolio, and has raised its dividend for 30 consecutive years, making it a more reliable cash-income choice for retirees while Annaly may be better suited to investors targeting total return with dividend reinvestment.

Market structure: Mortgage REITs (NLY) and net-lease/property REITs (O) attract different flows — yield chasers and total‑return allocators respectively. NLY’s ~12% yield (vs. O ~5.6% and S&P 1.2%) signals higher coupon income but much higher sensitivity to mortgage spreads, prepayment speed, and funding costs; Realty Income benefits from stable rent rolls and predictable dividend growth, limiting downside in a risk‑off move. Risk assessment: Immediate risk (days) is funding/hedge volatility (SOFR spikes, repo squeezes); short term (weeks–months) is mortgage spread widening or prepayment shocks that can force NLY dividend cuts; long term (quarters–years) is secular cap‑rate shifts and tenant credit cycles that erode O’s growth runway. Tail scenarios include a sharp 100–200bp move in rates or a housing stress event that triggers margin calls on mREIT leverage and >30% equity drawdowns. Trade implications: Tactical capital should favor O for income stability and defensive allocation, while NLY is an opportunistic, small‑sized total‑return play with strict NAV/coverage entry rules. Use pair trades (long O / short NLY) to isolate business‑model risk, and options to monetize yield on O (covered calls) while buying downside protection on NLY (put spreads). Contrarian angles: The market under‑prices scenario where Fed cuts compress mortgage spreads and accelerates prepayments — that would lift NLY materially (20–40% potential if spreads retrace). Conversely, consensus underestimates operational leverage in NLY (repo + hedges); dividend stability is a real, monetizable premium for O that likely persists unless cap rates rise >150bp.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

mildly positive

Sentiment Score

0.25

Ticker Sentiment