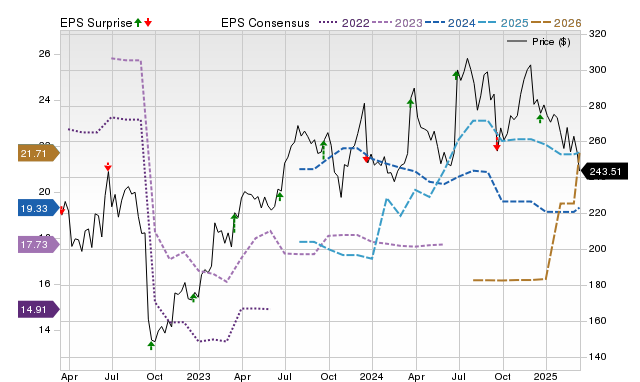

FedEx (FDX) is slated to report earnings next week, with consensus estimates projecting $3.68 EPS (+2.2% YoY) and $21.78 billion revenue (+0.9% YoY) for the quarter ended August. However, the consensus EPS estimate has seen a slight downward revision of 0.33% over the last 30 days. Critically, the company's Zacks Earnings ESP of -6.97%, combined with a Zacks Rank of #3, indicates that FedEx is not a compelling candidate for an earnings beat, suggesting limited upside from a positive surprise.

FedEx (FDX) is approaching its September 18 earnings release with consensus expectations pointing to modest year-over-year growth. Wall Street anticipates quarterly earnings of $3.68 per share, a 2.2% increase, on revenues of $21.78 billion, a 0.9% increase. However, sentiment among analysts appears to be deteriorating, evidenced by a 0.33% downward revision of the consensus EPS estimate over the past 30 days. More significantly, the proprietary Zacks Earnings ESP (Expected Surprise Prediction) is a negative 6.97%, indicating that the most recent analyst estimates are more bearish than the broader consensus. While the stock holds a Zacks Rank of #3 (Hold), the combination with a negative ESP makes it difficult to predict a positive earnings surprise. The company's track record is also inconclusive, having beaten consensus EPS estimates in only two of the last four quarters. Consequently, the quantitative signals suggest FedEx is not a compelling candidate for an earnings beat, shifting the focus for potential stock movement to management's forward-looking guidance on the earnings call rather than the headline results themselves.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly negative

Sentiment Score

-0.25

Ticker Sentiment