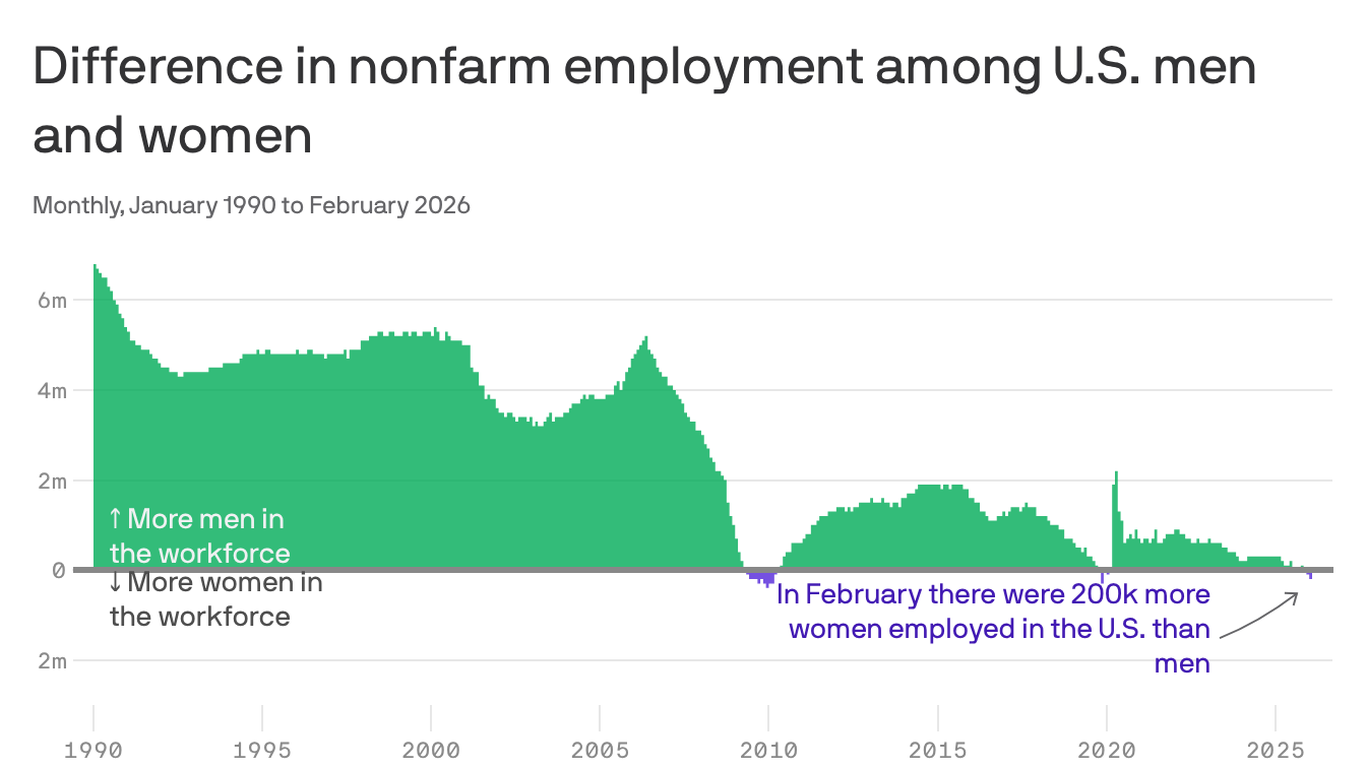

For only the third time ever, there are more women employed in the U.S. than men, driven partly by a 142,000 decline in male employment from Feb 2025 to Feb 2026. Job growth is concentrated in health care (female-dominated) while construction and manufacturing have been flat or negative, shifting the employment mix toward lower-paying occupations and likely weighing on average wages. Immigration enforcement has reduced male labor supply, and cultural/occupational barriers are limiting male transitions into growing HEAL (health, education, literacy) roles. The trend raises downside risk to wage growth and highlights sectoral labor shortages in health and education.

The labor-force gender mix shift has an underappreciated effect on sectoral unit economics: as health-and-education employment scales, pay pressure will concentrate in roles with high patient-contact and credential premiums, while aggregate headline wage growth can drift lower. That divergence creates a two-speed inflation picture — goods prices soften while localized services inflation (home health aides, niche therapists) outpaces, compressing payer margins and boosting specialized staffing vendors' billing rates over a 6–18 month window.

A durable cultural tilt that keeps men out of certain occupations will accelerate capital substitution in blue-collar tasks where supply is shrinking — expect faster adoption of modular construction, telemedicine automation for diagnostics, and labor-saving robotics over 12–36 months. This is a structural capex tailwind to industrial automation OEMs and software platforms that monetize projectization of once-labor–intensive workflows, even if headline construction/manufacturing volumes remain muted.

Policy is the main swing factor: immigration or targeted re-skilling initiatives could reroute these flows within quarters; absent that, the market will reprice around higher unit labor costs in health/social care. Cultural change is slow, so most tactical alpha is in companies that capture margin uplift (specialized staffing, telehealth platforms, automation enablers) rather than broad consumer plays that assume a quick reversal of workforce composition.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

neutral

Sentiment Score

0.00

Ticker Sentiment