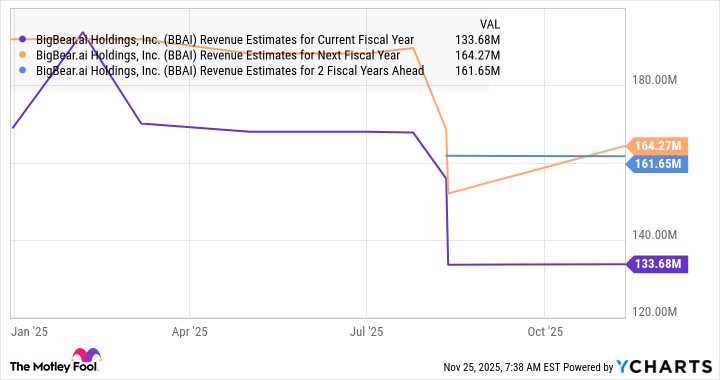

BigBear.ai’s results show weakening fundamentals: revenue for the first nine months of 2025 fell ~12% to just over $100M (2024 revenue was $158M) and the company cut full-year guidance from $160–$180M to $125–$140M amid timing uncertainty in federal contracts. Last quarter it posted an adjusted EBITDA loss of $9.4M and a $376M backlog, yet the stock has rallied and management is pursuing a $250M acquisition of Ask Sage (ARR $25M, 6x YoY) to try to restore growth. Analysts expect revenue to decline in 2025, recover in 2026, but show little growth in 2027; even a hypothetical 20% 2028 rebound to ~$194M implies a CAGR (~13%) that may not justify BigBear.ai’s $2.74B market cap versus lower market multiples. The combination of weak near-term results, reliance on government contracting, and a large strategic acquisition makes this a company-specific, high-attention but fundamentally cautious investment case.

Market structure: BigBear.ai (BBAI) remains a small, government-centric AI player with $~100M LTM revenue (9M 2025) and a $376M backlog versus Palantir’s $8.6B backlog; the $250M Ask Sage buy (ARR $25M) shifts revenue mix negligibly but concentrates government/regulated exposure. Winners: niche defense AI integrators, cloud vendors (AWS/Azure) hosting classified workloads, and Palantir (PLTR) as a scaled commercial/government hybrid. Losers: small-cap pure-play govtech names that cannot finance aggressive M&A; BBAI’s current market cap $2.74B implies >14x revenue vs. Nasdaq’s 5.4x — pricing power looks overstretched absent clear 2026+ growth acceleration. Risk assessment: Tail risks include loss/non-award of major federal contracts, a dilutive equity raise to fund integration ($250M cash/stock), or a cybersecurity/regulatory breach affecting DoD approvals. Immediate (days): elevated IV and trading volume around deal financing disclosures; short-term (weeks–months): integration KPIs, ARR retention from Ask Sage, Q4 guidance; long-term (3+ years): need ~13% CAGR to justify current cap absent multiple expansion. Hidden dependencies: federal budget timing, prime contractor relationships, and Ask Sage key-person retention. Trade implications: Implement a relative-value pair: short BBAI (1.5% portfolio NAV) and long PLTR (1.5% NAV) to capture divergence—PLTR has 60%+ recent growth and much larger backlog. Hedge entry with BBAI 3–6 month put spread (buy 1x 15% OTM put, sell 1x 30% OTM put) sized to cover short notional. Rotate 1–2% of equity from small-cap govtech into large-cap AI/defense (PLTR, LMT, MSFT) to reduce idiosyncratic funding risk. Contrarian angles: The market may be underpricing upside if Ask Sage retains >80% ARR and BBAI converts 30–40% of federal pipeline to awards, which would materially raise 2026 revenue above consensus; conversely, the biggest mispricing risk is forced dilution—if BBAI issues >$200M equity, current thesis breaks. Set re-rate triggers: add to longs if BBAI posts sequential revenue beat >10% QoQ or backlog >$600M within 12 months; tighten shorts if acquisition funding is non-dilutive and ARR retention >90% after 12 months.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately negative

Sentiment Score

-0.45

Ticker Sentiment