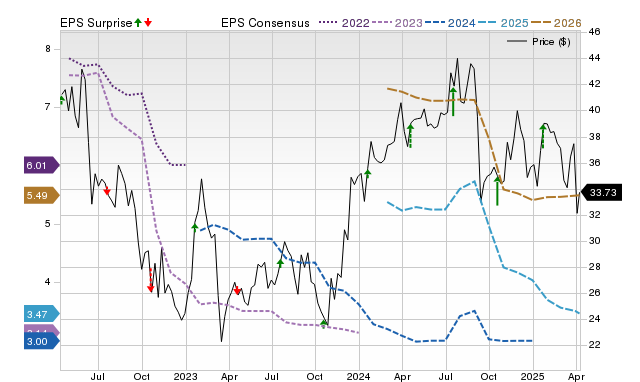

Ally Financial (ALLY) is scheduled to report its Q2 2025 earnings on July 18, with Wall Street anticipating $0.78 EPS, a 19.6% year-over-year decline, on revenues of $2.03 billion, up 1.5%. Despite the projected earnings decrease, the company holds a positive Zacks Earnings ESP of +3.53% and a Zacks Rank #3, strongly suggesting it will likely surpass the consensus EPS estimate. This outlook is reinforced by Ally's consistent history of beating EPS expectations in the past four consecutive quarters, positioning it as a compelling candidate for an earnings beat that could influence its stock performance.

Ally Financial (ALLY) is positioned for a potentially positive near-term catalyst despite a challenging underlying fundamental outlook ahead of its Q2 2025 earnings report on July 18. Wall Street consensus anticipates a significant 19.6% year-over-year decline in earnings to $0.78 per share, contrasted by a modest 1.5% revenue increase to $2.03 billion. While the consensus EPS estimate has been revised downward by 1.58% over the last 30 days, more recent analyst activity indicates a bullish shift. This is captured by a positive Zacks Earnings ESP of +3.53%, which, when combined with the stock's Zacks Rank #3 (Hold), suggests a high probability of an earnings beat. This quantitative signal is further supported by the company's strong track record, having surpassed consensus EPS estimates in each of the last four quarters, including a notable 34.88% surprise in the prior quarter. The primary tension for investors is the divergence between the expected year-over-year profit contraction and the high likelihood of the company exceeding current, potentially conservative, market expectations.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately positive

Sentiment Score

0.60

Ticker Sentiment