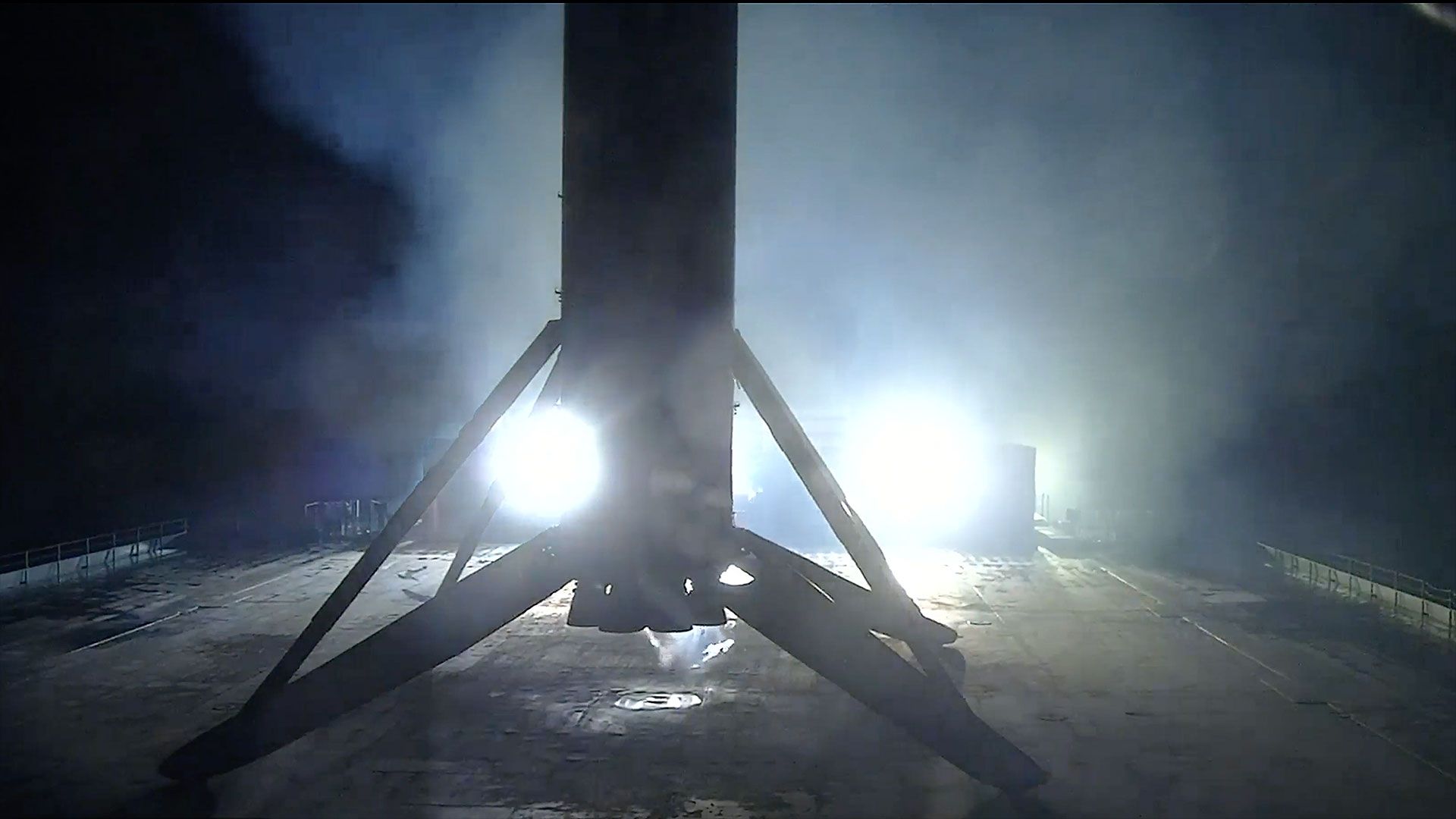

SpaceX successfully landed a Falcon 9 first stage on the droneship Just Read the Instructions in Exuma Sound, The Bahamas, following a Feb. 19 launch from Cape Canaveral that lofted 29 Starlink satellites; the booster (designated 1077) completed its 26th touchdown. The Civil Aviation Authority of The Bahamas recently greenlit a resumption of rocket recoveries in the region after an environmental assessment triggered by debris from a prior Starship upper-stage breakup; the Falcon 9 upper stage was on track to deploy the satellites about 64 minutes after liftoff, adding to the roughly 9,700-strong Starlink constellation.

Market structure: SpaceX’s resumed Bahamas drone-ship landings and continued Starlink deployments favor low-cost, high-frequency launch economics and operators of satellite payloads and components. Winners: space-system suppliers (L3Harris LHX, RTX) and satellite-component/antenna makers that can scale with Starlink; losers: niche launch providers (RKLB) and consumer/broadband incumbents exposed to Starlink competition (VSAT, to a lesser extent T, VZ). Expect downward pressure on per-launch pricing and secondary-market launch utilization rates; conservatively model a 10–30% effective drop in marginal launch revenue for alternatives over 12 months. Risk assessment: Key tail risks include a renewed Bahamas or other jurisdictional ban (10–15% probability) that forces costly reroutes (+$5–20M per mission) and multi-month schedule slips, and a regulatory clampdown on megaconstellations in the US/EU (5–10% over 12–24 months) that could slow Starlink rollouts. Hidden dependencies: supply-chain concentration for high-volume avionics and phased-array terminals (single-supplier shocks would amplify costs). Catalysts to monitor: Bahamas regulatory updates (next 30–90 days), FCC filings, and SpaceX launch cadence metrics. Trade implications: Favor equities of large defense/space suppliers with diversified government and commercial backlogs: establish 2–3% long LHX targeting 12–20% upside in 6–12 months; pair that with a 1–2% short of VSAT (or buy VSAT 3-month 10% OTM puts) expecting 15–25% downside in 3–6 months as consumer broadband pricing faces pressure. Use options to hedge: buy 6-month ATM calls on RTX sized to 1–2% portfolio risk and buy VSAT 3-month puts (10% OTM) to protect downside. Contrarian angles: The market underestimates demand elasticity where cheaper launches unlock new payload classes (IoT, small SAR, low-latency enterprise comms) — incumbents like MAXR and IRDM could see incremental TAM upside; consider a small 0.5–1% tactical long in MAXR/IRDM with 12–18 month horizon. Conversely, consensus may over-penalize RKLB; avoid large outright shorts without volatility hedges until quarterly revenue guidance confirms margin stress.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly positive

Sentiment Score

0.27