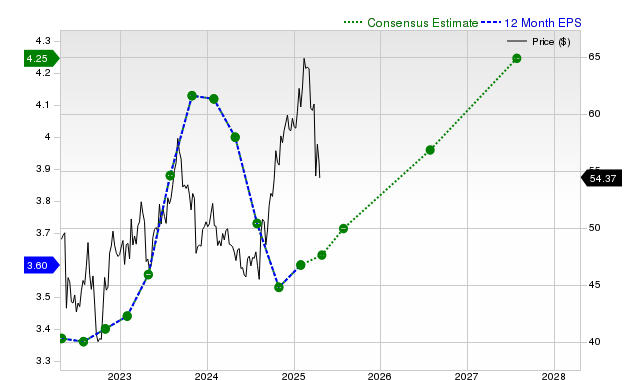

Cisco Systems (CSCO) is attracting investor attention, despite its recent one-month return of +0.9% underperforming the S&P 500 and its industry. The company projects modest year-over-year growth in both earnings and revenue for the current and next fiscal years, with slight positive revisions to estimates over the past month. While Cisco has consistently surpassed consensus EPS and revenue estimates for the last four quarters, its Zacks Rank #3 (Hold) suggests it may perform in line with the broader market, and its 'D' grade on the Zacks Value Style Score indicates it is currently trading at a premium relative to peers.

Cisco Systems (CSCO) presents a mixed but stable fundamental picture, characterized by consistent operational execution against a backdrop of modest growth expectations and a premium valuation. The company has a strong track record, having beaten both consensus EPS and revenue estimates for the last four consecutive quarters, with the most recent report showing a +2.06% EPS surprise and a +0.47% revenue surprise. Looking forward, analyst consensus projects steady, mid-single-digit growth; revenue is forecasted to grow +5.2% in the current fiscal year and +4.2% in the next, while EPS is expected to increase by +6.0% and +7.4% over the same periods. These estimates have seen minor positive revisions over the last 30 days. However, this fundamental stability is not translating into market outperformance, as the stock's +0.9% return over the past month significantly lags the S&P 500's +3.6% gain. This underperformance may be explained by its valuation, as the stock's Zacks Value Style Score of 'D' indicates it is trading at a premium to its peers, which, combined with a neutral Zacks Rank #3 (Hold), suggests the market anticipates its performance will be in line with, not ahead of, the broader market.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

neutral

Sentiment Score

0.10

Ticker Sentiment