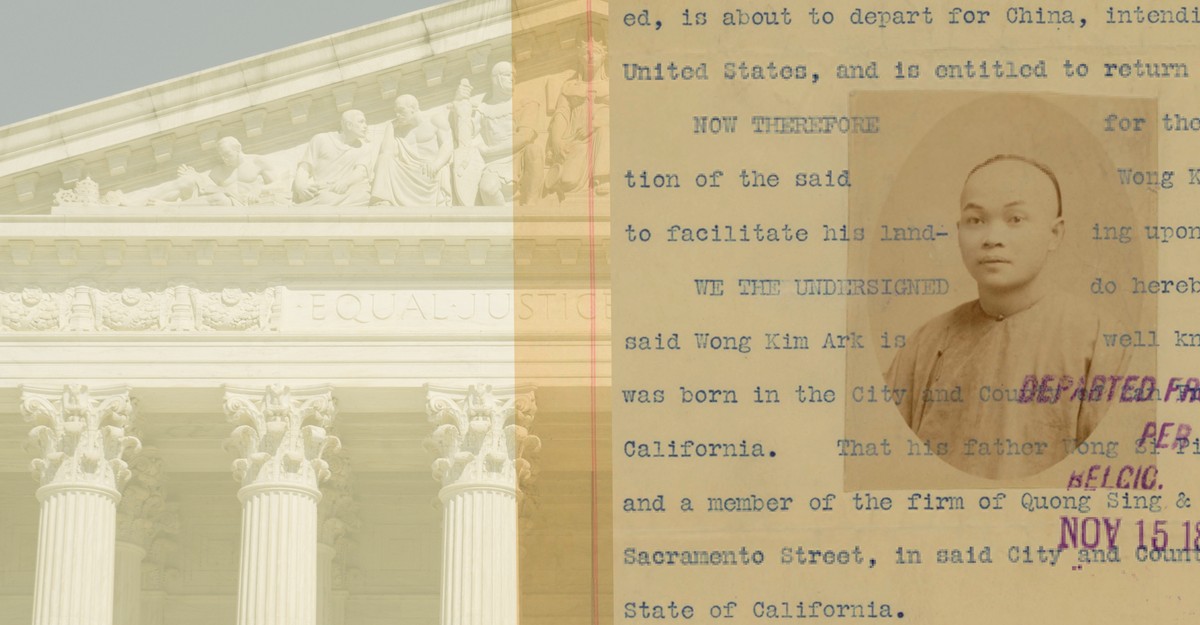

The Supreme Court will hear Trump v. Barbara this week, a challenge that could narrow or overturn the 1898 Wong Kim Ark precedent on birthright citizenship. The administration seeks to exclude children born to parents who are temporary visitors, undocumented, or "owe allegiance to anybody else," a change that could strip citizenship from tens of thousands and reverberate across immigration and civil-rights policy. For investors, the direct market impact is limited, but the decision could have broader political and regulatory implications for domestic politics and immigration-related sectors.

This dispute is a structural legal shock with concentrated near-term catalysts but multi-year economic knock-ons. A Supreme Court outcome that narrows birthright citizenship would not just change individual legal status; it would immediately create uncertainty in labor supply for sectors where foreign-born workers constitute a material share of frontline staff (agriculture, food processing, construction, hospitality). Expect margin pressure in low-margin, labor-intensive businesses within 3–12 months driven by higher compliance costs, more ICE-driven churn, and accelerated automation capex decisions. Second-order fiscal effects are underpriced: changes to who counts as “citizen” feed directly into benefit eligibility, school enrollments, and census-driven federal transfers — a reallocation of tens to low hundreds of billions of dollars over a 3–5 year window across states. That will shift state budget priorities and could widen spreads on municipal paper in states with large immigrant populations if funding formulas or enforcement costs change materially. Litigation and compliance ecosystems (defense contractors for detention, immigration law practices, litigation finance) are asymmetric beneficiaries if enforcement intensifies. Probability-weight the outcomes: the immediate market move should be treated as a binary event with low-to-moderate probability of full legal reversal but high economic optionality if it happens. Execution should favor optionality (short-dated, skewed option structures and small, directional pairs) and be sized to a 1–3% portfolio tilt because the operational implementation lags by months and is subject to countermeasures (Congress, future administrations, state-level litigation). Monitor the Court’s decision within days–weeks and follow-up rulemaking/litigation over 6–18 months for the true economic impact.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly negative

Sentiment Score

-0.30