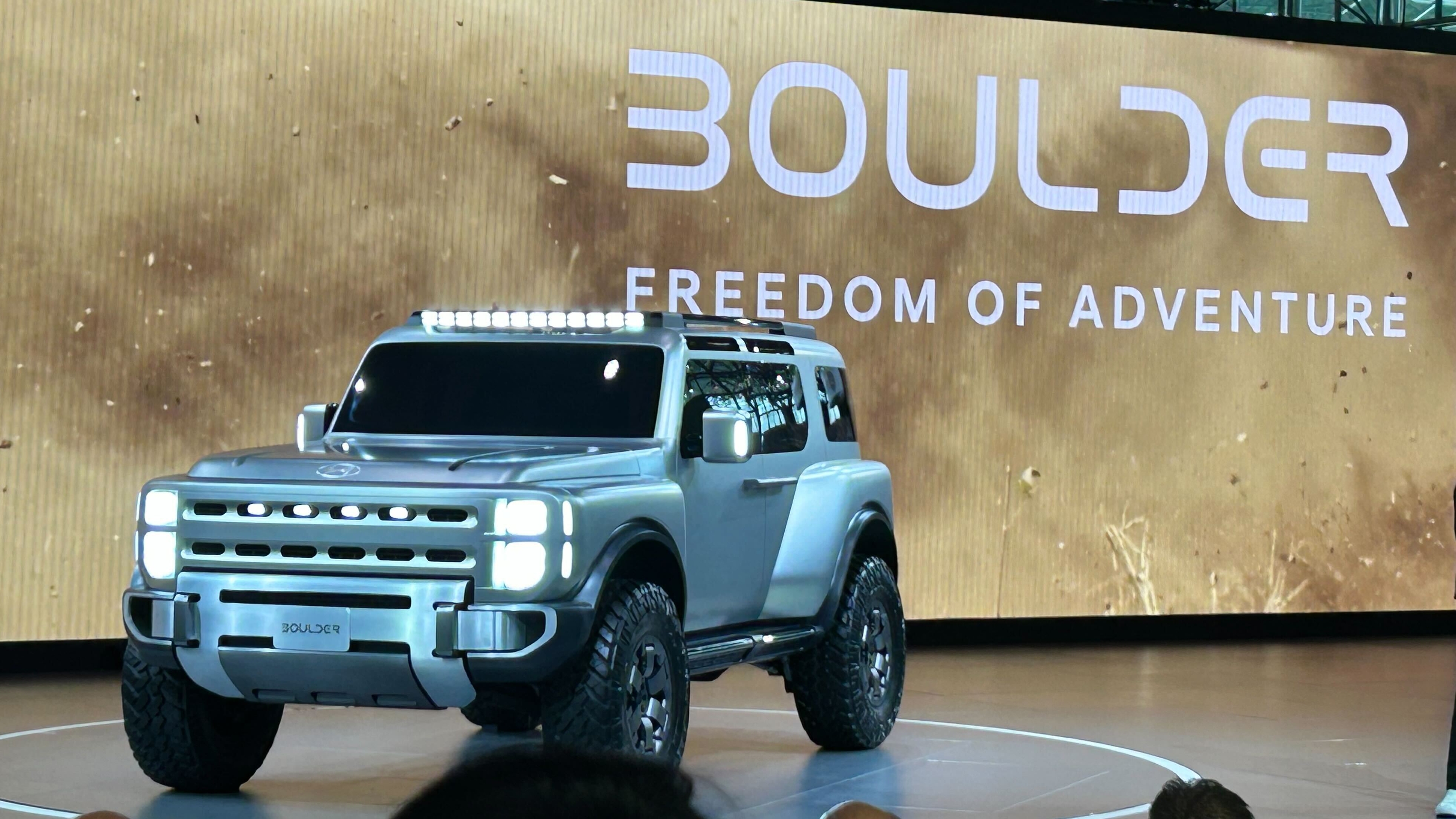

Hyundai unveiled the Boulder off-roader concept at the New York International Auto Show, previewing its plan to produce U.S.-built body-on-frame trucks and off-road-capable SUVs. The concept signals Hyundai's strategic push into the North American truck/SUV segment and potential shifts in its U.S. manufacturing and supply-chain footprint. As a concept reveal, near-term financial impact is limited, but it modestly improves Hyundai's competitive positioning in a high-margin vehicle category.

Hyundai’s push into U.S.-built, body-on-frame trucks is less about one new SKU and more about changing the upstream mix of content and where that content is bought. Body-on-frame architectures shift spend toward heavy sheet/hot-rolled steel, stamped frames, driveline assemblies, axles and ride-control modules—categories where U.S.-based suppliers have capacity and pricing leverage. Expect meaningful RFPs and tooling orders inside a 6–18 month window; those contracts typically front-load CAPEX and deliver recurring parts revenue over 5–7 years, so supplier revenues can re-rate before final vehicle volume proves out. Second-order competitive effects favor suppliers with flexible North American capacity and vehicle-integration capabilities (platform integrators that can supply module-level assemblies), while increasing margin pressure on offshore content providers and logistics chains that currently export major subassemblies. State and federal incentives for U.S. plant builds (tax credits, abatements) amplify the local-content tilt and raise the bar for non-U.S. suppliers to compete cost-effectively. Conversely, incumbents with entrenched dealer/aftermarket networks (Ford, GM, Toyota) retain a service/brand moat that will blunt Hyundai’s share shift unless product and distribution scale quickly. Key catalysts and risks are mostly multi-quarter: supplier award announcements (near-term), factory groundbreakings (3–12 months), and first production (18–36 months). Tail risks: execution (tooling delays), macro (steel/commodity spikes, higher interest rates raising CAPEX costs), and regulation (tightened emissions/EV incentives that could force platform re-design). A reversal could come fast if a large supplier loses a Tier-1 contract or if macro weakens U.S. truck demand, which historically compresses new-platform pricing leverage. From a contrarian perspective, the market may underprice two facts: (1) the speed at which body-on-frame content can be localized via North American suppliers (months, not years) and (2) the short-term revenue impact to modular suppliers through upfront tooling and launch-phase pricing. However, consensus may be over-optimistic on Hyundai capturing dealer-level share quickly; install-base and service economics favor incumbents, keeping absolute share gains modest for 2–3 years.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly positive

Sentiment Score

0.12