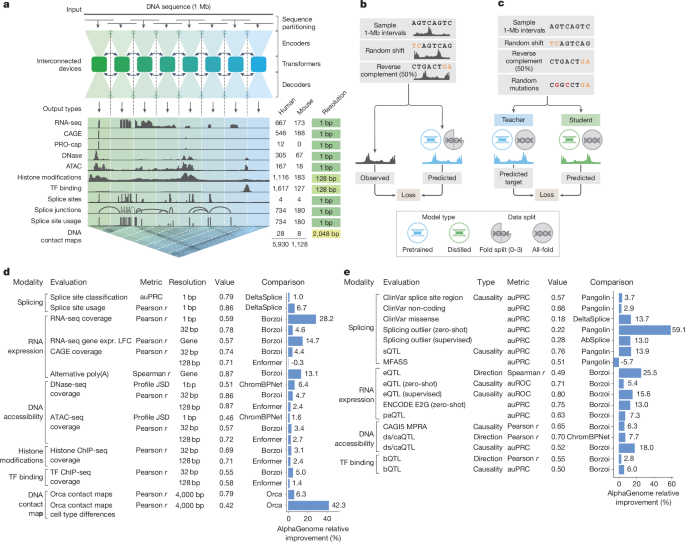

DeepMind released AlphaGenome, a unified deep‑learning model that ingests 1 Mb of DNA sequence and predicts thousands of functional genomic tracks at single‑base resolution across 11 modalities; the model achieved state‑of‑the‑art performance on 22 of 24 genome‑track tasks and 25 of 26 variant‑effect benchmarks. Key metrics include a +14.7% relative improvement on cell‑type gene‑level log‑fold prediction versus Borzoi, eQTL sign accuracy improvement of +25.5% versus Borzoi, and APA Spearman ρ of 0.894 versus 0.790; the distilled student model runs in under 1 second on an NVIDIA H100 and is available via a hosted API and GitHub for non‑commercial use. For investors, this represents a technical platform that could accelerate discovery and diagnostics in genomics, increase competitive pressure on specialized genomics AI vendors, and create downstream commercial opportunities for drug discovery and diagnostic tooling, though direct monetization and regulatory/commercial adoption timelines remain uncertain.

Market structure: AlphaGenome materially raises demand for high-end AI compute (H100 GPUs and TPUs) and for cloud inference services because DeepMind hosts an API; primary winners are NVIDIA (NVDA) and hyperscalers offering GPU/TPU capacity (GOOGL, AMZN, MSFT). Downstream, start-up specialized single-modality model vendors and some wet-lab assay budgets (molecular triage) face compression; pricing power shifts toward providers who bundle compute+models. Expect incremental GPU/HPC spend growth of mid-to-high single digits annually across genomics customers over 12–24 months, tightening lead times for H100-class cards and raising data-center power demand. Risk assessment: Tail risks include rapid regulatory limits on clinical/diagnostic AI (FDA/EMA), export controls on accelerators (US/EU/China), and liability from mispredicted clinical variants; each could erase >30–50% of near-term revenue upside for compute and cloud providers. Immediates (days–weeks): PR-driven equity moves; short-term (months): order flows and supply-chain announcements; long-term (quarters–years): structural uptake in biotech R&D and possible new revenue streams (APIs, licensing). Hidden dependencies: model utility depends on dataset breadth (human+mouse) and DeepMind’s API terms — closed hosting may cap third-party commercial adoption and slow industry-wide monetization. Trade implications: Direct plays: overweight NVDA (infrastructure), long hyperscalers (GOOGL/AMZN/MSFT) that supply TPU/GPU inference; underweight pure-play wet-lab services if >10% portfolio exposure. Prefer option structures to express upside while controlling capital: 3–6 month NVDA call spreads (buy 10% OTM, sell 30% OTM) ahead of quarterly results; consider LASSO-enabled quant exposure to biotech names that integrate in-silico design. Monitor cloud capex announcements and H100 lead-time changes as execution catalysts. Contrarian angles: The market may overestimate immediate monetization — DeepMind-hosted models can centralize value, limiting wider licensing: revenue capture might flow to Google more than to hardware partners. Historical parallels (AlphaFold) show scientific adoption does not equal rapid commercial revenue; expect a 12–36 month lag before durable revenue shifts. Unintended consequences: increased reliance on one vendor raises concentration risk and regulatory scrutiny; if export controls tighten, NVDA upside could be cut by >25% in non-US markets.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly positive

Sentiment Score

0.32

Ticker Sentiment