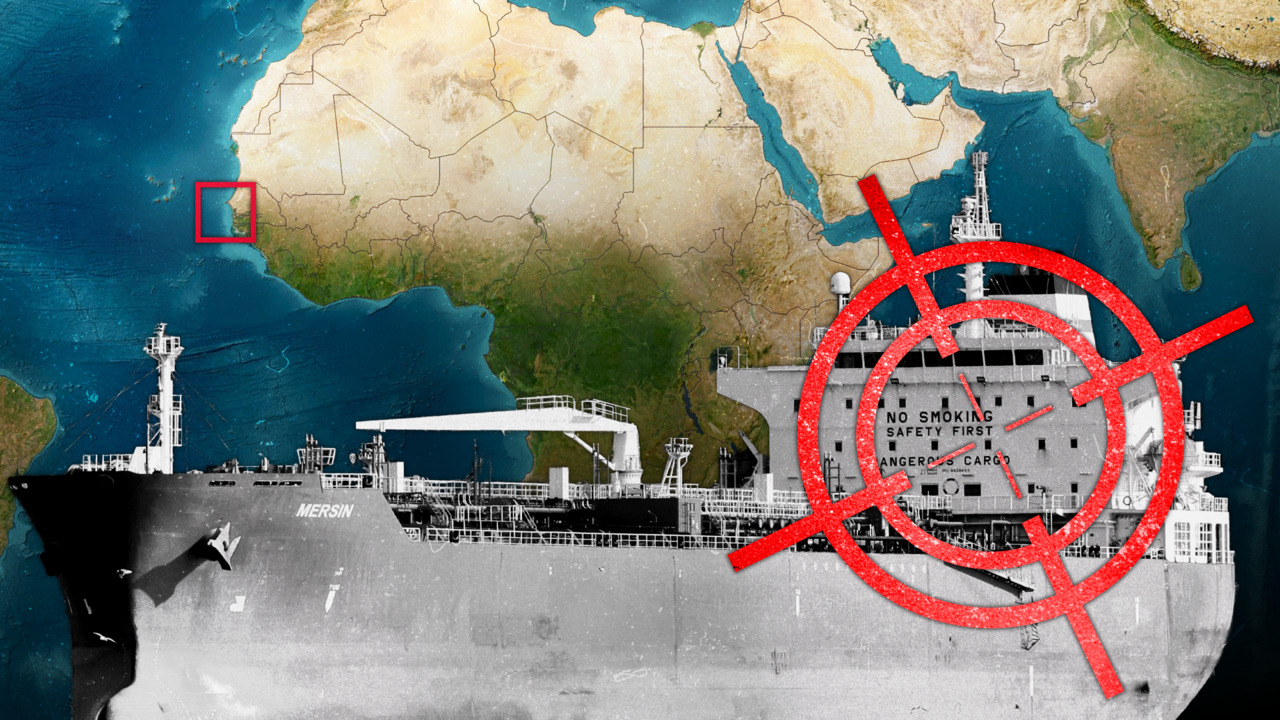

A Turkish-owned oil tanker, the Mersin (sailing under Panama), carrying nearly 39,000 tonnes of fuel was struck by four external explosions off Dakar with no casualties; the vessel has stopped at Russian ports this year and is suspected of links to Russia’s opaque 'shadow fleet'. The incident follows a string of unexplained attacks on tankers and explicitly claimed Ukrainian naval-drone strikes (Sea Baby drones, ~850kg payload) on sanctioned vessels in the Black Sea, signaling a possible geographic escalation to West Africa. The episode raises acute downside risk to maritime insurance, freight routes and the flows used to circumvent Russian oil sanctions, and may lift risk premia on shipping and certain energy trade corridors if such strikes persist.

Market structure: Attacks on “shadow fleet” tankers tilt near-term winners toward crude producers and owners of flexible tanker capacity (owners of VLCC/suezmax capacity) while harming operators with opaque ownership, insurers, and ports servicing dark-tonnage. Expect freight-rate repricing: a 10–30% spike in dirty tanker time-charter (TC) rates is plausible within 1–3 months if attacks continue, improving earnings for liquid tanker equities (FRO, EURN) and increasing insurance premiums for maritime risk. Risk assessment: Tail risks include escalation to insured loss events (large spills/crew casualties) triggering regulatory clamps or frozen insurance cover—this could cause a >50% effective de-rating for lightly capitalized tanker owners in 3–12 months. In the near term (days–weeks) volatility and headline-driven flows will dominate; medium term (3–6 months) underwriting cycles and rerouting costs matter; long term (12+ months) persistent targeting could reduce available shipping capacity and raise structural freight margins. Trade implications: Positioning should be asymmetric: buy leveraged optionality on higher oil/freight (OTM Brent calls, selective tanker equities) while hedging equity volatility and marine-insurance exposures. FX and sovereign spreads for West African EM (e.g., CFA-zone credits) could widen; consider hedging via short iShares MSCI EM ETF (EEM) exposure to frontier African risk if attacks spread. Contrarian angles: Consensus treats incidents as isolated; underestimate the economic weaponization of maritime logistics—if sustained, it accelerates a structural premium for Western insured, transparent shippers and large-cap, compliant tanker owners. The market may be underpricing higher insurance/re-routing costs (20–40% impact on voyage economics) and overpricing risk for large integrated oil majors with diversified logistics.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately negative

Sentiment Score

-0.35