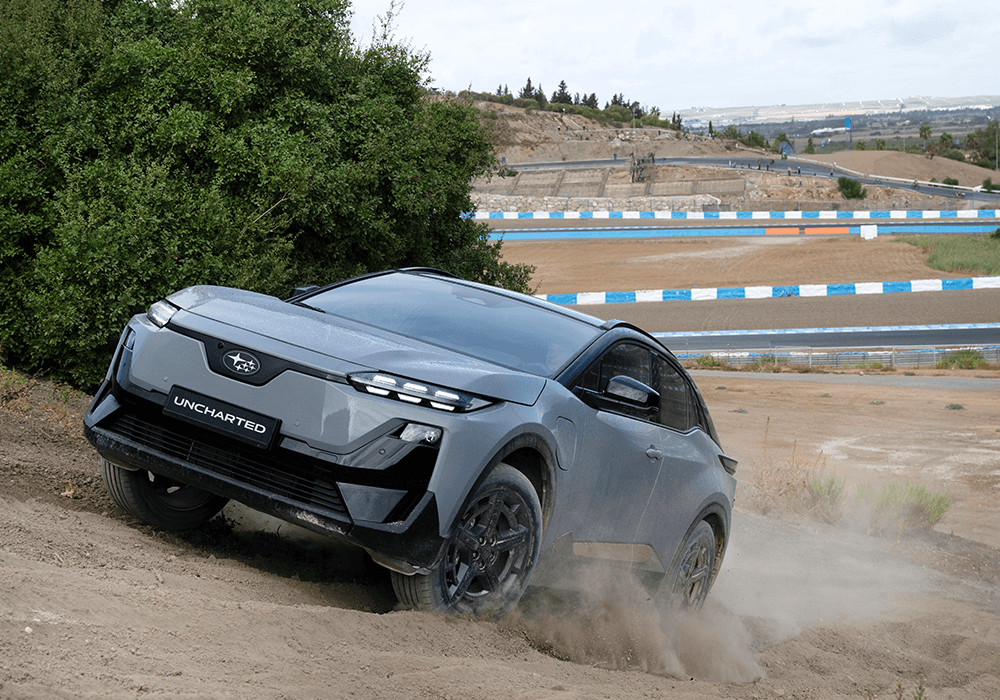

Subaru Australia confirmed the Uncharted small EV will launch in mid-2026; powertrain is dual motors with 252 kW combined, 0–100 km/h in ~5s, a 74.7 kWh CATL battery offering up to 522 km range, 150 kW DC fast charging (10–80% ≈30 min), 22 kW AC charging and 1,500W V2L. The model is built on Toyota's e-TNGA EV platform (shared with bZ4X and Solterra) and largely mirrors the C-HR+ exterior; Subaru NZ and Toyota NZ have said there is no confirmation of local availability. Product strengthens Subaru/Toyota EV lineups but regional rollout uncertainty limits near-term equity impact.

This product-level uncertainty around regional allocation (AU confirmed, NZ undecided) highlights how platform-sharing between incumbents creates optionality that manufacturers can flex to manage regional demand and dealer economics. Toyota/Subaru platform scale (and a third-party battery supply chain dominated by a few large cell makers) lets OEMs push marginal vehicles into markets opportunistically; that suppresses near-term new-model scarcity rents and compresses dealer pricing power where allocation is high. Second-order winners are modular component suppliers and charging-infrastructure vendors: predictable, high-volume platforms lower per-unit costs for inverters, e-axles and standardized charging hardware, boosting Tier-1 volume leverage over 12–36 months. Conversely, niche EV specialists and small-volume importers face margin pressure from better-capitalized OEMs offering similar specs at lower landed cost, which can accelerate consolidation in regional distribution networks. Key catalysts to watch are (1) official NZ allocation decisions and timing (3–9 months), (2) regional incentive or tariff moves that change landed economics within a single quarter, and (3) battery supply cadence from major cell suppliers that can flip global export flows inside 6–12 months. Reversals come from sudden cell shortages, regulatory barriers to rebadged models, or a demand shock that reintroduces scarcity pricing within a single selling season.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

neutral

Sentiment Score

0.05

Ticker Sentiment