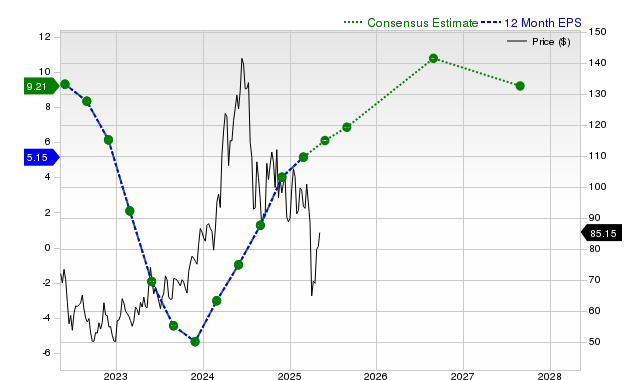

Micron Technology (MU) is drawing significant investor interest, outperforming the S&P 500 and its industry over the past month with a 4.1% return. The chipmaker is poised for substantial financial growth, evidenced by current fiscal year EPS estimates projecting a 518.5% year-over-year increase and robust positive revisions across future periods, alongside consensus revenue growth forecasts exceeding 30% for the next two fiscal years. This strong earnings estimate revision trend, coupled with a consistent history of beating analyst expectations, has resulted in a Zacks Rank #1 (Strong Buy), suggesting potential for continued near-term market outperformance, even as its valuation currently aligns with peers.

Micron Technology (MU) is exhibiting strong positive momentum, with its stock gaining 4.1% over the past month, significantly outperforming both the S&P 500 composite and its direct industry sector. This investor interest is fundamentally anchored in powerful upward revisions to earnings estimates by sell-side analysts. For the current fiscal year, the consensus earnings estimate of $8.04 per share represents a dramatic 518.5% year-over-year increase, with the estimate itself rising 3.6% in the last 30 days alone. This bullish outlook extends into the next fiscal year, with a projected EPS of $13.05, a 62.4% increase. This earnings expansion is supported by robust revenue growth forecasts, with consensus sales estimates pointing to a 47% increase in the current fiscal year and a 33.9% increase in the next. The credibility of these forecasts is reinforced by Micron's recent performance, where it surpassed last quarter's consensus EPS estimate by over 20% and has a track record of beating earnings estimates for four consecutive quarters. Despite this aggressive growth profile, valuation appears reasonable, as the company is graded as trading at par with its peers, suggesting the stock is not in overvalued territory based on current metrics. The combination of these factors culminates in a Zacks Rank #1 (Strong Buy), indicating a high probability of near-term market outperformance.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

strongly positive

Sentiment Score

0.85

Ticker Sentiment