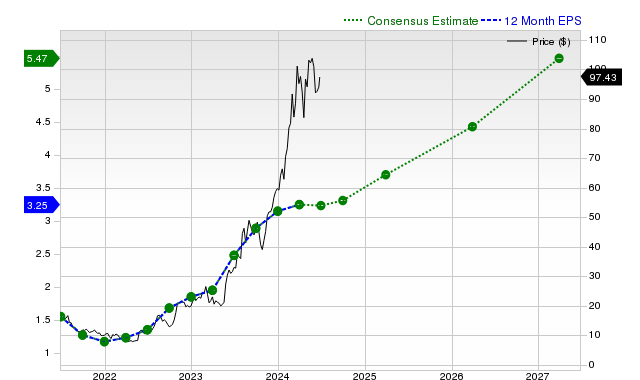

Modine Manufacturing reported quarterly revenue of $738.9 million (up 12.3% YoY) and EPS of $1.06 (vs. $0.97 a year ago), beating Zacks consensus revenue of $690.47 million (+7.01% surprise) and delivering a +9.28% EPS surprise. Analysts' consensus forecasts are stable: Q current EPS $1.02 (+10.9% YoY), FY EPS $4.62 (+14.1%), next FY EPS $6.17 (+33.6%), with sales estimates of $747.49M for the quarter (+21.2% YoY) and $3.04B/$3.36B for current/next fiscal years. Zacks assigns a Rank #3 (Hold) and Value Style Score C; the stock has returned +4.1% over the past month, indicating modest positive momentum but a neutral-to-cautious outlook for investors.

Market structure: Modine (MOD) is positioned to benefit from accelerating OEM thermal content growth tied to electrification; reported revenue +17.6% FY and consensus EPS next-year +33.6% imply expanding unit content and pricing power versus smaller aftermarket players. Competitors with broader product mixes may lose share if MOD converts EV thermal design wins — expect MOD to secure higher-margin contracts over 12–24 months. On cross-assets, sustained beats should compress MOD equity implied volatility and modestly tighten credit spreads for mid-cap industrials; USD strength is a downside for export-exposed sales over the next 3–9 months. Risk assessment: Tail risks include large OEM order cancellations, a macro vehicle-production shock (>15% YoY drop), raw-material shocks (aluminum/copper +20%) or tariff moves that could cut EBIT by >50% in a severe hit. Immediate (days) upside tied to sentiment around recent beats; short-term (3–6 months) depends on guidance cadence and backlog conversion; long-term (12–24 months) hinges on EV content wins and supply-chain capex. Hidden dependencies: MOD outcome is levered to a handful of OEM contracts and inventory cycles — watch OEM production/ship-rate data and supplier backlog disclosures. Trade implications: Direct play — establish a 2–3% long core position in MOD to capture 12-month upside target 25–35%, stop-loss 12%. Pair trade — long MOD (1.5%) vs short Gentherm (THRM, 1.5%) to express relative outperformance: rebalance if spread compresses >15% in 6 months. Options — buy a 6-month call debit spread sized to 0.5% portfolio to cap premium; after position, sell 3-month OTM calls at +15% to collect yield. Rotate 1–2% from large diversified suppliers into focused thermal/component suppliers over next 6–18 months. Contrarian angles: Consensus underweights recurring beats and management’s ability to convert EV platform wins into margin expansion; market hasn’t priced a scenario where MOD sustains >20% revenue growth for two consecutive years. The reaction is likely underdone if OEM design-win cadence accelerates — comparable re-ratings occurred in suppliers after multi-year content wins (example: supplier re-rate post-EV contract wins). Unintended consequence: a macro slowdown could turn strong execution into severe share-price drawdown (>30%), so size positions accordingly and use option-defined-risk structures.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly positive

Sentiment Score

0.25

Ticker Sentiment