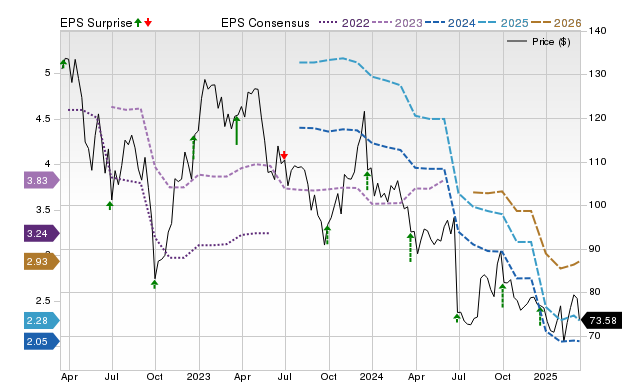

Nike (NKE) is projected to report a significant year-over-year decline in Q1 earnings to $0.28 per share and revenues to $11 billion, according to consensus estimates. However, Zacks' proprietary Earnings ESP model, showing a +25.35% positive Earnings ESP combined with a Zacks Rank #3, indicates a high likelihood that Nike will beat these consensus EPS estimates. This potential earnings surprise, consistent with Nike's track record of exceeding EPS expectations in the past four quarters, could positively influence its near-term stock price despite the anticipated overall decline in performance.

Nike (NKE) is approaching its Q1 earnings release with a consensus forecast indicating significant fundamental deterioration, including a 60% year-over-year decline in EPS to $0.28 and a 5.1% drop in revenue to $11 billion. Despite these bearish headline expectations, which have remained unchanged for the past 30 days, quantitative indicators suggest a high probability of a positive earnings surprise. The company's Zacks Earnings ESP (Expected Surprise Prediction) is a strong +25.35%, which, combined with a Zacks Rank of #3 (Hold), historically correlates with an approximate 70% likelihood of beating the consensus EPS estimate. This outlook is further supported by Nike's consistent track record of surpassing EPS estimates in each of the last four quarters. Consequently, the market is presented with a dichotomy: deeply negative official growth forecasts versus a strong statistical probability of a near-term earnings beat. The ultimate driver for the stock's post-release performance will likely be the magnitude of any surprise and, more critically, management's forward-looking guidance on the earnings call.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately positive

Sentiment Score

0.50

Ticker Sentiment