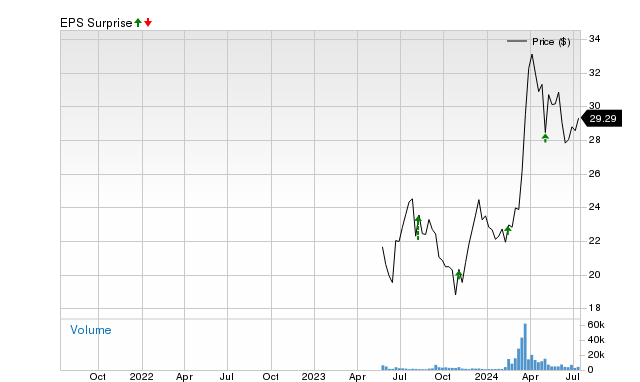

Atmus Filtration Technologies (ATMU), an industrial filtration product company, is poised for another potential earnings beat, extending its record of outperforming estimates with an average surprise of 8.11% over the past two quarters. This positive outlook is reinforced by a strong Zacks Earnings ESP of +9.64% and a Zacks Rank #2 (Buy), indicators that collectively suggest a high probability of exceeding consensus expectations in its upcoming report.

Atmus Filtration Technologies (ATMU) exhibits strong quantitative indicators suggesting a high probability of an earnings per share (EPS) beat in its upcoming quarterly report. The company has an established history of outperformance, having surpassed consensus EPS estimates in its last two reports by an average of 8.11%. Specifically, it delivered a 6.78% surprise last quarter with EPS of $0.63 versus a $0.59 estimate, and a 9.43% surprise in the prior quarter with EPS of $0.58 versus a $0.53 estimate. This historical performance is complemented by bullish forward-looking metrics, most notably a Zacks Earnings ESP (Expected Surprise Prediction) of +9.64%, indicating recent analyst revisions are significantly higher than the broader consensus. The combination of this positive ESP with the stock's Zacks Rank #2 (Buy) is statistically meaningful, as this pairing has historically forecasted an earnings beat nearly 70% of the time, pointing to strengthening near-term earnings potential.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

strongly positive

Sentiment Score

0.80

Ticker Sentiment