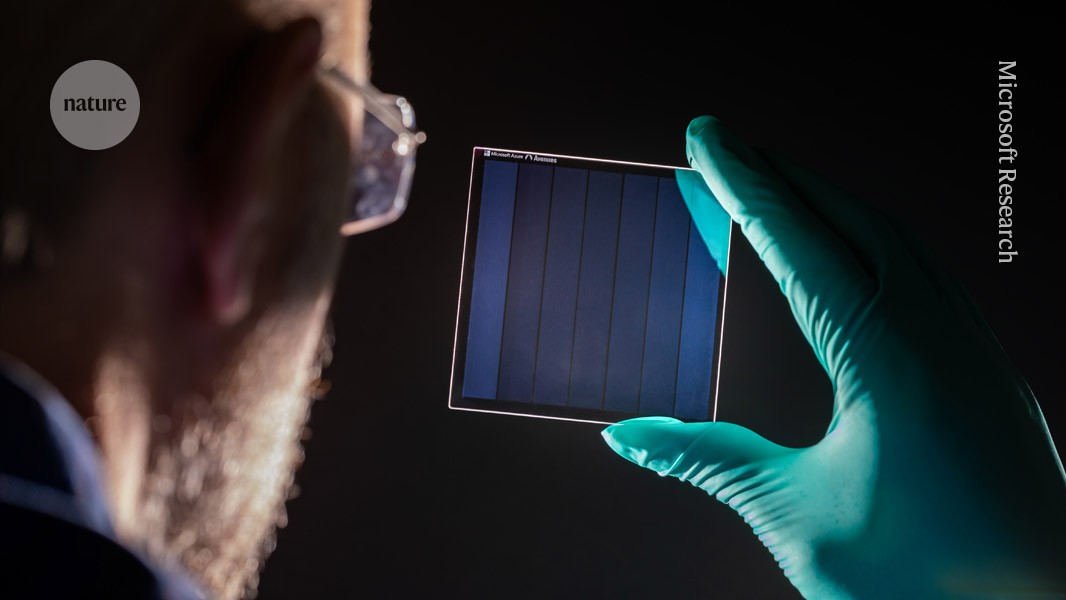

Microsoft Research's Project Silica demonstrated a deployable borosilicate glass archival storage system that uses laser-fired, plasma-induced nanoscale deformations to encode data; a 12 cm × 2 mm square stores 4.8 TB (about 2 million printed books). Published in Nature on 18 February, tests indicate data survival for at least 10,000 years at 290°C and potentially much longer at room temperature; the approach uses cheaper borosilicate glass and microscope-based readout, offering a potential long-term alternative to tapes and hard drives if commercial write/read hardware and standards are adopted.

Market structure: Microsoft (MSFT) is the primary beneficiary — this creates optionality for Azure/enterprise archival services and downstream sales of write/read appliances, while incumbents in tape/HDD (e.g., STX, WDC, perhaps smaller tape vendors) face secular demand erosion over multi-year horizons. Pricing power will initially accrue to Microsoft and customers who control reader standards; tape vendors lose recurring refresh revenue but won’t collapse overnight because cost/per-TB and ecosystem lock-in remain barriers. Expect a gradual shift in demand: negligible displacement in 0–12 months, meaningful share loss for tape/HDD over 2–7 years if cost falls below competitive thresholds. Risk assessment: Tail risks include irreversible format lock–in creating legal/ERISA/data-retention liabilities, failure to scale manufacturing of femtosecond-laser writers/readers, or export controls on high-energy laser tech; each could wipe >50% of projected upside. Immediate market impact on MSFT is minimal; watch 6–24 month proof-of-concept commercial pilots and 2–5 year adoption curves. Hidden dependencies: standards adoption, backwards compatibility, and per-GB write speed and capex per unit; catalysts include hyperscaler pilot wins, government archival contracts, or partnerships with storage integrators. Trade implications: Tactical alpha is long MSFT exposure (asymmetric upside from commercialization) and defensive shorts in exposed hardware names (STX, WDC) or small tape specialists. Use relative-value: long MSFT vs short WDC or STX to capture secular substitution; prefer options to express asymmetric payoffs — buy 9–18 month call spreads on MSFT 8–15% OTM to limit premium. Rotate modestly from direct storage hardware into cloud/AI infra names and increase liquidity by 1–3% of portfolio within 1–3 months as pilots confirm economics. Contrarian angles: Consensus overplays permanence — markets may underprice adoption friction: cost/TB, read/write latency, and ecosystem standards could delay disruption beyond 3–5 years. The market may also under-appreciate regulatory/legal risk from immutable archives (e.g., takedown obligations), which could depress commercial uptake. Historical parallels (optical archives, early SSD adoption) show durable technology doesn’t guarantee rapid incumbent displacement; if parity thresholds (e.g., <$5–10/TB total cost) aren’t hit within 36 months, hardware vendors recover some valuation.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly positive

Sentiment Score

0.28

Ticker Sentiment