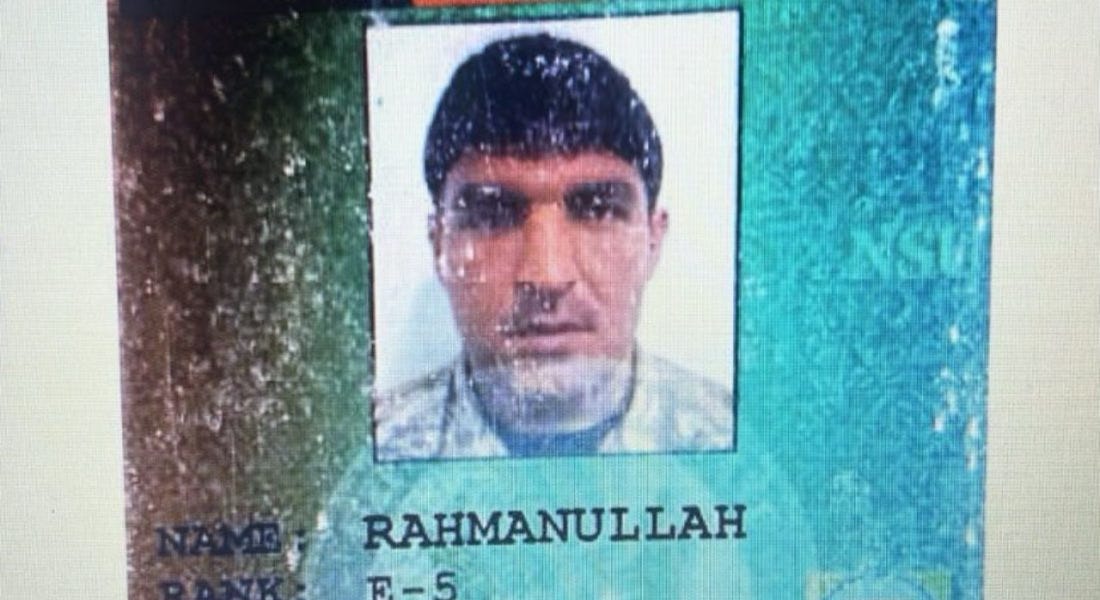

A former Afghan CIA asset, Rahmanullah Lakanwal—evacuated from Kabul in 2021 and granted asylum in 2024—has been charged after assaulting two West Virginia National Guard troopers, prompting scrutiny of U.S. vetting practices. Officials note vetting relies on biometric and biographic checks but is not predictive of future violence; critics also highlight controversial CIA 'Zero Unit' operations. The episode raises political and oversight risk for intelligence and immigration policy, though it is unlikely to have material market implications.

Market structure: The immediate winners are vendors of biometric/AI vetting and large government integrators who win complex contracts (examples: PLTR, LDOS, BAH) as agencies push to shore up screening capabilities; smaller private security and niche contractors face reputational and contract-risk pressure. Expect modest reallocation of program dollars within the $80–120B government services market over 12–24 months, increasing pricing power for incumbents with proven vetting tech and recurring revenue. Demand will pick up for end‑to‑end identity, iris/fingerprint analytics and secure data-matching services; supply is constrained by certification cycles and Fed procurement timelines, favoring scale players. Risk assessment: Tail risks include congressional/DOJ investigations that could freeze contracts or trigger litigation causing 20–40% drawdowns in small caps exposed to intel-work, and a political swing ahead of elections that redirects budgets. Immediate (days) risk is reputational headlines; short-term (weeks–months) is RFP/contract timing and stock moves around hearings; long-term (quarters–years) is durable budget reallocation and tech adoption. Hidden dependencies: asylum/immigration policy, interagency data-sharing upgrades, and FY26 appropriations timing that will materially affect cashflows. Key catalysts: congressional hearings and ODNI/DHS procurement notices in the next 30–90 days; FY26 budget markups in H2 2025. Trade implications: Establish concentrated, time‑bounded exposure to big integrators and vetting-tech: consider 2–3% long PLTR and 1–2% long BAH or LDOS with 12–24 month horizons, target +25–40%, stop-loss 15%. Relative/value: pair long LMT (1–2%) vs short MANT (1%) to play scale vs boutique consolidation; use 3–6 month 10–25% OTM call spreads on PLTR/BAH sized to 0.5–1% notional to cap premium. For downside protection on small-cap services, buy 3–6 month puts or collar structures; enter positions within 2–6 weeks around committee dates and trim on >15% moves or after FY26 budget signals. Contrarian angles: Consensus underprices the multi‑year structural uplift to identity/AI vetting—this is more like a 2001‑style acceleration for tech providers rather than a transient PR shock; specialist tech could outperform by 30–50% over 12–36 months. Reaction could be overdone on boutique contractors; if investigations remain limited, small caps may rebound sharply—watch 10%+ intraday selloffs as tactical reentry opportunities. Monitor concrete signals: award notices on SAM.gov, ODNI/DHS policy memos, and specific hearing dates; a lack of procurement action within 90 days would flip the thesis negative.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly negative

Sentiment Score

-0.25