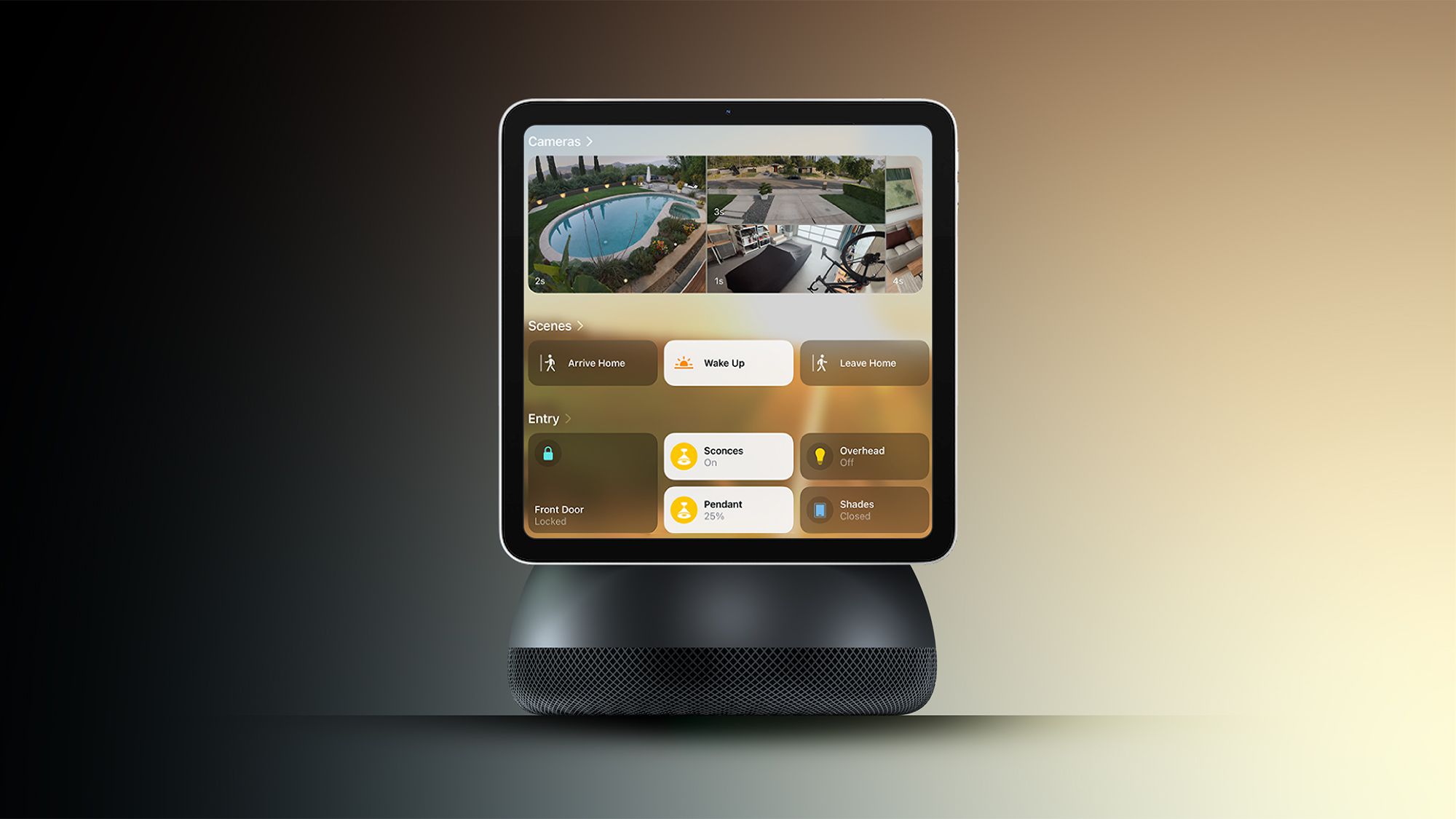

Apple is developing a smart home hub that reportedly includes a small display, speakers and a robotic swiveling base with a strong emphasis on AI capabilities, and sources say the device could ship as soon as this spring around the iOS 26.4 rollout. Reports describe two form factors — wall-mounted and a tabletop/HomePod mini–style unit with sensors to detect presence — though specifics of the swivel mechanism and its use cases remain unconfirmed and may tie into broader robotics efforts planned for later years.

Market structure: A robotic, AI-first home hub amplifies Apple’s hardware+services flywheel — winners are AAPL (ecosystem monetization), sensor/motor/display suppliers, and services/subscriptions; losers are standalone smart‑speaker/NVR vendors (AMZN/GOOGL/SONO) as premium pricing ($199–$399 target) and integration can shift share over 12–24 months. Competitive dynamics: Apple can reprice the category upward, forcing incumbents into lower-margin volume plays or rapid feature catch‑up, putting pressure on competitor gross margins within 2–3 quarters. Supply/demand: Expect front‑loaded component orders and constrained supply early (first 2–3 months), creating upside for parts suppliers but potential channel shortages that limit near‑term unit growth. Risk assessment: Tail risks include privacy/regulatory actions (EU/US probes) and mechanical recalls from moving parts that could swing quarterly EPS by +/-5–10% and dent consumer trust; a product delay to fall 2026 remains plausible if Siri/iOS 26.4 readiness lags. Time horizons: immediate (next 4–8 weeks) for rumor-driven vol, short-term (0–6 months) for launch and sales cadence, long-term (2–4 years) for platform lock‑in and follow‑on tabletop robot. Hidden dependencies: success depends on Siri upgrade quality, sensor accuracy, warranty costs and price elasticity — small changes in adoption rate (±20%) materially change revenue run‑rate. Trade implications: Direct play is AAPL long exposure sized 2–3% of portfolio ahead of spring launch; use 3‑6 month call spreads 5–8% OTM to limit Vega, targeting 10–20% upside if launch/OS catalysts hit. Pair trade: long AAPL vs short AMZN or GOOGL (1–1.5% net exposure) to capture smart‑home share rotation; consider buying 6‑month puts on pure‑play smart‑home vendors (SONO) as asymmetric hedge. Timing: initiate within 2–6 weeks pre‑launch, trim into post‑launch order flow and iOS 26.4 confirmations, exit or re‑size after two quarters or a 15% adverse move. Contrarian angles: Consensus underestimates mechanical/warranty costs and adoption drag — HomePod history shows Apple will iterate price/positioning, not guarantee immediate domination; market may be overpricing a clean win against Alexa/Google if privacy backlash or high price (> $299) depresses TAM. Conversely, supplier equities that sell off on rumors (small motor/display vendors) could be mispriced — identify names with >=30% short interest and >20% revenue exposure to Apple for contrarian longs. Unintended consequences: moving parts increase insurance/recall risk and could invite safety regulations, compressing margins long term.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

neutral

Sentiment Score

0.12

Ticker Sentiment