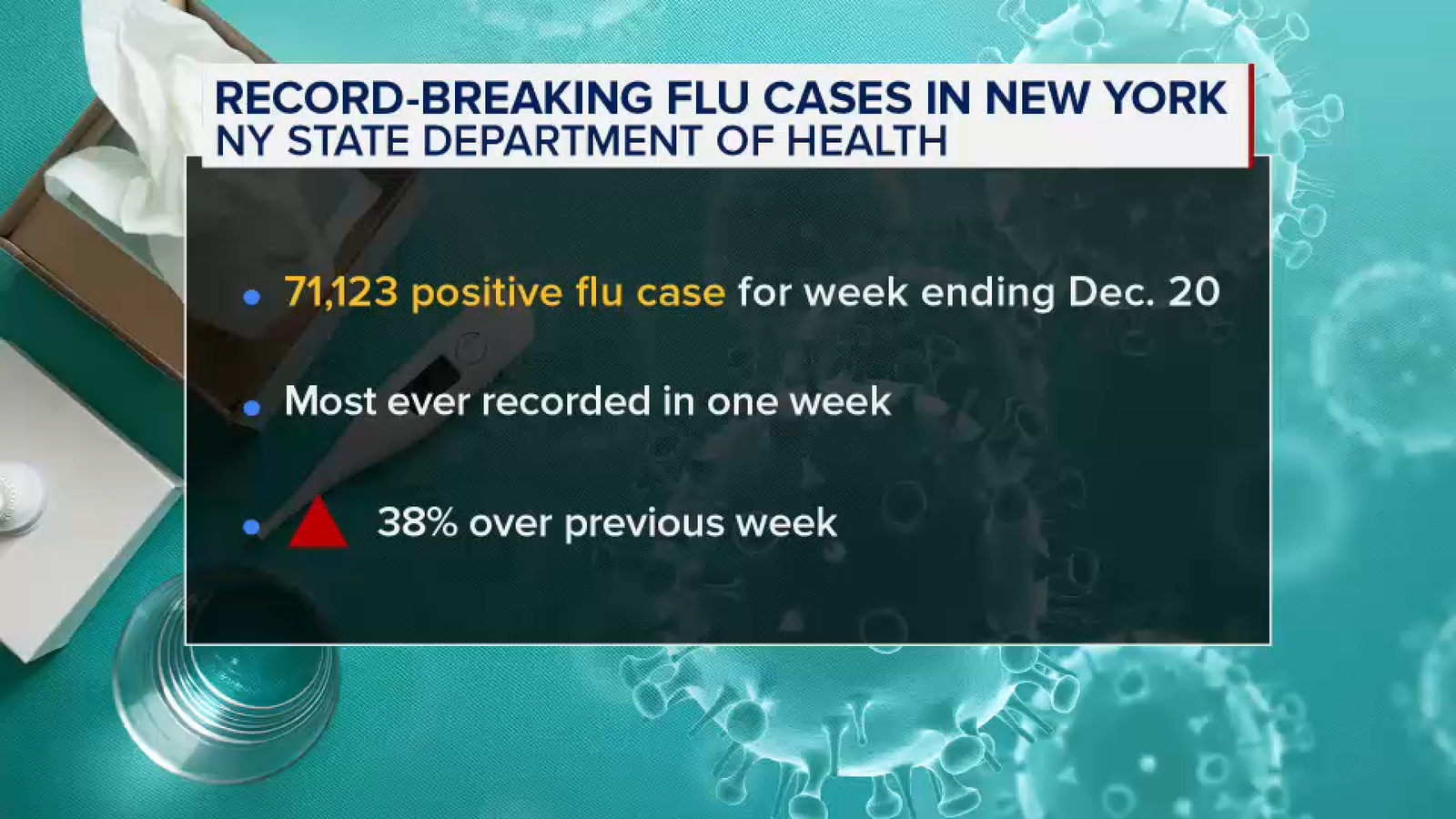

New York State recorded a record 71,123 positive flu cases in the week ending December 20, a 38% increase from the prior week and the highest weekly total since tracking began in 2004. With flu season typically peaking in January and experts warning it could worsen, the surge raises near-term risks for healthcare system strain and workforce absenteeism that could affect consumer-facing businesses and local economic activity. Preventive measures, including vaccination, are being urged to slow transmission.

Market structure: A sharp NY flu surge is a near-term positive for vaccine makers (SNY, GSK), retail pharmacies (CVS, WBA) and OTC/rescue brands (JNJ, PRGO) via higher vaccine volumes and symptomatic product sales in the next 4–8 weeks. Hospitals (HCA, THC) may see revenue upside from admissions but face margin pressure from staff overtime and elective-procedure deferrals; airlines (AAL, DAL) and leisure names risk modest demand softness in Jan–Feb. Risk assessment: Tail risks include a more virulent strain or hospital-capacity constraints forcing regional shutdowns (low probability, high impact) that could widen credit spreads and push 2s–10s flatter by 10–20bp short-term. Hidden dependencies: co-circulation with COVID/RSV could amplify payer reimbursement disputes and absenteeism-driven supply-chain hiccups across retail and services. Key catalysts: CDC weekly positivity reports, state hospitalization dashboards and pharmacy order replenishment notices over the next 2–6 weeks. Trade implications: Prefer tactical longs into January for SNY and CVS (seasonal demand window) sized 1–3% of equity book; hedge with short positions in domestic airlines (AAL) sized 0.5–1% for downside if absenteeism depresses travel. Use 30–90 day call spreads on CVS/SNY and 30–60 day put spreads on AAL/DAL to limit premium spend and time exposure around the January peak. Contrarian angles: Consensus downplays recurring upside to vaccine and OTC margins—pricing for SNY/GSK may be too low if uptake increases 10–20% vs typical season; conversely market may overreact to headline cases by overshorting consumer-discretionary travel stocks. Historical analog: 2017–18 bad flu season lifted pharmacy and OTC sales without systemic market stress, suggesting asymmetric reward for targeted long exposure versus broad defensives.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly negative

Sentiment Score

-0.25