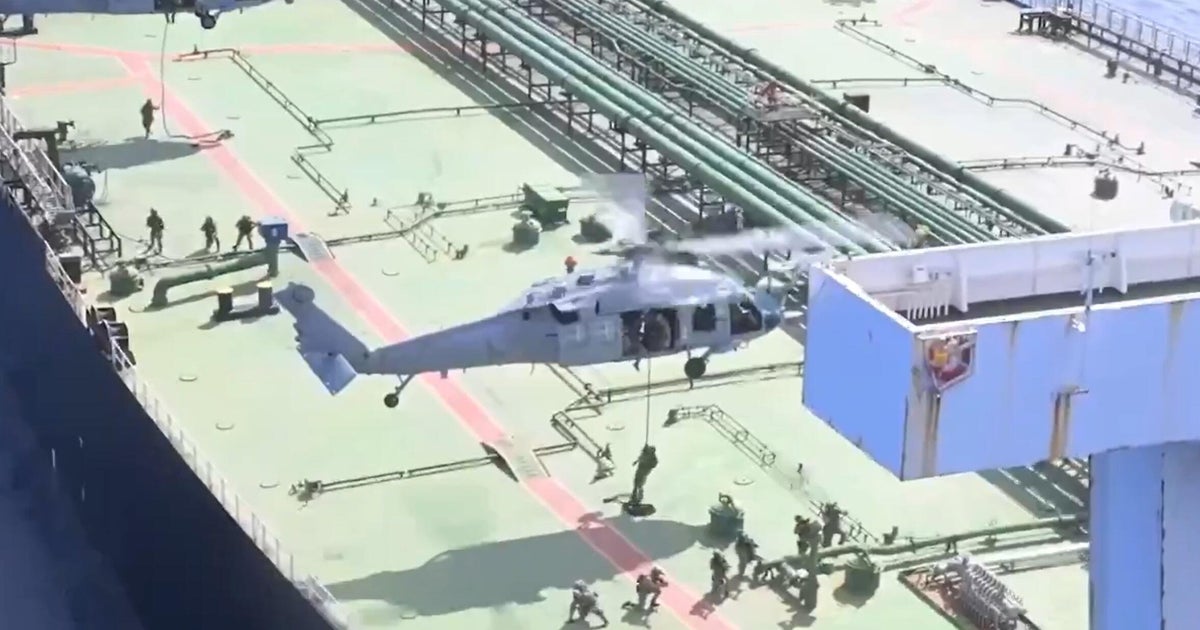

U.S. forces interdicted the sanctioned Iran-linked tanker M/T Majestic X in the Indian Ocean, while Iran seized two commercial ships in the Strait of Hormuz the prior day. The tit-for-tat escalates regional shipping risk and underscores disruption risk for oil flows and commercial maritime routes through a critical chokepoint. The article also notes 15 Filipino seafarers aboard two seized container ships are safe and unharmed.

This is less about the individual tankers and more about the normalization of maritime coercion as a policy tool. The immediate market effect is not a broad energy supply shock; it is a rise in the probability-weighted cost of moving crude and refined products through adjacent corridors, which should bleed into freight rates, war-risk premiums, insurance, and charter availability before it shows up in headline spot prices. Second-order, the most vulnerable assets are not the obvious oil majors but shippers and refiners exposed to Middle East routing flexibility. Even if physical volumes are only intermittently disrupted, repeated interdictions create operational friction: longer voyage times, higher bunkering costs, and a heavier inventory buffer requirement across Asian importers. That tends to favor diversified logistics platforms and domestic pipeline/terminal operators while penalizing spot-exposed tanker owners with weak balance sheets. The catalyst window is days-to-weeks for volatility spikes and months for structural repricing if the cycle persists. The key reversal risk is diplomatic enforcement discipline: if both sides stop at symbolic seizures and avoid sustained blockage of chokepoints, the crude risk premium will fade quickly. But if either party broadens from boarding actions to missile/drone harassment or insurance denial, the market will have to reprice not just Brent but the entire seaborne trade stack. The consensus is probably underpricing the knock-on effect in refined products and freight rather than crude itself. Diesel, jet fuel, and naphtha spreads can widen faster than Brent because refiners and traders hedge crude but cannot as easily hedge routing disruption and vessel detention risk. That makes this a better relative-value trade than a directional energy-beta expression right now.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

moderately negative

Sentiment Score

-0.35