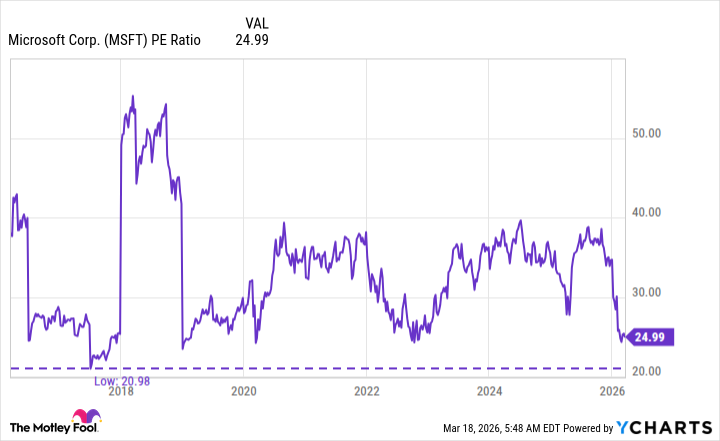

Broadcom projects its custom AI chip business to generate $100 billion+ in revenue by end-2027; its AI semiconductor unit reported $8.4B in the latest quarter (+106% YoY) and the company sits at roughly a $1.5 trillion market cap. Nvidia is expected to deliver ~70% revenue growth this fiscal year but trades at ~22x forward EPS (roughly in line with the S&P 500 at ~21x), implying current valuation does not price sustained AI-driven growth. Microsoft is described as trading near decade-low P/E levels for its cloud/subscription-era business; the author calls all three 'screaming' or 'no-brainer' buys, signaling a bullish conviction on multi-year AI demand.

AI-driven capex is creating a two-track market: general-purpose accelerated compute (GPUs) remains a volume play with tight supply dynamics at foundries, while custom ASICs shift margin pools upstream to chip designers and systems integrators. That bifurcation benefits fabs, EDA/IP owners, and backend test/assembly vendors — expect incremental revenue and pricing tailwinds at TSMC/ASML and packaging houses if Broadcom’s custom wins scale. Conversely, OEMs and third-party GPU cloud resellers face price compression in pockets where hyperscalers internalize acceleration.

Key catalysts cluster by cadence: earnings/guidance and product cycles move the next 30–90 days, new architecture launches and design-win announcements drive 6–18 month re-rating, and capex reallocation (GPUs -> ASICs) plays out over multiple years with durable structural winners. Tail risks include a macro-driven AI capex pause, renewed export controls or supply normalization that broadens competition, and execution shortfalls on custom-chip projects — any of which could flip the narrative within quarters.

Positioning should reflect asymmetric outcomes: concentrated, long-dated exposure to the hardware/design winners, hedged for short-term cyclicity. Size allocations should account for conviction: reward multiples if the ASIC thesis accelerates (2x–4x over 12–36 months) but capped losses if demand stalls. Watch flow-through metrics (server billings, hyperscaler capex, foundry lead times) as high-signal, high-frequency indicators to adjust exposure.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

strongly positive

Sentiment Score

0.70

Ticker Sentiment