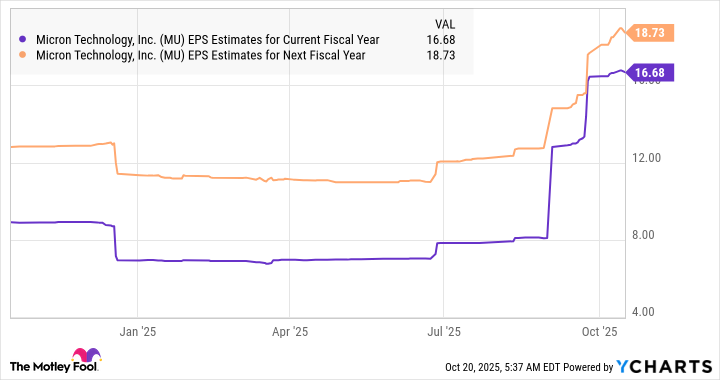

Micron Technology (MU) shares have surged 140% in 2025, yet the company remains attractively valued at 24x trailing earnings despite strong fiscal 2025 results, including a 49% revenue increase to $37.4 billion and a significant rise in EPS to $8.29, largely driven by robust demand for high-bandwidth memory (HBM) chips in AI servers. While Micron is exiting data center memory sales to Chinese customers, representing a minor revenue impact, it plans to reallocate this capacity to other markets, with analysts forecasting continued substantial earnings growth and a potential 170% upside given its HBM leadership and the long-term AI infrastructure spending trend.

Micron Technology (MU) has demonstrated exceptional fiscal performance, with shares surging 140% in 2025, driven by a 49% year-over-year revenue increase to $37.4 billion and a significant jump in non-GAAP EPS to $8.29. Despite this rally, MU trades at an attractive 24x trailing earnings, a substantial discount to the Nasdaq-100's 33x, positioning it as a potentially undervalued AI play. The company's robust growth is primarily fueled by secular demand for high-bandwidth memory (HBM) chips, critical for AI servers and processors. Micron's cloud memory business unit (CMBU) revenue surged 3.5x to $13.5 billion, with Goldman Sachs forecasting significant HBM demand increases of 23% for GPU-related and 82% for custom AI processors next year. Micron is actively expanding manufacturing capacity to meet this accelerating demand. While Micron is exiting data center memory sales to Chinese customers, a move prompted by 2023 restrictions, this segment represented only 7% ($2.6 billion) of its prior fiscal year's revenue. The company plans to reallocate this freed-up capacity to other markets, mitigating the impact and ensuring continued supply to its six HBM customers, including major AI chipmakers like Nvidia, Broadcom, and AMD. Analysts anticipate continued strong earnings growth, with a potential doubling in fiscal 2026, supported by the projected $4 trillion AI infrastructure spending by decade-end. This earnings trajectory, combined with its current valuation, suggests a potential 170% upside to $550 per share if MU's valuation aligns with the broader tech index.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

extremely positive

Sentiment Score

0.85

Ticker Sentiment