Okta (OKTA) is trending on Zacks.com, with its shares recently declining -18.9% over the past month, while the Zacks Security industry gained 4%. Despite this recent underperformance, Okta has a Zacks Rank #2 (Buy), driven by positive earnings estimate revisions; the consensus EPS estimate for the current quarter is $0.84, a +16.7% year-over-year change, and revenue is expected to grow by 10% to $710.75 million. However, the stock is graded D in value, indicating it is trading at a premium to its peers.

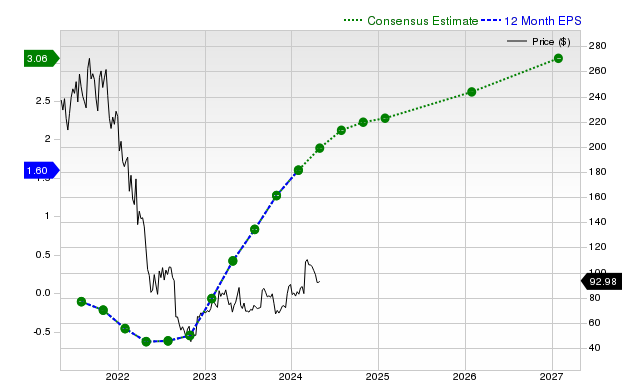

Okta, Inc. (OKTA) has garnered significant investor attention despite a recent sharp decline in its stock price, which fell 18.9% over the past month, starkly underperforming the Zacks S&P 500 composite's +0.6% change and the Zacks Security industry's +4% gain. Notwithstanding this share price weakness, fundamental indicators appear robust. Analysts have notably revised earnings estimates upwards; the Zacks Consensus Estimate for the current quarter's earnings per share (EPS) is $0.84, reflecting a 16.7% year-over-year increase, and this estimate has risen by 22.2% in the last 30 days. Similarly, the current fiscal year EPS estimate of $3.28 indicates a 16.7% year-over-year growth, with a 12.3% upward revision in the past month. For the next fiscal year, EPS is projected at $3.57, an 8.6% increase, with estimates up 1.4% recently. This positive trend in earnings revisions contributes to Okta's Zacks Rank #2 (Buy). Revenue growth forecasts also remain positive, with a consensus sales estimate of $710.75 million for the current quarter (+10% YoY) and anticipated growth of 9.4% and 9.6% for the current and next fiscal years, respectively. Okta's last reported quarter showed strong performance, with revenues of $688 million (+11.5% YoY) and EPS of $0.86, surpassing consensus estimates by 1.22% and 11.69% respectively, and extending a streak of beating both revenue and EPS estimates for the past four quarters. However, the company's valuation is a point of caution, as evidenced by a Zacks Value Style Score of D, indicating it trades at a premium compared to its peers.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

strongly positive

Sentiment Score

0.60

Ticker Sentiment