The text is website cookie/privacy boilerplate and contains no financial news, data, or events. There is nothing actionable or market-moving for a portfolio manager.

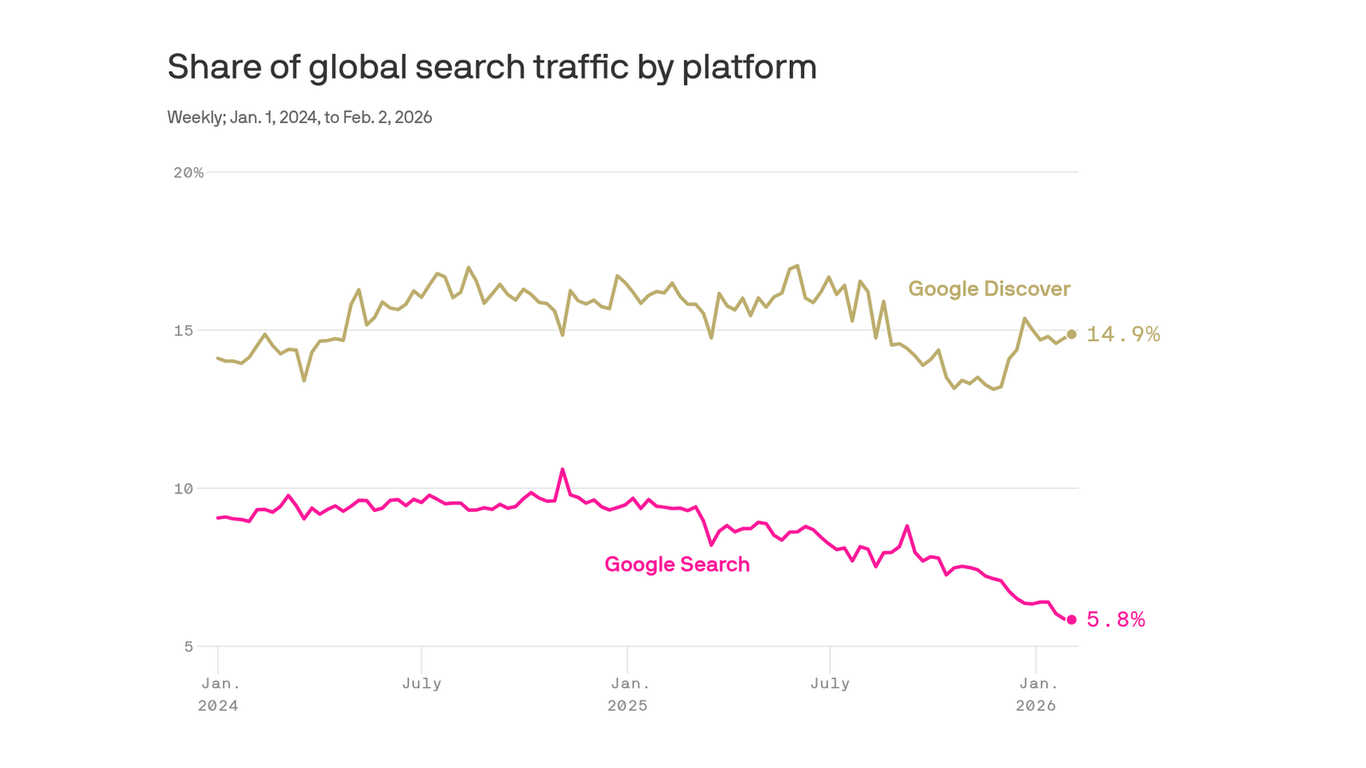

Privacy-driven opt-outs and fragmented state-level definitions of “sale/sharing” are not just a compliance headache — they compress the marginal value of third-party cookies and accelerate a flight to first‑party identity and server‑side signals. Expect programmatic open‑web CPMs to weaken first (we model a 10–25% decline across 6–12 months for audience-targeted inventory) while walled gardens and direct‑to‑publisher subscription strategies capture share and pricing power. Second‑order winners will be companies that monetize authenticated relationships, clean‑room analytics, and consent/ID orchestration — these are capacity and integration plays (CDPs, marketing clouds, server‑side tag managers). Conversely, supply‑side platforms and smaller header‑bidding dependent publishers face a twofold squeeze: lower CPMs and higher customer acquisition costs as publishers invest in paywalls and email capture instead of programmatic scale. Key catalysts and risks: state regulatory clarifications, multi‑state litigation, and browser/OS vendor moves (e.g., additional cookie restrictions or new privacy APIs) can move outcomes in weeks; major tech industry agreements on a universal identifier or a rapid uptake of server‑side conversions could reverse revenue pressure over 6–18 months. Tail risk: a federal preemption or a widely adopted industry ID could restore programmatic yields faster than the market anticipates, while protracted regulatory divergence could entrench walled gardens and materially reduce open‑web liquidity over years.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

neutral

Sentiment Score

0.00