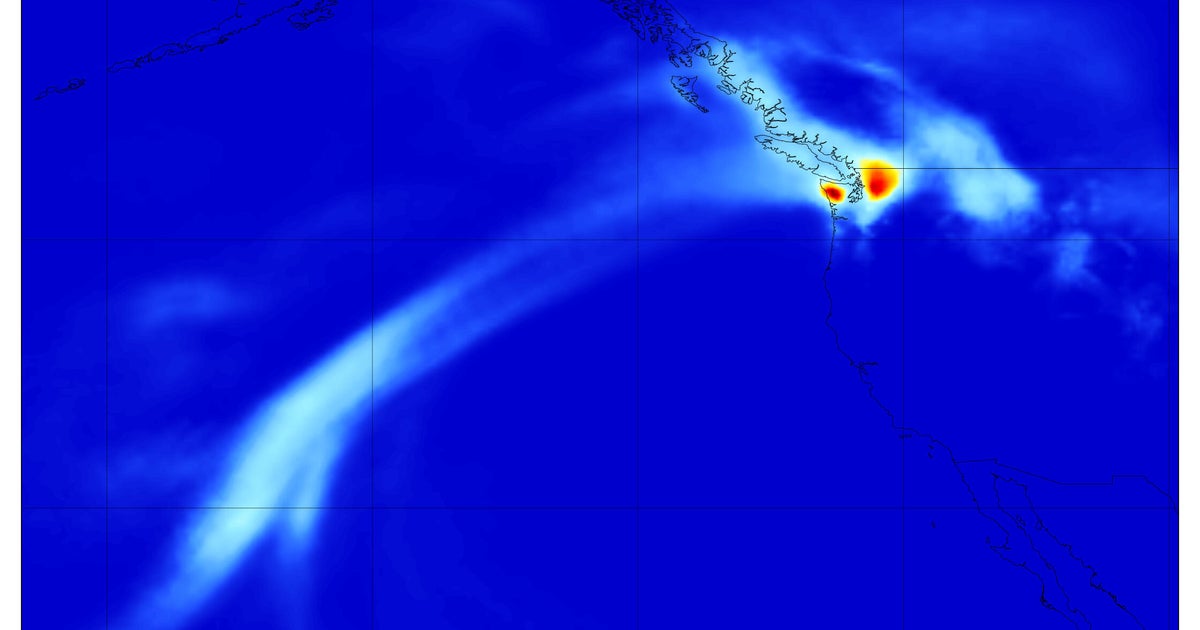

NOAA unveiled a new suite of AI-driven forecasting systems — AIGFS, AIGEFS and a Hybrid-GEFS — that leverage its existing GFS/GEFS frameworks to deliver faster and potentially more accurate weather predictions. The agency estimates computational requirements will fall by 91–99% (a single 16‑day AIGFS run uses ~0.3% of operational GFS compute and completes in ~40 minutes), and forecasts could be extended by roughly 18–24 hours; NOAA notes remaining work on hurricane track accuracy and ensemble diversity. The improvements could materially lower operational costs for large-scale numerical forecasting and speed data delivery to forecasters, though model refinements are still needed before full operational reliance.

Market structure: NOAA’s AI forecasts — 16‑day runs in ~40 minutes using 91–99% less compute — reallocate value from raw compute and proprietary feed vendors toward platforms that host, integrate and monetize higher‑frequency, cheaper public forecasts. Winners: cloud providers (AMZN, MSFT, GOOGL) and AI chip/software vendors (NVDA, PYPL for payments on services) that enable model serving and downstream analytics; insurance/reinsurance (RE, MKL) and commodity traders who can tighten risk models. Losers: niche paid weather‑data businesses and high‑end HPC hardware suppliers whose incremental compute contracts for traditional NWP may decline. Risk assessment: Tail risks include a high‑profile hurricane misforecast that triggers regulatory scrutiny, lawsuits and a freeze on NWS adoption (probability low, impact high). Short horizon (days–weeks): market re‑pricing of small cap vendors and cloud infra guidance; medium (3–12 months): NOAA validation in hurricane season and formal NWS deployment; long (1–3 years): insurance pricing cycles and volatility compression in ag/energy markets. Hidden dependencies: federal funding, hybrid GEFS use, and the need for periodic retraining — NOAA’s savings may not fully displace commercial products that add proprietary value. Trade implications: Favor long cloud/AI exposure (NVDA, AMZN, MSFT) and selective reinsurers (RE, MKL) to capture lower catastrophe volatility and higher analytics demand; consider tactical shorts in HPE/IBM’s high‑margin HPC exposure where gov spend could shrink. Options: sell short‑dated ATM straddles on CORN/CBOE agricultural implied vol (30–90d) to monetize expected vol compression, with strict stop if realized vol > implied by 50% of premium. Pair trade: long RE (12–24m) / short HPE (3–9m) to capture relative upside as forecasting risk falls. Contrarian angles: Consensus may under‑estimate that commoditized forecasts actually expand addressable market for analytics — cheaper forecasts enable more frequent runs and productization, sustaining cloud and software demand. Conversely, investors may be overpaying pure HPC names for a transient revenue stream; watch NOAA’s hurricane‑season verification (hit rate, false alarm ratio) over next 90 days — a >5% miss vs historical benchmarks would meaningfully reverse sentiment. Historical parallel: major NWP upgrades in the 1990s compressed some services but ultimately expanded derivative analytics markets, suggesting a multi‑year structural shift rather than a one‑time shock.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly positive

Sentiment Score

0.32