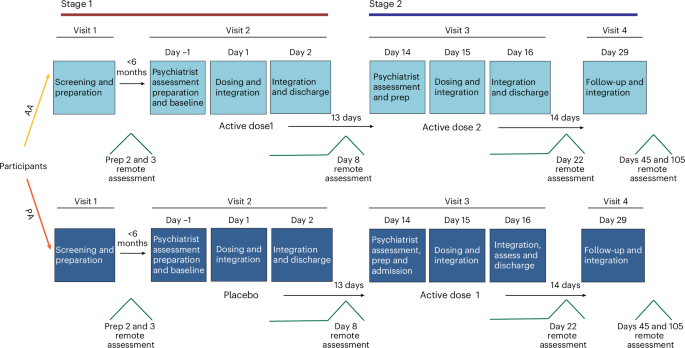

A Small Pharma/Cybin‑sponsored phase IIa randomized, double‑blind, placebo‑controlled trial in 34 adults with moderate‑to‑severe MDD found a single 21.5 mg IV 10‑minute infusion of DMT fumarate (SPL026) produced a statistically significant reduction in MADRS at 2 weeks versus placebo (mean difference −7.35; 95% CI −13.62 to −1.08; P = 0.023; d = 0.82), with larger early effects at 1 week (mean diff −10.75; P = 0.002) and antidepressant effects persisting up to 3 months. Safety was acceptable—most TEAEs were mild/moderate (infusion site pain, nausea, transient anxiety), no serious adverse events or withdrawals related to treatment—and a second dose provided no clear additional benefit, supporting further but cautious clinical and commercial development.

Market structure: The trial props up sponsors and DMT-focused developers (CYBN foremost; GHRS, AGNPF as secondary beneficiaries) by validating a short-acting psychedelic that could lower chair-time and clinic costs versus psilocybin. If adoptable at scale, capturing 5–10% of the ~$8–12bn annual MDD treatment market implies $400M–$1.2bn revenue opportunity dispersed across successful sponsors within 3–7 years, but incumbents (large SSRI makers) are unlikely to be disrupted near-term due to formularies and prescribing inertia. Risk assessment: Material tail risks include regulatory scheduling/DEA action, negative larger trials, and therapeutic-delivery bottlenecks (therapist scarcity and reimbursement), any of which could wipe out equity value (>70% downside in small-caps). Time buckets: immediate (days/weeks) — sentiment and fundraising moves; short-term (3–9 months) — additional Phase II/III readouts and regulatory signals; long-term (1–3 years) — commercial pathway, payer coverage and capacity scaling. Trade implications: Favor asymmetrical, time-limited exposure to CYBN via 9–18 month call spreads (limited premium, 1–2% portfolio exposure) to capture regulatory/clinical readouts while capping downside; avoid large outright long equity positions without clearer Phase III data. Consider a relative-value pair: long CYBN (1.5% net) / short CMPS (1% net) to express preference for rapid-infusion DMT adoption vs longer psilocybin sessions, using options to limit tail risk. Contrarian view: Consensus underestimates operational friction — therapy cost and workforce limits could cap peak revenue well below trial-implied potential; early sponsor-led trials historically produce larger effect sizes than subsequent registrational studies (see early psilocybin runs). If blinding/expectancy materially inflated results, downside may be swift once independent datasets arrive, creating late-stage short opportunities.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly positive

Sentiment Score

0.30

Ticker Sentiment