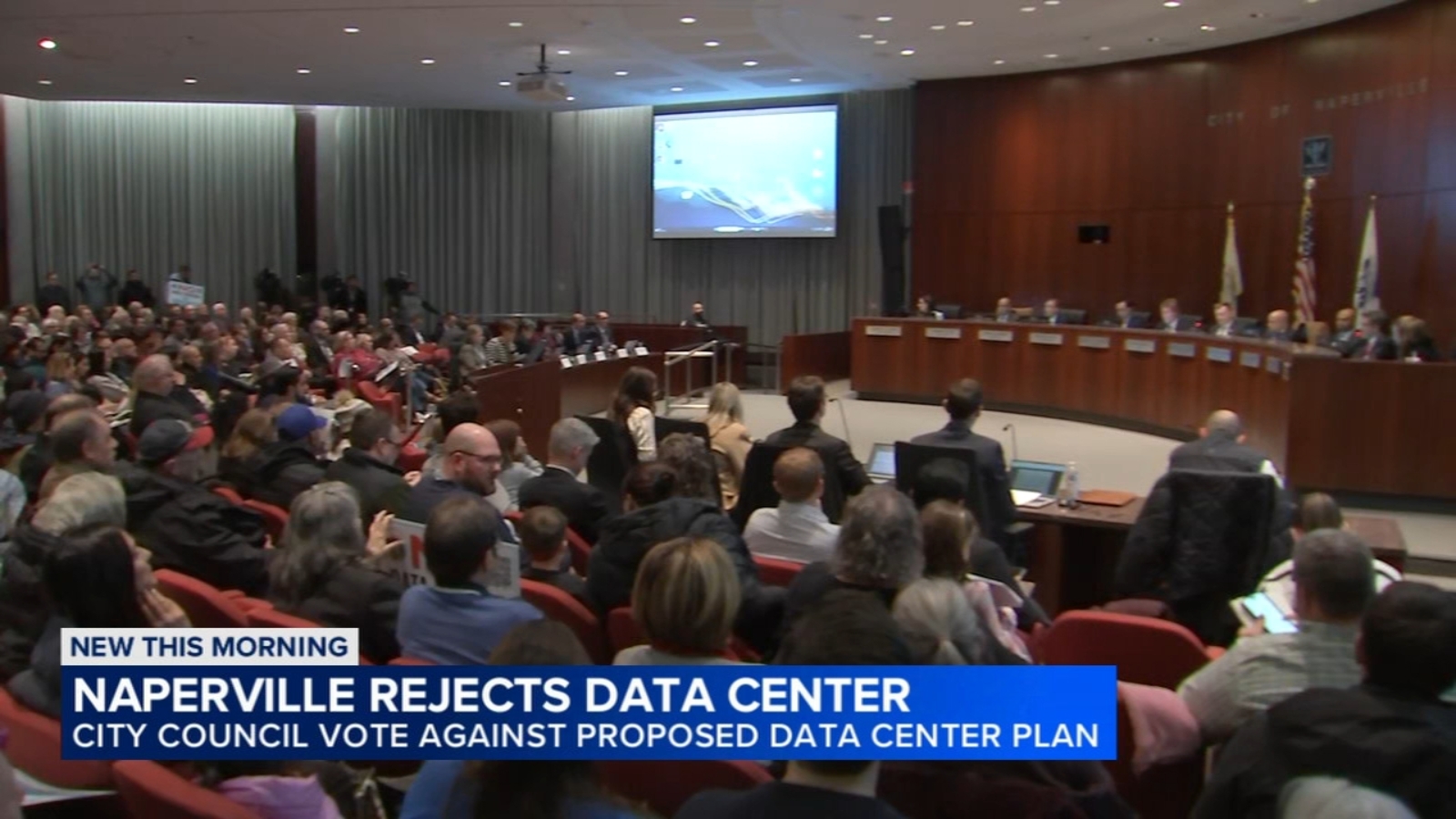

Naperville city council voted 6-1 with two abstentions to reject Karis Critical's proposed ~145,000 sq ft data center on the former Lucent campus along I‑88 after months of public opposition; the developer had proposed reducing on-site diesel backup generators from 24 to 12. Karis said generators would be used only for outages and monthly tests and had pledged 'hundreds of millions' of investment, but the council's decision—overturning the city plan commission—raises local regulatory and community-risk concerns that could deter similar data-center and infrastructure investments.

Market structure: The Naperville denial is a localized but high-signal shock to suburban data-center permitting that benefits established, permitted players and markets with smoother entitlement (Northern Virginia, Phoenix). Expect a modest reallocation of near-term demand — I estimate 1–3% of planned Chicagoland capacity could migrate to other metros over 6–12 months, tightening supply in permitted pipelines and supporting premium rents for shovel-ready sites (+5–15%). Local contractors and the specific developer lose; public-equity winners are large, diversified data‑center REITs (DLR, EQIX) with national footprints. Risk assessment: Tail risks include a cascade of municipal rejections across other U.S. suburbs producing a 5–10% NAV markdown for REITs concentrated in regulatory‑dense markets; a positive tail is state or county-level preemption that standardizes permitting. Immediate (days) volatility is political/media-driven; short-term (30–90 days) impacts center on permit/backlog reallocation; long-term (3–24 months) the industry may accelerate battery/clean backup adoption, adding 10–25% up-front capex to projects. Hidden dependencies: utility interconnect timelines and diesel‑generator ESG backlash are first-order constraints that will drive capex and permitting outcomes. Trade implications: Favor long positions in large, geographically diversified data-center operators (DLR, EQIX) for 6–12 months to capture demand migration; underweight single-market or privately‑developed Midwest projects and smaller industrial REITs exposed to Chicagoland (relative shorts). Use small, tactical option structures (3–6 month call spreads) to express convexity into rerating while limiting capital. Watch bond spreads for muni credits in suburbs — a pattern of denials could modestly compress local tax base growth and widen muni spreads for development‑backed issuances. Contrarian angles: The consensus reaction (binary negative for all data-center equities) is overbroad — the denial is anti‑developer not anti-demand; large REITs with utility relationships and existing permits could capture pricing power. This could underprice the winners’ upside (5–15% recovery) while overpricing the pain for nationally diversified names. Historical parallels: permitting shocks in other infrastructure (wind/solar siting fights) led to short-term headlines but medium‑term concentration benefits for incumbents and technology shifts (battery replacement of diesel) that created new suppliers.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately negative

Sentiment Score

-0.40